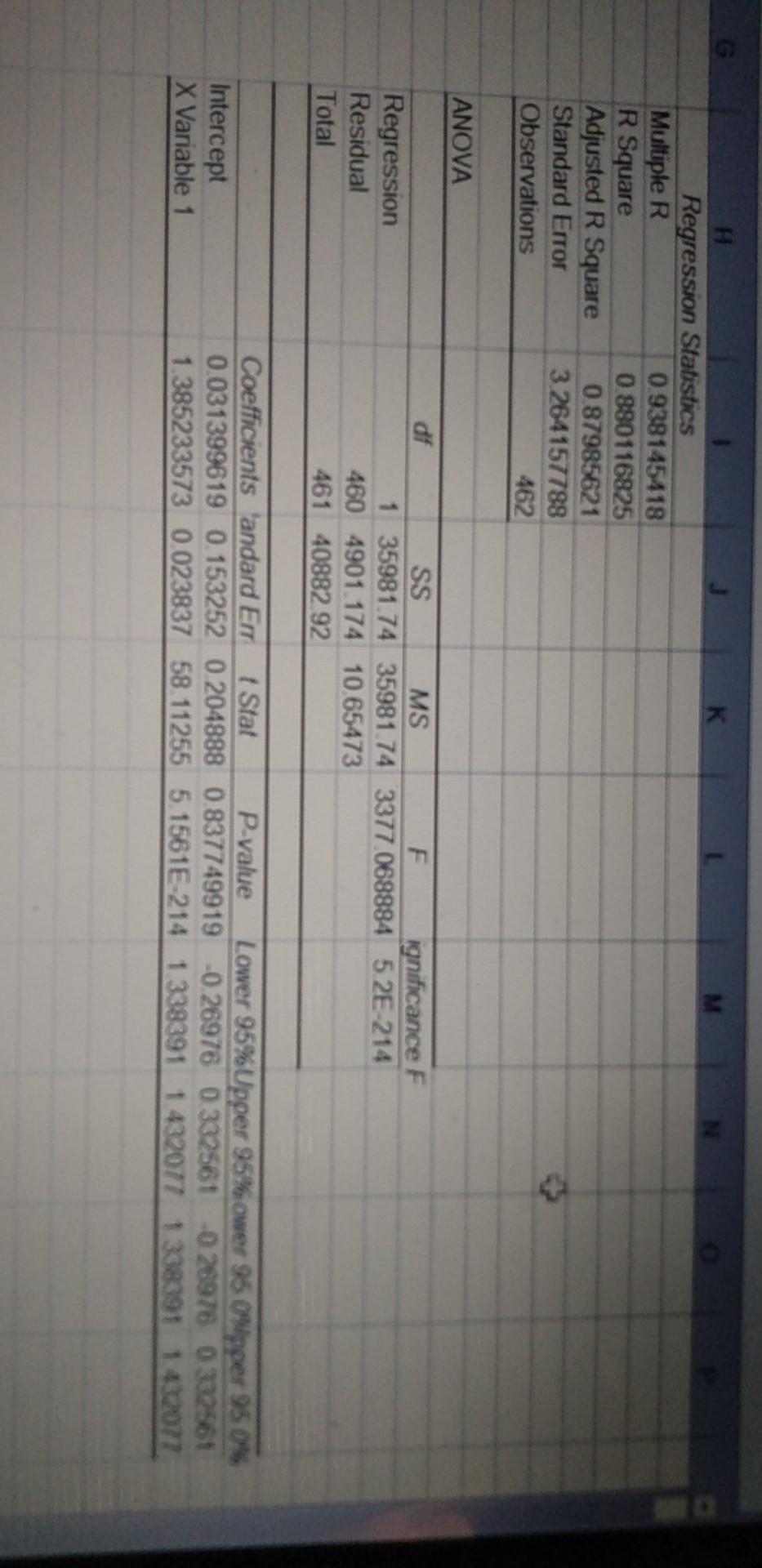

Question

refer to data spreadsheet, tab CAPM. Please run CAPM regression and select the CORRECT answer: Market beta is statistically insignificant in the model Intercept coefficient,

refer to data spreadsheet, tab CAPM. Please run CAPM regression and select the CORRECT answer:

Market beta is statistically insignificant in the model

Intercept coefficient, or Jensens alpha, is zero

Capital asset pricing model explains 75% variation in returns of the target portfolio

Market beta equals 1.16

K H Regression Statistics Multiple R 0.938145418 R Square 0.880116825 Adjusted R Square 0.87985621 Standard Error 3.264157788 Observations 462 ANOVA df Regression Residual Total SS MS F ignificance F 1 35981.74 35981.74 3377 069894 52E-214 460 4901.174 10.65473 461 40882.92 Intercept X Variable 1 Coefficients 'andard Errt Stat P-value Lower 95%Upper 95%ower 95 Olipper 95 0% 0.031399619 0.153252 0.204888 0.837749919 026976 0332561 -0.26978 0332561 1.385233573 0.023837 58.11255 5.1561E-214 1 338391 1 432077 1 338391 1432077 K H Regression Statistics Multiple R 0.938145418 R Square 0.880116825 Adjusted R Square 0.87985621 Standard Error 3.264157788 Observations 462 ANOVA df Regression Residual Total SS MS F ignificance F 1 35981.74 35981.74 3377 069894 52E-214 460 4901.174 10.65473 461 40882.92 Intercept X Variable 1 Coefficients 'andard Errt Stat P-value Lower 95%Upper 95%ower 95 Olipper 95 0% 0.031399619 0.153252 0.204888 0.837749919 026976 0332561 -0.26978 0332561 1.385233573 0.023837 58.11255 5.1561E-214 1 338391 1 432077 1 338391 1432077

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Foundations Of Business Analysis

Authors: M Douglas Berg

1st Edition

1465222030, 9781465222039