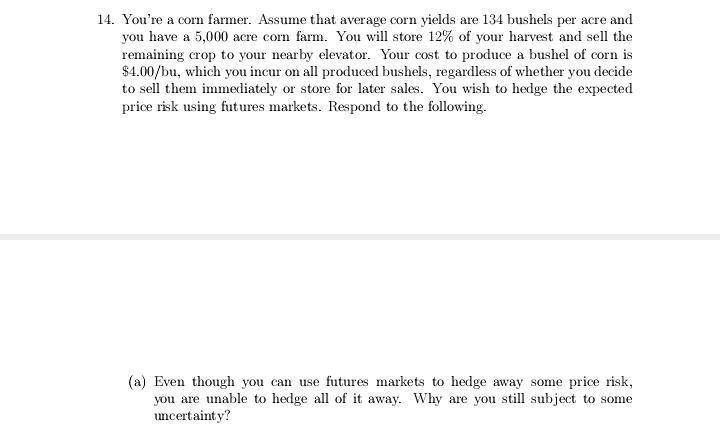

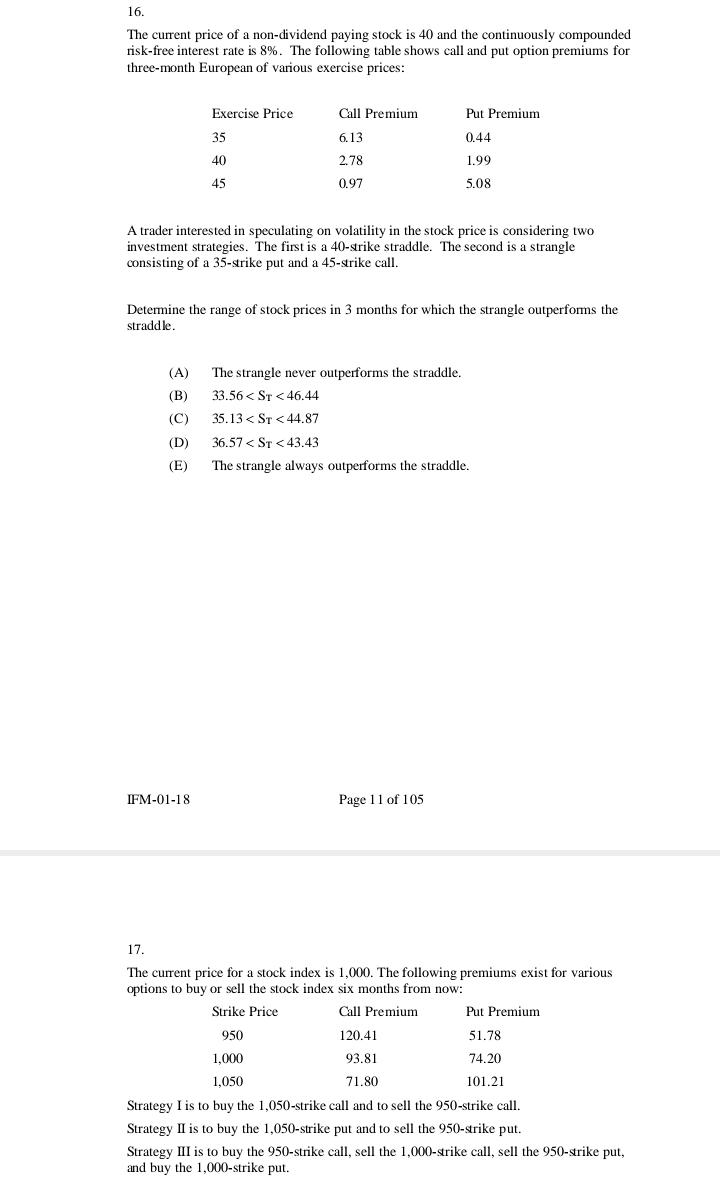

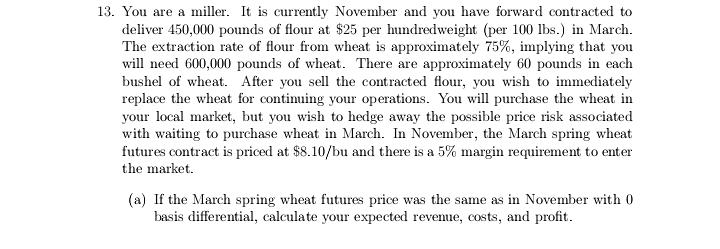

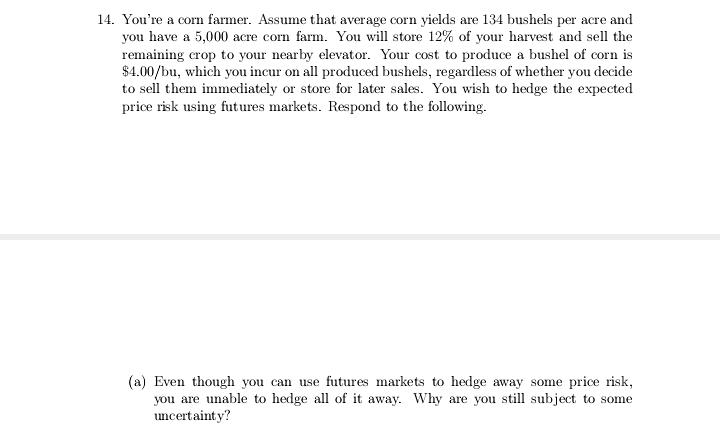

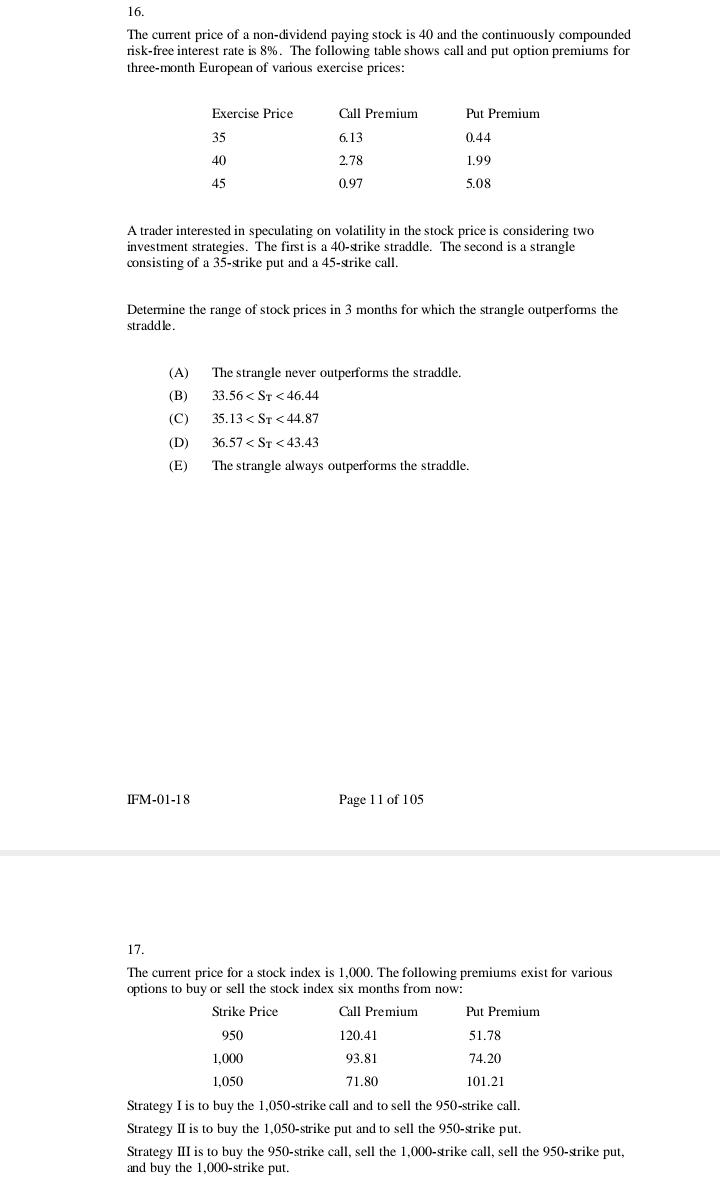

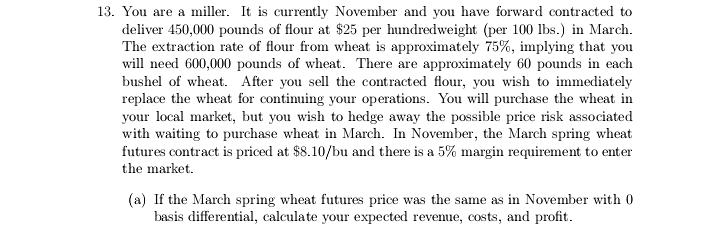

refer to the ..attachments.

30. True or False. Briefly explain. (a) The capital asset pricing model assumes that all investors have the same information and are willing to hold the market portfolio. (b) Over the long run, average returns on low-beta stocks have been less than predicted by the capital asset pricing model. 31. Suppose that the actual rate of return on the S&P 500 index from December 17, 2001 (today) to December 17, 2002 (12 months hence) is 9.0%, including dividends paid by companies in the index. You are given the following information about the performance of mutual funds X, Y and Z. Each mutual fund invests only in common stocks. Fund (manager) Rate of return Alpha (SE) Beta (SE) X (Gladys Friday) 9.8% +.48% (1.0%) 1.05 (.05) .92 Y (Gene Pool) 9.0% -.65% (3.0%) 1.10 (.07) .88 Z (Hugh Betcha) 13.4% +.50% (3.1%) 1.60 (.09) .65 Alphas and betas are estimated from 52 weekly returns from December 2001 to December 2002. Returns and alphas are given above as annual percentage returns. SE means standard error. The start-of-year risk- free rate is 2.5%. Based on these statistics, what can you say about the investment strat- egy and performance of each of the three managers? Explain. Consider risk as well as return before answering. 32. Your company offers three funds to its employees for their pensions: a money-market fund, an S&P 500 index fund and a new-economy equity fund. You need to form a portfolio from these funds for your own pension investments. The money-market fund is invested in 3-month Treasury bills, now with a risk-free return of 1.5% per annum. The index fund gives a premium of 8% and a standard deviation of 20% per annum. The new-economy fund's return can be described by the following equation: T1 - 1p = 0 + 3(rm - "p) + e where r, and ryne are the fund and market returns, ry is the risk-free return, a is a constant, and er is the part of the fund's returns not explained by the market. The performance of the fund over the last 60 months gives 39 0 2001, Andrew W, In and Jiang Wang 1.7 CAPM 1 QUESTIONS . 0 =0.0 . 3 = 1.2 . R2 = 0.75 (proportion of the variance of the fund's return ex- plained by the market return). (a) Compute the expected return of the new-economy fund using CAPM. Use reasonable estimates for the market return and the risk- free return. (b) If CAPM holds, what is the optimal portfolio to achieve an ex- pected return of 8% per annum. (c) If instead, the estimate of a is 0.0050 (0.5% per month) with a standard error of 0.0015. Without doing any calculations, discuss how this may affect your portfolio. 33. Two mutual fund managers are being evaluated for their performance in the last ten years. One of them, Mr. Hare, has achieved an eye-popping 34% annual average return; the other, Ms. Tortoise, has obtained a modest 12% annual average return. On closer examination of their portfolios, it is found that Mr. Hare always bet on risky Argentinian stocks (whose beta is 4), whereas Ms. Tortoise always invested in conservative technology firms like IBM (whose beta is (a) If the risk-free return was 3% every year and the expected mar- ket return was 11% every year, who should get the higher bonus? Why? (Credit only if reasoning is correct.)14. You're a corn farmer. Ass ume that average corn yields are 134 bushels per acre and you have a sum acre corn farm. You will store 12% of your harvest and sell the remaining crop to your nearly,r elevator. Your cost to produce a bushel of corn is $4fbu, which you incur on all produced bushels, regardless of whether you decide to sell them immediately or store for later sales. You wish to hedge the expected price risk using futures markets. Respond to the following. (a) Even though you can use futures markets to hedge away some price risk, you are unable to hedge all of it away. Why are you still subject to some uncertainty? 16. The current price of a non-dividend paying stock is 40 and the continuously compounded risk-free interest rate is 8%. The following table shows call and put option premiums for three-month European of various exercise prices: Exercise Price Call Premium Put Premium 35 6.13 0.44 40 2.78 1.99 45 0.97 5.08 A trader interested in speculating on volatility in the stock price is considering two investment strategies. The first is a 40-strike straddle. The second is a strangle consisting of a 35-strike put and a 45-strike call. Determine the range of stock prices in 3 months for which the strangle outperforms the straddle. (A) The strangle never outperforms the straddle. (B) 33.56