Reference: https://www.investopedia.com/terms/e/eps.asp You are a consultant who has been hired to advise your BSG firm. Your goal is to analyze the company's performance and make

You are a consultant who has been hired to advise your BSG firm. Your goalis to analyze the company's performance and make suggestions forimproving performance in the future.

Comapny Analyzing is called Company( F)Part I: Your first task is to analyze your firm's performance (good or bad) and identify Companytwo root causes. Part II: Your second task is to generate and analyze three potential solutions for improving performance in the future. You are not limited to BSG simulation actions; for instance, you may recommend an acquisition or foreign expansion. Part III: Next, you need to select the best option and justify its use as compared to the other options. Part IV: Finally, you must develop a plan for how the firm should implement the recommendation

TEMPLATE

Part I: Causes of Firm Performance

Financial Results

Report your firm's financial state as of the end of the simulation. Include the income statement, balance sheet, and cash flow report for the final period in a separate Excel spreadsheet. Describe these results here, and briefly discuss how they changed over time. Calculate relevant financial ratios for your firm in the spreadsheet, then report and describe the results here. Report how your stock price varied over the course of the simulation.

Analysis of Financial Performance

Analyze your firm's financial results, by comparing your stock price, financial ratios, and other financial results to relevant firms inside the Class Industry (other 9 teams)( Those companies are named as letters A through J). Based on comparing your results to others and to your own past performance, how would you characterize your financial position as of the end of the simulation?

Cause 1

Choose a root cause of your performance. Explain in detail (step by step) how that cause affected your stock price. Be as specific as possible and support your argument with details from BSG. For instance, if you say marketing expenditures caused your performance, then you should include details about how much you spent and why you concluded it was a problem. You'll probably need to look at the competition as well.

Cause 2

Same expectations as Cause 1.

Part II: Potential Solutions

Solution 1

Note: Your solutions and justification may be stronger if you do some outside research. Please be careful to follow the instructions for citing and quoting.

Make sure your solution is future and real-world oriented. Include details about the solution. For instance, don't just say we should pursue a market penetration strategy. Instead, explain exactly how you will pursue that strategy, including which market(s), which product(s), etc. Don't just say we need to do an alliance. Instead, identify an alliance partner and describe what you hope to gain from them. Talk about how this solution will address root causes and what effect you expect it to have on stock price and how. Support your arguments with specific data from the BSG simulation. For instance, if you expect your marketing solution to increase awareness, then you should talk about what the value is now and how you expect it to change relative to the competition.

Pros for Solution 1:

Cons for Solution 1:

Identify at least 2 pros and 2 cons . Make sure you've addressed any critical pros and cons.

Solution 2

Same expectations as Solution 1, but make sure the solution is different. The solutions can be mutually exclusive.

Pros

Cons

Solution 3

Same expectations as Solution 1, but make sure the solution is different. The solutions can be mutually exclusive.

Pros

Cons

Part III: Recommendation

Clearly state which solution you have selected. Justify your recommendation by comparing and contrasting the three alternate solutions, referring to the pros and cons you identified, and using specific data from the BSG simulation. For instance, if your recommendation was to create a blue ocean strategy, then map out the four actions and describe the value curve you would use. If your recommendation was to create new products, describe the products, target markets, etc.you could do a break-even analysis or calculate ROI. You could suggest a new strategy and map it out using the strategy diamond. ,

Part IV: Implementation

Resources & Capabilities

State which two resources and capabilities your firm needs to implement the recommendation and why they are necessary.

Tactics for Implementation

Identify two tactics you would recommend for implementing your solution. These should be specific "how to" steps that you believe are important for your firm to do.

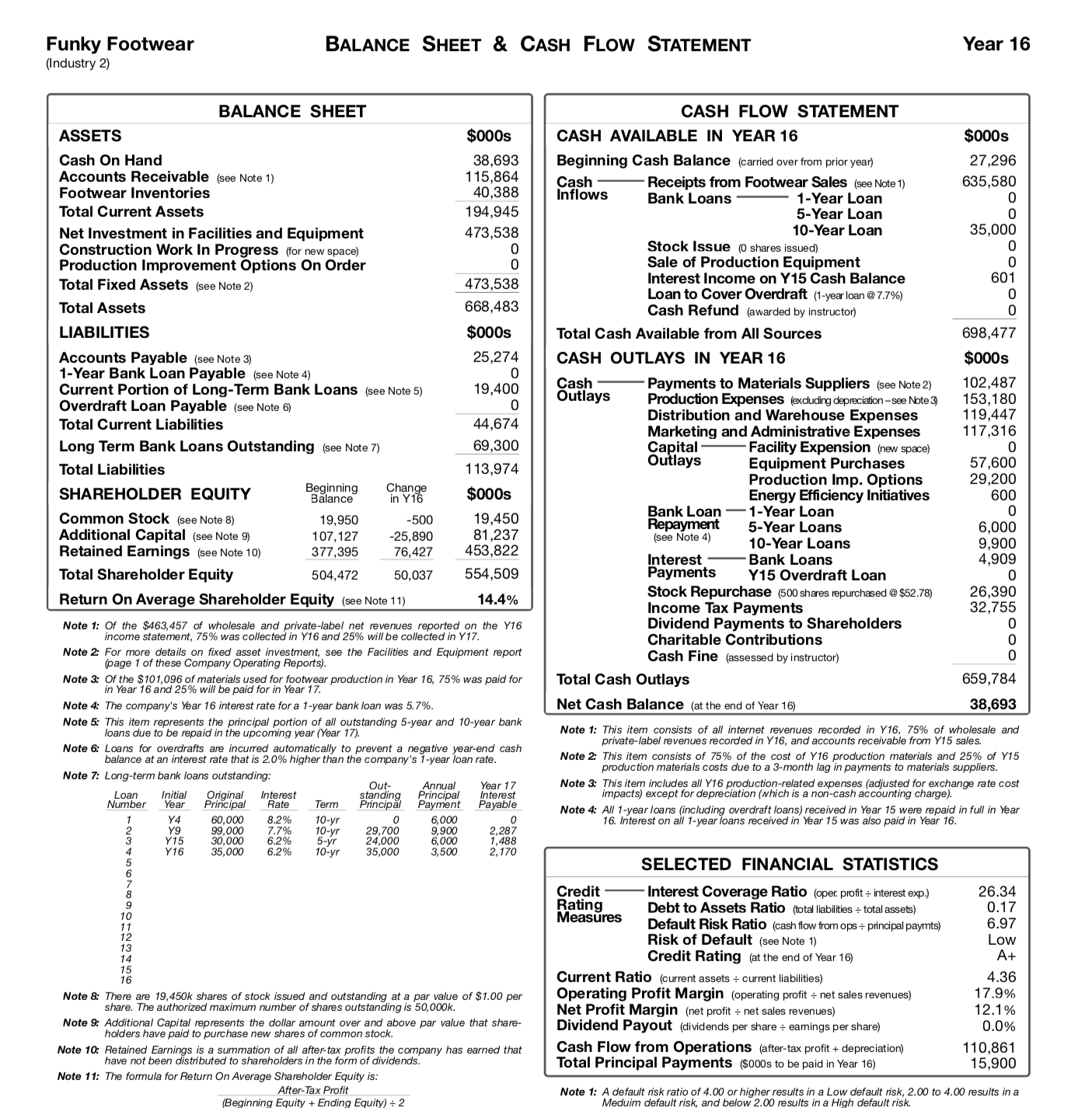

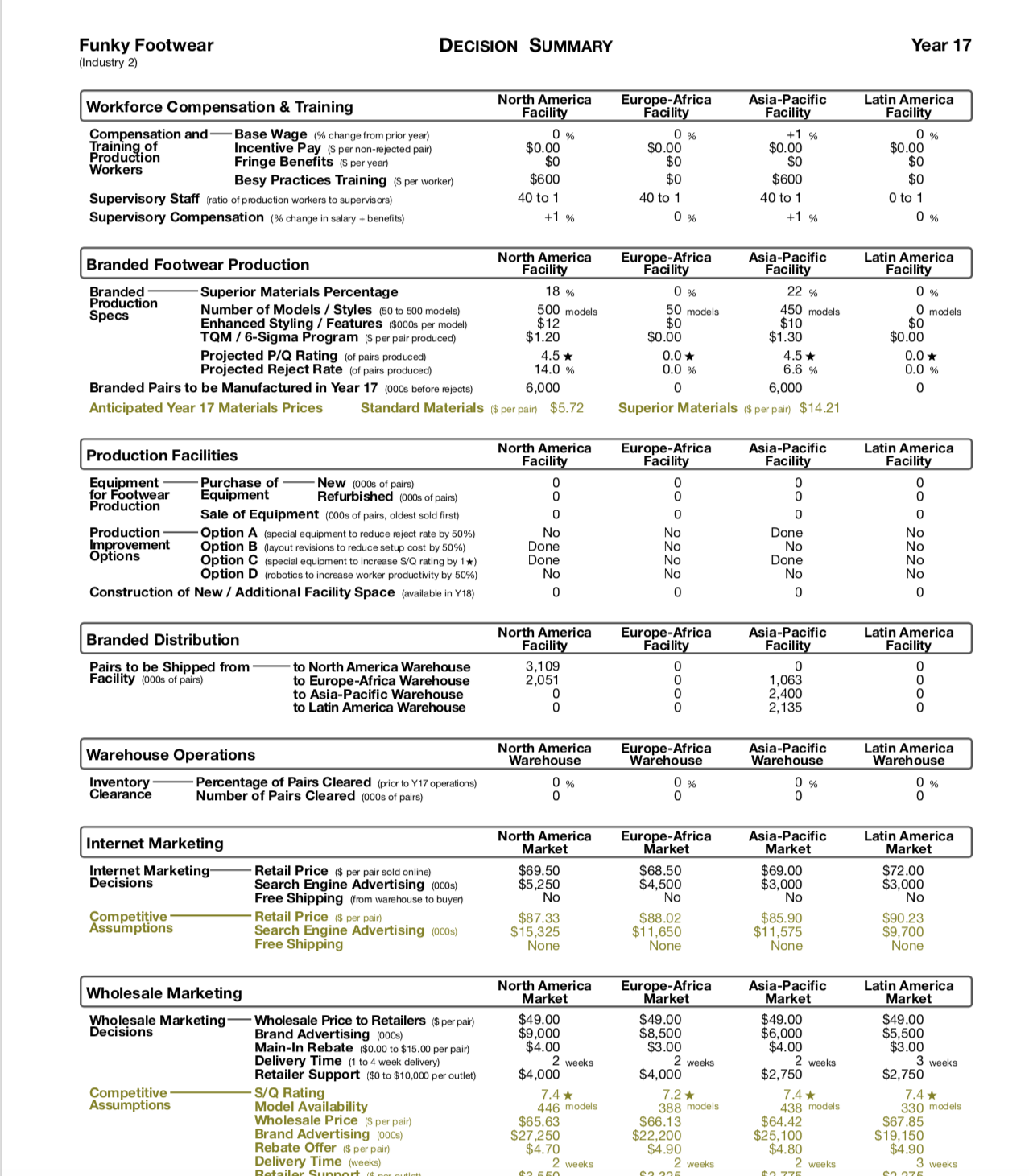

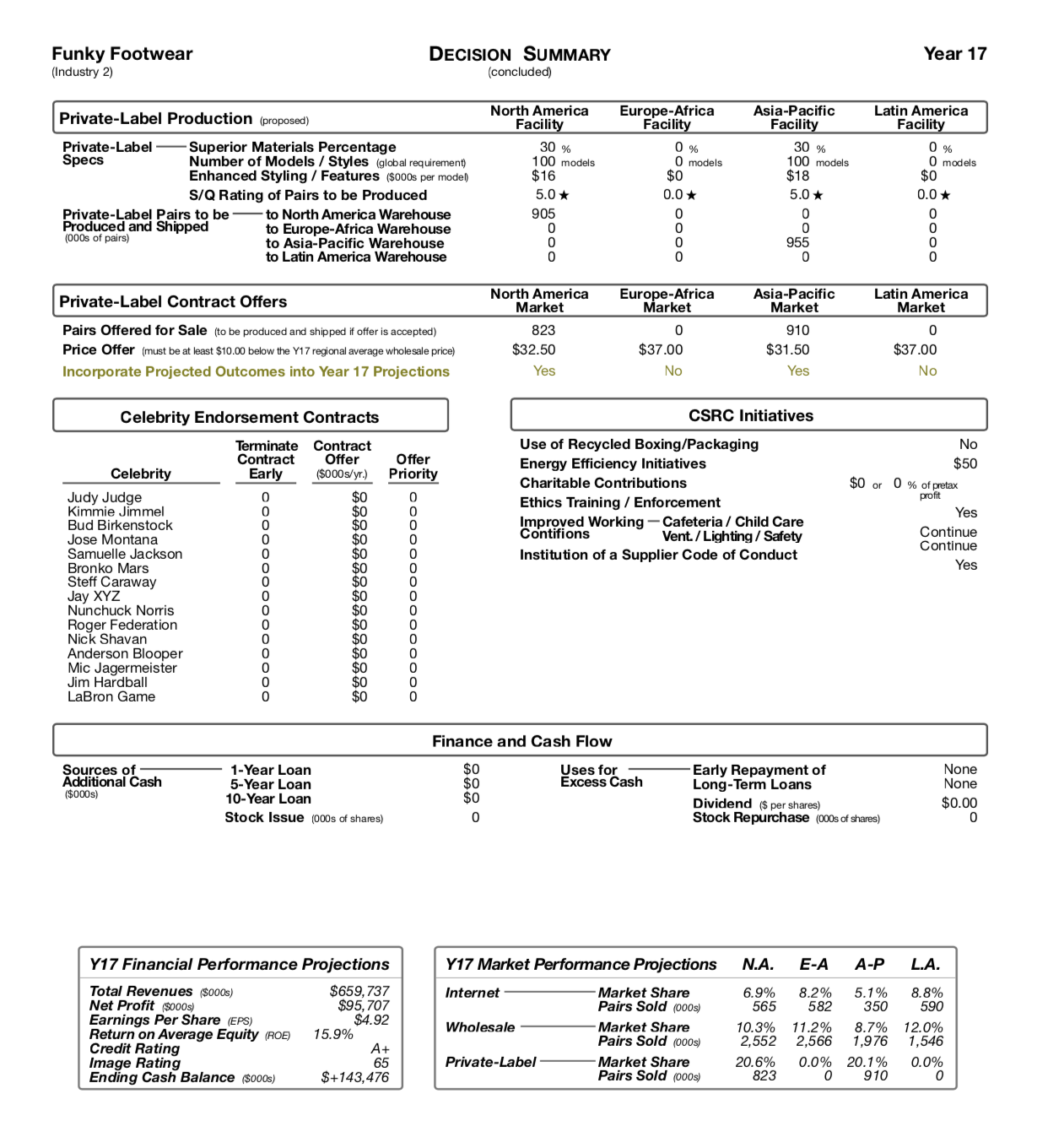

Funky Footwear BALANCE SHEET & CASH FLOW STATEMENT Year 16 (Industry 2) BALANCE SHEET CASH FLOW STATEMENT ASSETS $000s CASH AVAILABLE IN YEAR 16 $000s sh On Hand 38,693 Beginning Cash Balance (carried over from prior year) 27,296 Accounts Receivable (see Note 1) 15,864 Cash - 40,388 Receipts from Footwear Sales (see Note 1) 635,580 Footwear Inventories Inflows Bank Loans 1-Year Loan C Total Current Asset 194,945 5-Year Loan 0 Net Investment in Facilities and Equipment 473,538 10-Year Loan 35,000 Construction Work In Progress (for new space) Stock Issue (0 shares issued) 0 Production Improvement Options On Order Sale of Production Equipment 0 473,538 Interest Income on Y15 Cash Balance 601 Total Fixed Assets (see Note 2) Loan to Cover Overdraft (1-year loan @ 7.7%) 0 Total Assets 668,483 Cash Refund (awarded by instructor) 0 LIABILITIES $000s Total Cash Available from All Source 698,477 Accounts Payable (see Note 3) 25,274 CASH OUTLAYS IN YEAR 16 $000s 1-Year Bank Loan Payable (see Note 4) 0 Current Portion of Long-Term Bank Loans (see Note 5) 19,400 Cash Payments to Materials Suppliers (see Note 2) 102,487 Outlays Production Expenses (excluding depreciation -see Note 3) 153,180 Overdraft Loan Payable (see Note 6) Distribution and Warehouse Expenses 119,447 Total Current Liabilities 44,674 Marketing and Administrative Expenses 117,316 Long Term Bank Loans Outstanding (see Note 7) 69,300 Capital Facility Expension (new space) 0 Total Liabilities 1 13,974 Outlays Equipment Purchases 57,600 Production Imp. Options 29,200 SHAREHOLDER EQUITY Beginning Change Balance in Y16 $000s Energy Efficiency Initiatives 600 C Common Stock (see Note 8) 19,950 -500 19,45 Bank Loan 1-Year Loan Repayment 5-Year Loans 6,000 Additional Capital (see Note 9) 107, 127 25,89 81,237 ( see Note 4) 9.900 Retained Earnings (see Note 10) 377,395 76,427 453,822 10-Year Loans nterest Bank Loans 4.909 Total Shareholder Equity 504,472 50,037 554,509 Payments Y15 Overdraft Loan 14.4% Stock Repurchase (500 shares repurchased @ $52.78) 26,390 Return On Average Shareholder Equity (see Note 11) Income Tax Payments 32,755 Note 1: Of the $463,457 of wholesale and private-label net revenues reported on the Y16 Dividend Payments to Shareholders 0 income statement, 75% was collected in Y16 and 25% will be collected in Y17. Charitable Contribution Note 2: For more details on fixed asset investment, see the Facilities and Equipment report Cash Fine (assessed by instructor) 0 (page 1 of these Company Operating Reports). Note 3: Of the $101,096 of materials used for footwear production in Year 16, 75% was paid for Total Cash Outlay 659,784 Year 16 and 25% wil Note 4: The company's Year 16 interest rate for a 1-year bank loan was 5.7%. Net Cash Balance (at the end of Year 16) 38,693 Note 5: This item represents the principal portion of all outstanding 5-year and 10-year bank loans due to be repaid in the upcoming year (Year 17). Note 1: This item consists of all internet revenues recorded in Y16, 75% of wholesale and Note 6: Loans for overdrafts are incurred automatically to prevent a negative year-end cash private-label revenues recorded in Y16, and accounts receivable from Y15 sales. balance at an interest rate that is 2.0% higher than the company's 1-year loan rate. Note 2: This item consists of 75% of the cost of Y16 production materials and 25% of Y15 production materials costs due to a 3-month lag in payments to materials suppliers. Note 7: Long-term bank loans outstanding: Out- Annual Year 17 Note 3: This item includes all Y16 production-related expenses (adjusted for exchange rate cost Loan Initial Original Interest standing Principal Interest impacts) except for depr which is a non-cash accounting charge). lumber Year Principal Rate Term Principal Payment Payable Note 4: All 1-year loans (including overdraft loans) received in Year 15 were repaid in full in Year 2 Y4 60,000 8.2% 10-yr O 6,000 " 16. Interest on all 1-year loans received in Year 15 was also paid in Year 16. 99,000 7.7% 9,900 Y15 10-yr 29,700 6.2% 24,000 6,000 1,488 Y 16 30,00 35,000 6.2% 10 - yr 35,000 3,500 2, 170 SELECTED FINANCIAL STATISTICS Credit Interest Coverage Ratio (oper. profit + interest exp.) 26.34 Rating Debt to Assets Ratio (total liabilities + total assets) 0.17 Measures Default Risk Ratio (cash flow from ops + principal paymts) 6.97 Risk of Default (see Note 1) Low Credit Rating (at the end of Year 16) A+ Current Ratio (current assets + current liabilities) 4.36 Note 8: There are 19,450k shares of stock issued and outstanding at a par value of $1.00 per Operating Profit Margin (operating profit + net sales revenues) 17.9% share. The authorized maximum number of shares outstanding is 50,000k. Net Profit Margin (net profit + net sales revenues) 2.1% Note 9: Additional Capital represents the dollar amount over and above par value that share- Dividend Payout (dividends per share + eamings per share) 0.0% holders have paid to purchase new shares of commo Note 10: Retained Earnings is a summation of all after-tax profits the company has earned that Cash Flow from Operations (after-tax profit + depreciation) 110,861 have not been distributed to shareholders in the form of dividends. Total Principal Payments ($000s to be paid in Year 16) 15,900 Note 11: The formula for Return On Average Shareholder Equity is: After-Tax Profit Note 1: A default risk ratio of 4.00 or higher results in a Low default risk, 2.00 to 4.00 results in aFunky Footwear DECISION SUMMARY Year 17 (Industry 2 North America Europe-Africa Asia-Pacific Latin America Workforce Compensation & Training Facility Facility Facility Facility Compensation and Base Wage (% change from prior year) 0 % 0% +1 % 0% Training o ncentive Pay ($ per non-rejected pair) $0.00 $0.00 60.0 60.00 Production Fringe Benefits ($ per year) $0 $0 $0 $0 orkers Besy Practices Training ($ per worker) $600 $0 $600 $0 Supervisory Staff (ratio of production workers to supervisors) 40 to 1 40 to 1 40 to 1 to 1 +1% 0 % +1% 0% Supervisory Compensation (% change in salary + benefits) North America Europe-Africa Asia-Pacific Latin America Branded Footwear Production Facility Facility Facility Facility Branded Superior Materials Percentage 18 % 0% 22% 0 % Production 500 models 0 models Specs Number of Models / Styles (50 to 500 models) 50 models 450 models $12 $0 $10 $0 Enhanced Styling / Features ($000s per model) TQM / 6-Sigma Program ($ per pair produced) $1.20 $0.00 $1.30 $0.0 Projected P/Q Rating (of pairs produced) 4.5* 0.0* 4.5* 0.0* Projected Reject Rate (of pairs produced) 14.0 % 0.0% 6.6 % 0.0% Branded Pairs to be Manufactured in Year 17 (000s before rejects) 6,000 6,000 Anticipated Year 17 Materials Prices Standard Materials ($ per pair) $5.72 Superior Materials ($ per pair) $14.21 North America Europe-Africa Asia-Pacific Latin America Production Facilities Facility Facility Facility Facility Equipment Purchase of New (000s of pairs) o Doc for Footwear Equipment Refurbished (000s of pairs) Production 0 Sale of Equipment (000s of pairs, oldest sold first Production - Option A (special equipment to reduce reject rate by 50%) No No one No No mprovement Option B (layout revisions to reduce setup cost by 50%) one No No Options No Option C (special equipment to increase S/Q rating by 1 *) Done No one No No No No Option D (robotics to increase worker productivity by 50%) Construction of New / Additional Facility Space (available in Y18) North America Europe-Africa Asia-Pacific Latin America Branded Distribution Facility Facility Facility Facility Pairs to be Shipped from to North America Warehouse 3,109 O Facility (000s of pairs) to Europe-Africa Warehouse 2.051 1,063 ooo to Asia-Pacific Warehouse 2,400 to Latin America Warehouse 2,135 North America Europe-Africa Asia-Pacific atin America Warehouse Operations Warehouse Warehouse Warehouse Warehouse Inventory Percentage of Pairs Cleared (prior to Y17 operations) 0 % )% Clearance Number of Pairs Cleared (000s of pairs) North America Europe-Africa Asia-Pacific Latin America Internet Marketing Market Market Market Market Internet Marketing Retail Price ($ per pair sold online) $69.50 $68.50 $69.00 $72.00 Decisions Search Engine Advertising (000s) $5,250 $4,500 $3,000 $3,000 No No No No Free Shipping (from warehouse to buyer) Competitive Retail Price ($ per pair) $87.33 $88.02 $85.90 $90.23 Assumptions Search Engine Advertising (000s) $15,325 $1 1,650 $1 1,575 $9,700 Free Shipping None None None None North America Europe-Africa Asia-Pacific Latin America Wholesale Marketing Market Market Market Market Wholesale Price to Retailers ($ per pair) $49.00 49.00 $49.0 $49.0 Wholesale Marketing Decisions Brand Advertising (000s) $9,000 $8,500 $6,000 $5,500 Main-In Rebate ($0.00 to $15.00 per pair) $4.00 $3.00 $4.00 $3.00 Delivery Time (1 to 4 week delivery) 2 weeks 2 weeks 2 weeks 3 weeks Retailer Support ($0 to $10,000 per outlet) $4,000 $4,000 $2,750 $2,750 Competitive S/Q Rating 7.4* 7.2* 7.4* 7.4* Assumptions Model Availability 446 models 388 models 438 models 330 models Wholesale Price ($ per pair) $65.63 $66.13 $64.42 $67.85 Brand Advertising (000s) $27,250 $22,200 $25,100 $19,150 Rebate Offer ($ per pair) $4.70 $4.90 $4.80 $4.90 Delivery Time (weeks) 2 weeks 2 weeks 2 weeks 3 weeksFunky Footwear DECISION SUMMARY Year 17 (Industry 2 (concluded) North America Europe-Africa Asia-Pacific Latin America Private-Label Production (proposed) Facility Facility Facility Facility Private-Label Superior Materials Percentage 30 % 0 % 30 % 0 % Number of Models / Styles (global requirement) 100 models 0 models 100 models 0 models Specs $16 $0 $18 $0 Enhanced Styling / Features ($000s per model) 5.0* ).0* S/Q Rating of Pairs to be Produced ).0* 5.0* to North America Warehouse 905 0 Private-Label Pairs to be Produced and Shipped to Europe-Africa Warehouse 0 Doo Dood (000s of pairs) 0 955 to Asia-Pacific Warehouse to Latin America Warehouse North America Europe-Africa Asia-Pacific Latin America Private-Label Contract Offers Market Market Market Market Pairs Offered for Sale (to be produced and shipped if offer is accepted) 823 910 Price Offer (must be at least $10.00 below the Y17 regional average wholesale price) $32.50 $37.00 $31.50 $37.00 Incorporate Projected Outcomes into Year 17 Projections Yes No Yes No Celebrity Endorsement Contracts CSRC Initiatives NO erminate Contract Use of Recycled Boxing/Packaging Contract Offer Offer Energy Efficiency Initiatives $50 Celebrity Early ($000s/yr.) Priority Charitable Contributions $0 or 0 % of pretax profit Judy Judge $0 Ethics Training / Enforcement Yes Kimmie Jimmel $0 Bud Birkenstock $0 mproved Working - Cafeteria / Child Care $0 Contifions Vent. / Lighting / Safety Continue Jose Montana Continue ooooooo Samuelle Jackson $0 Institution of a Supplier Code of Conduct Yes Bronko Mars Steff Caraway Jay XYZ oooooooooooooo Nunchuck Norris 0 $0 Roger Federation Nick Shavan $0 Anderson Blooper ooooo Mic Jagermeister $0 Jim Hardball LaBron Game SO Finance and Cash Flow None Sources of - 1-Year Loan $0 Uses for Early Repayment of Non Additional Cash 5-Year Loan $0 Excess Cash Long-Term Loans ($000s) 10-Year Loan $0 Dividend ($ per shares) $0.00 Stock Issue (000s of shares) 0 Stock Repurchase (000s of shares) 0 Y17 Financial Performance Projections Y17 Market Performance Projections V.A. E-A A-P L.A. $659,737 Internet Market Share 6.9% 8.2% 5.1% 8.8% Total Revenues ($000s 582 59 Net Profit ($000s) $95, 707 Pairs Sold (000s) 565 350 Earnings Per Share (EPS) $4.92 Wholesale Market Share 10.3% 11.2% 8.7% 12.0% Return on Average Equity (ROE) 15.9% Pairs Sold (000s) 2,552 2,566 1,976 1.546 Credit Rating A+ Image Rating 65 Private-Label Market Share 20.6% 0.0% 20.1% 0.0% 823 910 Ending Cash Balance ($000s) $+143,476 Pairs Sold (000s)Funky Footwear BALANCE SHEET & CASH FLOW STATEMENT Year 16 (Industry 2) BALANCE SHEET CASH FLOW STATEMENT ASSETS $000s CASH AVAILABLE IN YEAR 16 $000s Cash On Hand 38,693 Beginning Cash Balance (carried over from prior year) 27,296 Accounts Receivable (see Note 1) 15,864 Cash Receipts from Footwear Sales (see Note 1) 635,580 Footwear Inventories 40,388 Inflows Bank Loans 1-Year Loan 0 Total Current Assets 194,945 5-Year Loar 0 Net Investment in Facilities and Equipment 473,538 10-Year Loan 35,000 Construction Work In Progress (for new space) Stock Issue (0 shares issued Production Improvement Options On Order Sale of Production Equipment 0 Interest Income on Y15 Cash Balance 601 Total Fixed Assets (see Note 2) 473,538 Loan to Cover Overdraft (1-year loan @ 7.7%) 0 Total Assets 668,483 Cash Refund (awarded by instructor) 0 LIABILITIES $000s Total Cash Available from All Sources 698,477 Accounts Payable (see Note 3) 25,274 CASH OUTLAYS IN YEAR 16 $000s 1-Year Bank Loan Payable (see Note 4) 0 102,487 Current Portion of Long-Term Bank Loans (see Note 5) 19,400 Cash Payments to Materials Suppliers (see Note 2) Outlays Overdraft Loan Payable (see Note 6) Production Expenses (exduding depreciation- see Note 3) 153,180 119,447 Total Current Liabilities 44,674 Distribution and Warehouse Expenses Marketing and Administrative Expenses 117,316 Long Term Bank Loans Outstanding (see Note ?) 69,300 Capital Facility Expension (new space) 0 Total Liabilities 113,974 Outlays Equipment Purchases 67,600 Production Imp. Options 29.200 SHAREHOLDER EQUITY Beginning Change $000s 600 Balance in Y16 Energy Efficiency Initiatives 19,450 Bank Loan 1-Year Loan 0 Common Stock (see Note 8) 19,950 -50 Repayment 6,000 Additional Capital (see Note 9) 107,127 25,890 81,237 (see Note 4) 5-Year Loans 10-Year Loans 9.900 Retained Earnings (see Note 10) 377,395 76,427 453,822 Interest Bank Loans 1,909 Total Shareholder Equity 504,472 50,037 554,509 Payments Y15 Overdraft Loan Stock Repurchase (500 shares purchased @ $52.78) 26,390 Return On Average Shareholder Equity (see Note 11) 14.4% Income Tax Payments 32,755 Note 1: Of the $463,457 of wholesale and private-label net revenues reported on the Y16 Dividend Payments to Shareholders 0 income statement, 75% was collected in Y16 and 25% will be collected in Y17. Charitable Contributions Note 2: For more details on fixed asset investment, see the Facilities and Equipment report Cash Fine (assessed by instructor) (page 1 of these Company Operating Reports). Note 3: Of the $101,096 of materials used for footwear production in Year 16, 75% was paid for Total Cash Outlays 659,784 in Year 16 and 25% will be paid for in Year 17. Note 4: The company's Year 16 interest rate for a 1-year bank loan was 5.7%. Net Cash Balance (at the end of Year 16) 38,693 Note 5: This item represents the principal portion of all outstanding 5-year and 10-year bank Note 1: This item consists of all internet revenues recorded in Y16, 75% of wholesale and loans due to be repaid in the upcoming year (Year 17). private-label revenues recorded in Y16, and accounts receivable from Y15 sales. Note 6: Loans for overdrafts are incurred automatically to prevent a negative year-end cash balance at an interest rate that is 2.0% higher than the company's 1-year loan rate. Note 2: This item consists of 75% of the cost of Y16 production materials and 25% of Y15 production materials costs due t rials suppliers. Note 7: Long-term bank loans outstanding: Out- Annual Year 17 Note 3: This item includes all Y16 production-related expenses (adjusted for exchange rate cost Loan Initial Original Interest standing Principal Interest impacts) except for depreciation (which is a non-cash accounting charge). Number Year Principal Rate Term Principal Payment Payable Note 4: All 1-year loans (including ov Year 15 were repaid in full in Year Y4 60,000 8.2% 10-yr 6.000 9 800 16. Interest on all 1-year loans received in Year 15 was also paid in Year 16. Y9 99,000 6.2% 5- YT 29.700 24,00 6,000 Y16 35,000 6.2% 10-yr 35,000 3,500 2, 170 SELECTED FINANCIAL STATISTICS EdDO VODAWN Credit Interest Coverage Ratio (oper. profit + interest exp.) 26.34 Rating Debt to Assets Ratio (total liabilities + total assets) 0.17 Measures Default Risk Ratio (cash flow from ops + principal paymts) 6.97 Risk of Default (see Note 1) Low Credit Rating (at the end of Year 16) A+ Current Ratio (current assets + current liabilities) 4.36 Note 8: There are 19,450k shares of stock issued and outstanding at a par value of $1.00 per Operating Profit Margin (operating profit + net sales revenues) 17.9% share. The authorized maximum number of shares outstanding is 50,000k. Net Profit Margin (net profit + net sales revenues) 12.1% Note 9: Additional Capital represents the dollar amount over and above par value that share- Dividend Payout (dividends per share + earnings per share) 0.0% holders have paid to purchase new shares of common stock. Note 10: Retained Earnings is a summation of all after-tax profits the c 1 10,861 m of diff company has eamed that Cash Flow from Operations (after-tax profit + depreciation) have not been distributed to shareholders in the form of dividends. Total Principal Payments ($000s to be paid in Year 16) 15,900 Note 11: The formula for Return On Average Shareholder Equity is: After-Tax Profit Note 1: A default risk ratio in a Low default risk, 2.00 to 4.00 results in a (BeginnIndustry 2 COMPARATIVE COMPETITIVE EFFORTS Year 16 Co. F VS North America Competitive Efforts by Company Industry Ind. A B C D E F G H I J Average Avg. INTERNET SEGMENT -20.4 % Retail Price ($ per unit) 95.50 80.00 80.34 91.00 90.00 69.50 88.00 91.00 98.00 89.99 87.33 Search Engine Advertising ($000s) 20,000 19,500 16,000 15,250 16,500 5,250 15,000 14,000 11,750 20,000 15,325 -65.7% Free Shipping No No No No No No No No No No None Near Avg S/Q Rating (1 to 10 stars 0.0* B.0* 6.4 8.0* 5.5* 4.5* 6.1* 7.8* 7.2* 10.0* 7.4* -39.2 % 50 483 499 470 495 494 490 493 498 446 490 +11.0% Model Availability 30,000 30,000 29,000 28,500 29,000 9,000 28,500 28,500 30,000 30,000 27,250 -67.0% Brand Advertising ($000s) 445 75 210 0 90 80 0 0 0 210 111 -27.9% Celebrity Appeal 100 83 91 60 69 77 83 71 100 81 -14.8% Brand Reputation (prior-year image) Online Orders (000s of pairs) 894 1,055 1,088 583 627 594 568 551 420 1,170 755 -21.3% Pairs Sold ($000s of pairs) 894 1,055 1,088 583 627 594 568 551 420 1,170 755 21.3% 11.8% 14.0% 14.4% 7.7% 8.3% 7.9% 7.5% 7.3% 5.6% 15.5% 10.0% Market Share (%) -2.1 pts. WHOLESALE SEGMENT 67.00 70.00 80.00 66.00 62.00 49.00 63.00 65.00 70.00 64.32 5.63 Wholesale Price ($ per pair) -25.3 % 10.0* 74 S/Q Rating (1 to 10 stars) 8 0* 6.4* 8.0* 5 5* 4.5* 61* 72+ 10.0* -39.2% 183 499 446 Model Availability 50 490 470 195 490 493 498 +11.0% 30,000 30,000 29,000 28,500 29,000 9,000 28,500 28,500 30,000 30,000 27,250 -67.0% Brand Advertising ($000s) Rebate Offer ($ per pair 5.00 5.00 5.00 5.00 5.00 4.00 5.00 4.00 5.00 4.00 4.70 14.9% Delivery Time (weeks) 2 wks 2 wks 1 wks 2 wks 2 wks 2 wks 2 wks 2 wks 1 wks 3 wks 1.9 wks +5.3% 6,500 1.000 750 3,500 4,000 4.000 4,000 4,000 2,000 5.750 3.550 +12.7% Retailer Support ($ per outlet) 576 731 528 1.540 1 032 871 1.552 1 282 789 4.469 1.537 -43.3% Retailer Outlets 0 0 210 111 -27.9% Celebrity Appea 145 75 210 0 90 80 100 91 79 60 69 77 83 71 100 81 -14.8% Brand Reputation (prior-year image) Pairs Demanded (000s of pairs) ,772 2,062 1,736 2,243 2 2,286 3,045 2,315 2,147 1,835 5, 150 2,659 +14.5% +96 +52 +44 +57 +58 -599 +59 +55 +47 Gained / Lost (due to stockouts) +131 Pairs Sold (000s of pairs) 3,868 2,114 1,780 2,300 2,344 2,446 2,374 2,202 1,882 5,281 2,659 .8.0 % 14.5% 8.0% 6.7 % 8.6% 8.8% 9.2 % 8.9% 8.3% 7.1 % 19.9% 10.0 0.8 pts. Market Share (% PRIVATE-LABEL SEGMENT Total Offer Price (maximum = $55.63) 34.99 0.00 70.00 44.00 32.00 3 0.00 32.99 55.00 37.00 Private-Label S/Q Rating (minimum = 5.0 stars) 5.0* 0.0* 5.7* 5.2* 5.5* 5.0* 0.0* 6.2* 5.8* 5.0* Pairs (000s) 443 Demand = 3,660 Pairs Offered / Available (000s) 1.182 0 1,675 387 634 823 0 1,431 1,886 Pairs Sold (000s) 732 0 634 732 732 732 Offered = 8,461 Sold = 3,562 Market Share (%) 20.0 % 0.0 % 0.0 % 0.0% 17.3% 20.0% 0.0% 20.0% 0.0 % 20.0% Note: A market share limitation of 20.0% was imposed by chain retailers to help reduce market domination by a few private-label suppliers and promote competition among more suppliers. INTERNET SEGMENT - NORTH AMERIC WHOLESALE SEGMENT - NORTH AMERICA High End High End A J A J A A B C B Price and S/Q Rating C Price and S/Q Rating G G E H F F Low 50 Models 500 Models Low 5 Models 500 Models Product Line Breadth Product Line BreadthSCORING MEASURES Year 16 Industry 2 Earnings Per Share ($ per share Earnings Per Share scores are based on a 20% (20-point) weighting. A bolded number indicates achievement of the investor expected EPS shown below each yearly column head. A highlighted number indicates best-in- industry performance. Game-To-Date EPS scores are based on a weighted average of the annual EPS performances. Y11 Y12 Y13 Y14 GLA Y16 Y17 Y18 Y19 Y20 Wgt. Avg. Y16 Score G-T-D Score I.E. B-I- 2.50 (3.00) (3.50) (4.00) 4.50) (5.25) (6.00) (7.00) (8.50) (10.00) (3.79) I.E. B-I-I 8.19 19.22 10.33 24 13.80 15.16 20 20 3.13 4.05 2.63 4.18 3.26 A 3.3 3.49 2.38 3.74 5.3 1.83 3.6 8.44 8.57 4.06 7.15 .13 4.74 4.80 5.15 4.53 4.05 1.09 0.65 1.92 0.70 0.66 0.80 0.97 HIATMDOWD CHIATMOOWD .55 3.2 3.41 3.99 3.93 3.12 0.37 0.5 1.29 3.51 5.37 2.16 1.94 4.61 3.9 3.30 3.34 3.04 1.13 3.99 3.21 3.88 -0.92 3.06 .10 2.21 6.95 9.59 12.83 14.72 B.17 Return On Equity (%) Return On Equity scores are based on a 20% (20-point) weighting. A bolded number indicates achievement of the investor expected ROE shown below each yearly column head. A highlighted number indicates best-in- industry performance. Game-To-Date ROE scores are based on a weighted average of the annual ROE performances. Y13 Y14 Y16 Y17 Y18 Y19 Y20 Wgt Avg. Y16 Score G-T-D Score Y12 Y15 (30.0) (24.0) I.E. B-I-I I.E. B-I-I (21.0 2.0 (23.0) (24.0 25.0) (26.0) (27.0) (28.0) (29.0) 26.0 26.9 42.2 51.7 41.9 43.6 41.2 24 20 27.1 5.2 7.2 11.1 13.3 13.1 14.9 40. 8.0 22.4 5.4 $4.9 23.1 19.0 24.6 26.8 21.4 18.8 16.0 19.9 14.5 4.8 4.3 5.0 7.1 GHIATMDOWD SOONNNVAD GHIATMDOWD 22.6 1.1 9.3 17.2 17.1 14.4 16.7 16.9 4.2 9.2 21.3 25.9 14.7 12.3 5.3 29.9 23.8 19.6 16.7 20.0 29.7 7.3 22.6 16.5 18.1 -4.3 17.3 5.8 15.2 36.4 36.7 36.5 34.3 32.9 Stock Price $ per share) Stock Price scores are based on a 20% (20-point) weighting. A bolded number indicates achievement of the investor expected stock price shown below each yearly column head. A highlighted number indicates best-in- industry performance. Game-To-Date scores are based solely on the most recent year's stock price Y1 Y14 Y15 Y16 Y17 Y18 Y19 Y20 Y16 Score G-T-D Score Y11 Y12 I.E. B-I-I (40.0 (50.00) (65.00) (100.00) (125.00) (150.00) (180.00) (215.00) (250.00) I.E. B-I-I (80.00) 59.49 85.77 222.11 397.56 409.38 519.43 20 20 62.17 44.06 38.60 16.18 37.59 33.76 148.11 186.73 254.60 185.70 172.01 74.91 53.42 21.87 94.90 86.91 85.60 58.58 IATMDOWD ATONW ALONG. InTmDOWD 12.20 5.79 8.47 5.16 5.11 5.06 34.59 3.99 38.61 48.89 51.46 37.80 15.85 6.56 5.21 6.79 58.61 99.66 2.32 15.86 92.25 39.09 34.86 25.87FINANCIAL PERFORMANCE SUMMARY Year 16 Industry 2 Income Statement Data $000s Net Sales Revenues Cost of Warehouse Marketing Admin Operating Interest Income Net Total Pairs Sold Expenses Expenses Expenses Profit Exp (Inc) Taxes Profit Internet Who t Wholesale P-label 112,055 1,492,578 481,291 97,307 395,693 31,070 487,217 11,525 142,708 332,984 337,201 1,024,332 377,803 95,586 214,432 23,223 189,790 44,306 43,645 101,839 323,136 577,698 0 900,834 385,776 490,327 0 876,103 365,772 103,432 224,342 24,219 158,338 45.350 33,896 79,092 24,215 137,555 4,149 38.821 90.583 206,611 579,946 109,445 912,722 195,763 66,718 188,471 209,052 359,000 44,190 612,242 297,523 59,381 162,721 20,869 71,748 44,004 5,823 15,921 CHIOTMDOWD WHITMOOWD 413,680 49,777 634,010 340,253 61,860 92,427 25,980 113,490 4,308 32,755 76,427 170,553 199,824 646,358 26,361 921,205 452,236 72,387 200,525 27,720 168,337 17,137 45,360 105,840 177,411 509, 1 17 24, 182 719,631 296,523 67,373 193,217 29.471 133,047 57,148 22,770 53, 129 515,826 0 689,189 328.291 71,694 179,206 24,469 85,529 100,740 -15,211 173,363 5.254 278,240 389,913 881,543 200,384 1,508,023 685,440 101,977 285,793 32,073 402,740 119,246 26,331 194,779 33,392 48,602 111,884 257,284 599,783 56,639 926.654 412,090 79,772 213,683 Selected Balance Sheet Data ($000s) Shareholder Equity Assets Liabilities Cash Current Fixed Total Current Long-Term Total Beginning Stock Sale Earnings Ending On Hand Assets Assets Assets Liabilities Loans Liabilities Equity (Purchase) Retained Equity 127,688 149,280 276,968 733,845 -273,880 332,984 792,949 0 314,583 755,334 1,069,917 1,434,283 219,298 445,400 664,698 785,094 -117,348 101,839 769,585 44,468 926,178 508, 105 1,533,571 104,911 448,603 653,515 989, 174 -88,210 79,092 980,056 62,562 810,383 723, 188 0 -69,249 259,032 370,668 629,700 68,337 30,000 98,337 600,612 531,363 no 192,000 399,849 310,420 15,921 326,341 426,477 726, 190 207,849 WHITMOOWD 3,815 299,713 WHITMOOWD 38,693 194,945 473,538 668,483 44,674 69,300 113,974 504,472 -26,390 76,427 554,509 365,149 -17,850 105.840 453,139 7,738 302,476 530,021 832,497 88,558 290.800 379,358 451,048 1,140,500 188,845 647,000 835,845 332,906 -81,380 53,129 304,655 75,618 689,452 518,133 1,692,543 811,374 531,200 1,342,574 365, 180 0 -15,211 349,969 0 1,174,410 759,975 1,132,962 109,410 200,000 309,410 801,046 -232,105 254,611 823,552 42,560 372,987 578,790 588,612 27,545 534,416 551,649 1,086,065 197,094 300,358 497,453 -83,716 93,538 Selected Financial Statistics Profitability Measures Dividend Data Credit Rating Measures Shares Risk of Stock Gross Operating Net Div. Per Total Div. Payout Interest Debt to Default Current Days of Outstanding Profit Profit Profit Share Payment (percent of Coverage Assets Risk Margin Margin Margin $/share) ($000s) net profit) Ratio Ratio Ratio Default Ratio Inventory (000s of shares) 67.8% 32.6% 22.3% 0.00 0.0% 42.27 0.26 5.57 Low 2.46 28 days 17,323 0.00 0.0% 4.28 0.46 0.95 High 4.22 677 days 24,374 58.1% 21.1% 1 1.3% 0.0% 3.49 0. 36 1.25 High 7.72 617 days 19,500 58.3% 18.1% 9.0% 0.00 19,979 45.7% 15.1% 9.9% 8.00 159,832 176.6% 33.15 0.16 3.23 Mediu 1.79 81 days m 0.0% 0.55 0.24 11.7% 2.6% 0.00 1.63 High 1.44 279 days 20,000 WHIGTM DOWD 51.4% 46.3% 17.9% 12.1% 0.00 0.0% 26.34 0.17 6.97 Low 4.36 51 days 19,450 1 1.5% 0.00 0.0% 9.82 0.46 5.21 Low 3.42 125 days 19,700 WHIGTIM 50.9% 18.3% 7.4% D.00 0.0% 2.33 0.73 0.30 High 3.65 594 days 15,898 58.8% 18.5% 0.06 High 1.45 1,180 days 16,449 52.4% 12.4% -2.2% 0.00 0.0% 0.85 0.79 54.5% 26.7% 18.5% 1.25 23,629 8.5% 76.65 0.27 8.32 Low 3.41 39 days 18,903 55.5% 21.0% 12.1% 0.93 18,346 18.5% 20.08 0.42 3.21 3.59 367 days 19,158

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance