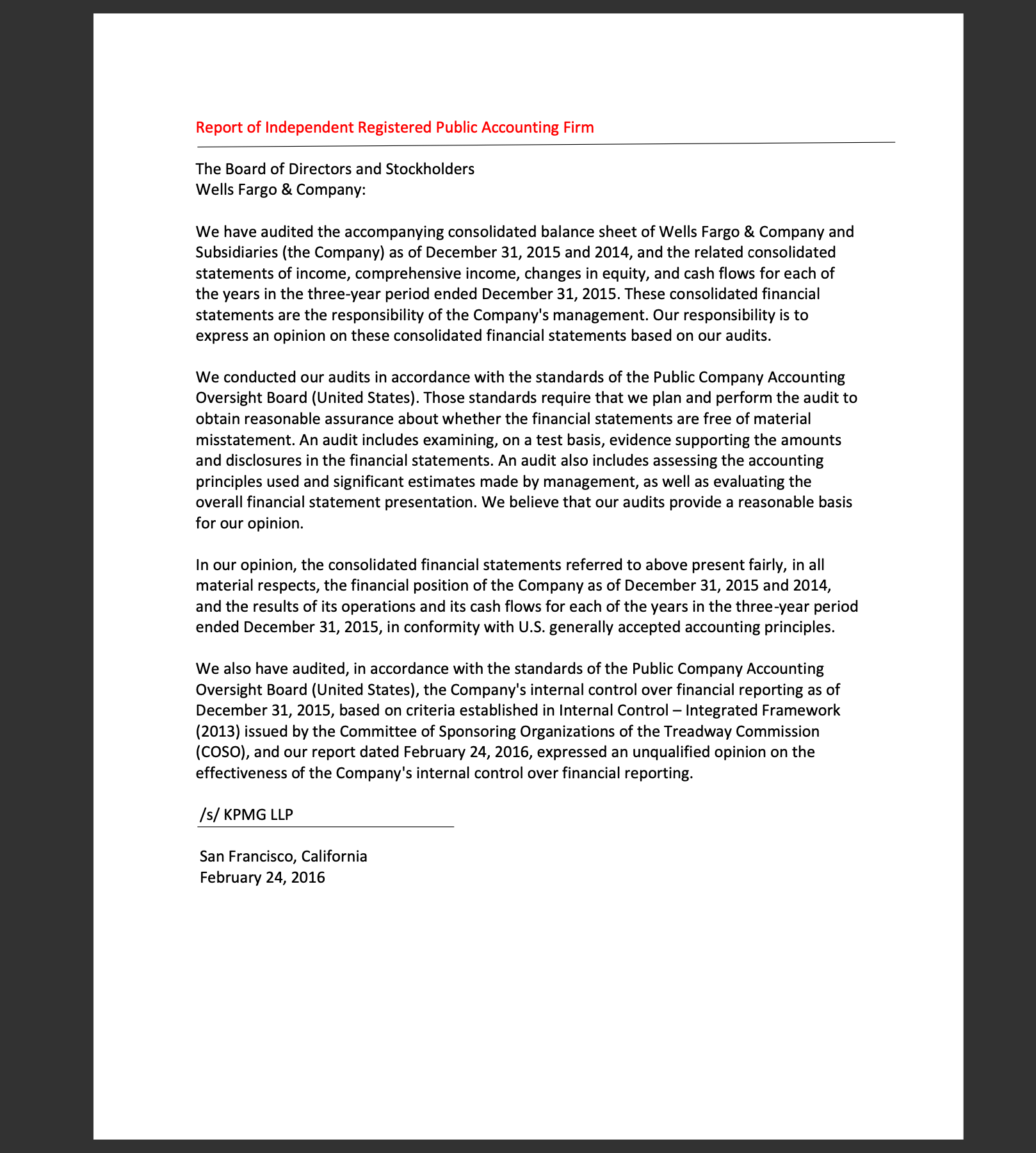

Report of Independent Registered Public Accounting Firm The Boa rd of Directors and Stockholders Wells Fargo & Company: We have audited the accompanying consolidated balance

Report of Independent Registered Public Accounting Firm The Boa rd of Directors and Stockholders Wells Fargo & Company: We have audited the accompanying consolidated balance sheet of Wells Fargo & Company and Subsidiaries (the Company} as of December 31, 2015 and 2014, and the related consolidated statements of income, comprehensive income, changes in equity, and cash flows for each of the years in the three-year period ended December 31, 2015. These consolidated financial statements are the responsibility of the Company's management. Our responsibility is to express an opinion on these consolidated financial statements based on our audits. We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion. In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the financial position of the Company as of December 31, 2015 and 2014, and the results of its operations and its cash flows for each of the years in the three-year period ended December 31, 2015, in conformity with US generally accepted accounting principles. We also have audited, in accordance with the standards of the Public Company Accounting Oversight Board (United States), the Company's internal control over financial reporting as of December 31, 2015, based on criteria established in Internal Control Integrated Framework (2013) issued by the Committee of Sponsoring Organizations of the Treadway Commission (C050), and our report dated February 24, 2016, expressed an unqualified opinion on the effectiveness of the Company's internal control over financial reporting. [5/ KPMG LLP San Francisco, California February 24, 2016 WELLS FARGO: DID KPMG PERFORM ITS DUTIES? AN AUDITING CASE ABOUT CONSUMER FRAUD Nancy Chun Feng ii, Ross D. Fuennan M, Nicole Heron * " Sawyer Business School, Suffolk University, Boston, the USA ** Corresponding author, Sawyer Business School, Suffolk University, Boston, the USA Contact details: Sawyer Business School, Suffolk University, 120 Tremont Street, Boston, MA 0210872770, the USA Abstract OPEN 8 ACCESS How to cite this paper: Fang, N. C., Fuennan. R. D.. 8: Heron. N. (2022). Wells Fargo: Did. ICPMG perform its duties? Anaudiiing case about consumer fraud. Corporate Ownership :5 Control, 19(2), 121128. htips://dai.org/IO.22495/cocv1Bi2art10 This article describes the implementation of a case study that uses as its setting the role of KPMG in the Wells Fargo consumer fraud scandal as a way for students to learn about what can happen during an audit failure and what should be done to prevent audit failure. As the case details illustrate, it features the only recent signicant Big 4 audit failure that is still being resolved. the audit failure includes many aspects of an auditor's job, including some that typically are not covered in traditional course textbooks, and it highlights the auditor's role within the broader context of Copyright 2022 The Authors This work is licensed under a Creative Commons Attribution 4.0 International License (cc BY 4.0). corporate governance. This case study exposes students to several TEE/\"creativemmm'e\"lg/licemes/hv/ auditing standards and laws related to 1) consumer fraud; 2) contingent liabilities; 3) materiality: 4) illegal acts: 5) audit evidence; 5) audit opinions; 7) auditor independence and mandatory rotation: 8) auditor liability under the Securities Act of 1933: and 9) auditor liability under the Securities Exchange Act of 1934. The case was used in two undergraduate auditing classes and a graduate auditing class. Student opinion surveys were used to ascertain the learning outcomes of the case study. The survey results suggest strong student engagement and support for learning in groups while collaborating on the case study. The case results also show particularly strong knowledge enhancement with regard to understanding the auditor's duty to disclose illegal acts, understanding consumer fraud, understanding audit evidence, understanding materiality. and understanding contingent liabilities. [SEN Online: 1810-305? [SSN Print: [721-9232 Received: 20.04.2021 Accepted: 18.02.2022 151- Classication: M420, M480, K420 DOI: 10.22405/cocv19i2ar110 Keywords: Illegal Acts, Consumer Fraud, Audit Evidence, Materiality, Contingent liabilities, Auditor Regulation Authors' individual contribution: Conceptualization i R.D.F.; Methodology R.D.F.; Investigation R.D.F.; Writing Original Draft R.D.F.; Writing Review 8.: Editing N.C.F. and N.H.; Supervision R.D.F. Declaration of conicting interests: The Authors declare that there is no conict of interest. 1. INTRODUCTION The Wells Fargo unauthorized accounts scandal first became public in the Los Angeles Times (Reckard, 2013). The Los Angeles City Attorney filed a complaint (The Office of the City Attorney, 2015). The fraud began by 2002 and continued to 2016. Hundreds of thousands of bank employees opened 3.5 million accounts, issued products or services, or transferred customer funds, without the customer's consent. Senior executives set intentionally unrealistic sales goals and placed unreasonable pressure on rank-and-file employees to meet those goals. They intimidated and badgered employees, subjecting them to hazing-like abuse, and threatened to terminate and actually terminated employees for failure to meet the goals. Senior executives believed that the more accounts, products and services per customer, the greater the bank's profitability and executive compensation would be. In the first part of the fraud. Wells Fargo and its semor executives perpetrated a consumer fraud. which is a fraud that victimizes Consumers. it includes identity theft, elder fraud, advance fee schemes, credit card fraud, mortgage fraud, collectibles fraud. and fraudulent business practices. In the second part of the fraud. since Wells Fargo did not disclose its consumer fraud, Wells Fargo and its management perpetrated a financial reporting fraud. By 2021, Wells Fargo had settled its lawsuits but many of the proceedings against its management and board of directors are still ongoing. The Securities and Exchange Commission (sec) is litigating against head of community bank Carrie Tolstedt for unspecified disgorgement and monetary penalties (SEC. 2020). The Office of the Comptroller of the Currency (OCC) is also litigating against Tolstedt for $25,000,000 (OCC, 2020). Furthermore. it is seeking an additional $5,000,000 from Community Bank Group Risk Officer Claudia R. Anderson (it already collected 33.000.000). an additional $5,000,000 from chief auditor David Julian (it already collected $2,000,000]. and an additional $1,000,000 from executive audit director Paul McIJnko (it already collected $500,000) (Wack. 2021a). Members of the board are being sued for havmg produced abiased report whitewashing themselves of responsibility for the scandal (Wack. 2021b). The study is structured as follows. Sectionl contains an introduction. Section2 and SectionS cover the description of the case and its major questions. Section4 describes a teaching strategy and case implementation guidance. Section 5 presents the conclusions and limitan'ons of the study 2. DESCRIPTION OF THE CASE 2.1. Contingent liabilities Companies scrutinize their potential liabilities. Some events are determined to be probable to cause the company to pay out a material amount of cash in the future. These are liabilities, unless the company cannot determine the amount or at least a reasonable range (in which case it is a contingent liability). For some events, it is remote that the company will pay out cash. Then these are not liabilities: they are ignored as immaterial. There are also contingent liabilities. This is when it is reasonably possible that the event will result in the company paying out a material amount of cash in the future. Because of the uncertainty, line item inclusion is not required. Instead, footnote disclosure is required. 2.2. Materiallty Senator Elizabeth Warren wrote that \"your firm's failure to identify the illegal behavior at Wells Fargo raises questions about the quality of your audits..." (Warren, Sanders, Hirono, er Markey, 2016. p.2). KPMG'S CEO admitted the audit firm knew all about the consumer fraud since at least 2013. However. she argued KPMG did not need to ask the management of Wells Fargo to disclose the consumer fraud because KPMG believed that the consumer fraud was not material when KPMG signed its audit opinion on February 24. 2016 (Doughtje. 2016). Senators Warren and Markey disagreed and asked the Public Company Accounting Oversight Board (PCAOB) to investigate KPMG for its audits of Wells Fargo (Warren 8i Markey. 2017). The PCAOB states that a fact is material if areasonable investor would regard the fact as having significantly altered the total mix of Information made available (PCAOB, 2010b]. In the past generation. a wider group of people has also become regarded as stakeholders of a public corporation: a firm's employees. its customers. its suppliers, its regulators, and the communities affected by the firm. These additional people, because they are stakeholders, are also entitled to correct financial reporting The key events and quantifiable costs to Wells Fargo for the unauthorized accounts scandal are listed in Table I. Table 1. The key events and quantifiable costs to Wells Fargo for the unauthorized accounts scandal Quantiobia cons Kay events The lA Times article about the unauthorized accounts published on December 21 2013. begin aftcr the LA Times article. Investigations by Los Angclcs (LA) City Attomcy. Consumer Financial Protection Bureau (CFFB). and OCC LA City Altai-ire complaint filed on May 4 2015. t142 000 000 Wells Fargo customer complaint tiled May 14 2015. Settlement on July is 2017. 3165 000 000 Settlement wtth LA City Attorney CFPB and occ on September 8 2016. 51 000 000 000 CFPB and OCC additional settlement on April 20 2018. 53.nno.oon,nno Investigations by sec and Department of Justice (DUI) began in Fall 2016. Settlement on Fcbruary 21. 2020 includes dcfcrrcd prosecution agreement. 5480 not) not) Securities class action riled on September 26 2016. Settlement on September 4 2018. EM 000 000 Deceptive unneeded car loan insuranc e class action filed on July 30 2017. Settlement on June 6 2019. 5575 000.000 Fifty states and District of Columbia begin investigation in Fall 2017. Settlement on December 28, 2018. :5 776,000 000 source: Authori' elaboration. The Los Angeles (LA) City Attorney sought $5000 per unauthorized account. which later were estimated to total $3,500,000. Thus. it sought penalties of 517.500.000.000. Later. the Federal Reserve and the OCC imposed restrictions on Wells Fargo that reduced its ability to grow. and the Department of Justice (DOJ) imposed a deferred prosecution agreement. also limiting Wells Fargo's ability to grow As a result. Wells Fargo stock performed far worse than any of its industry sector competitors and has continued to underperform through 2021. Many of the materiality factors discussed above related to the Wells Fargo scandal are qualitative o mi met min f 122 rather than quantitative, but some quantification is possible. The 35.776.000.000 in direct costs shown above for the settlements, compared to the \"2,894,000,000 of net income of Wells Fargo for the year ended in December 31, 2015, represent an overstatement of net income of 25%. The Sl7,500,000,000 in penalties demanded in the May 4. 2015, LA City Attorney complaint represent an overstatement of net income of 76%. 2.3. Audit evidence Auditors of public companies must obtain reliable evidence. The PCAOB's AS 1105.08 states that \"evidence obtained from a lmowledgeable source that is independent of the company is more reliable than evidence obtained only from internal company sources" (PCAOB. 2010a) AS 1105129. however. states that \"if audit evidence obtained from one source is inconsistent with that obtalned from another. or if the auditor has doubts about the reliability of information to be used as audit evidence. the auditor should perform the audit procedures necessary to resolve the matter and should determine the effect. if any. on other aspects of the audit" (PCAOB, 2010a). Wells Fargo's auditor did not appear to have relied on any evidence other than that provided by Wells Fargo and its law firms. Consequently, the auditor concluded that the materiality threshold for footnote disclosure of the pending lawsuits and investigations regarding the unauthorized accounts scandal was not met 2.4. Illegal am When auditors of public companies discover an illegal act, they should consider such required responses as: 1. Investigation and report to management. if, in the course of conducting an audit pursuant to this paragraph(1) to which sulrpointtLA) applies, the registered public accounting firm detects or otherwise becomes aware of information indicating that an illegal act (whether or not perceived to have a material effect on the nancial statements of the issuer) has or may have occurred. the firm shall. in accordance with generally accepted auditing standards, as may be modified or supplemented from time to time by the cammttsl'orl'. to: LA. (i) Deternune whether it is likely that an illegal act has occurred; and (ii) If so, determine and consider the possible effect of the illegal act on the financial statements of the issuer, including any contingent monetary effects. such as fines. penalties, and damages; LB. As soon as practicable, inform the appropriate level of the management of the issuer and assure that the audit committee of the issuer, or the board of directors of the issuer in the absence of such acomuuttee. is adequately informed with respect to illegal acts that have been detected or have otherwise come to the attention of such firm in the course of the audit, unless the illegal act is clearly inconsequential. 1 tom/1W law cor-tic\" cdu/dcfluitmm/uscndc php'N/idihutkhuyitt Ostifnmcriruc&dcfiidrlSVUSCV128323762!72067023497Aicmiioccut =W9hmmislv=|ltlc l5 chapter 11? mini. 7XJ"/iE2"/i80"/i93l 2. Response to failure to take remedial action. If. after determining that the audit committee of the board of directors of the issuer. or the board of directors of the issuer irl the absence of an audit committee, is adequately informed with respect to illegal acts that have been detected or have oLherwise come to the attention of the rm in the course of the audit of such firm, the registered public accounting mt' concludes that: 21A. The illegal act has a material effect on the financial statements of the issuer; 2.8. The senlor management has not taken, and the board of directors has not caused seruor management to take. timely and appropriate remedial actions with respect to the illegal act; 21C. The failure to take remedial action is reasonably expected to warrant departure from a standard report of the auditor, when made. or warrant resignation from the audit engagement; the registered public accounting rm shall, as soon as practicable. directly report its conclusions to the board of directors. 3.Noti'ce to commission; mpome to failure to notify. An issuer whose board of directors receives a report under paragraph (2) shall inform the commission by notice not later than one business day after the receipt of such report and shall furnish the regstered public accounting firm making such report with a copy of the notice furnished to the commission. If the registered public accounong rm fails to receive a copy of the notice before the expiration of the required one-business- dav period, the registered public accounting rm shall: 3.A. Resign from the engagement; or 3.13. Furnish to the commission a copy of its report [or the documentation of any oral report given) not later than one business day following such failure to receive notice. 4. Report after resignation. if a registered public accounting firm resigns from an engagement under sub-poinlBA) the rm shall. not later than one business day following the failure by the issuer to notify the commission under paragraph (3), furnish to the commission a copy of the report of the firm (or the documentation of any oral report given). 5. Auditor liability limitation. No registered public accounting firm shall be liable in a private action for any finding. conclusion, or statement expressed in areport made pursuant to sub-point(3.B) or paragraph (4), including any rule promulgated pursuant thereto (Securities Btchange Act of 1934', section 10A, pp. 91796). 3. CASE QUESTIONS The questions to this case are formulated as follows: 1) What is consumer fraud? Give five examples of consumer fraud. You can find examples at the Consumer Financial Protection Bureau [CFPB)'. 2) what is the three-part analysis of every potential liability that must be performed? Does 1 hllps waw law comm oduldcmilomruscudi: pnpwiottiexonahnghean DAlfmmL'tmckdcfiltkl 5~USC-I 283306352-2067023625Mcmiioccur =999arormrsicaitlo ls chapterzzb tccllon 7si%bz%xo%9ai 3 hllps waw govinfo gnvlconicnt/pkyCOMPS- I Elli/pdf/COMPS- I its out ' httpsz/lwwwsoiisiiiiicrtiiiiice govInkrtfph/whahslcrsomt'rconunonslypcs ol-scams-cn-ZO'JZ/ o 7731 ms: VIK up} 12} a contingent liability get ignored, get recorded (line item inclusion), or footnote disclosure? You can nd more information on contingent liabilities in intermediate accounting texts. or in auditing texts. 3) On February 24. 2016. when KPMG signed its audit opinion on the Wells Fargo financials for the year ending December 31. 201 S. was there a contingent liability? Wells Fargo did not disclose the unauthorized accounts scandal. Should KPMG have demanded that Wells Fargo disclose the unauthorized accounts scandal? Note that theLA City Attorney complaint had been available since May 4, 2015 (The Office of the City Attorney, 2015). Apply the facts of the case to the literature on materiality, including the broad group of stakeholders of a public corporation. 4) Answer the following questions on illegal acts. using the case material above. and section 10A of the Securities Exchange Act of 1934. What is the auditor supposed to do first if he believes that an illegal act occurred? Does it matter whether it is adircct illegal act or indirect illegal act? What is the auditor supposed to do if the company, after being notied, does not promptly notify the SEC about an illegal act that has a material effect on the company's financial statements? Is the auditor in that situation supposed to make the disclosure of the illegal act to the SEC? If the auditor makes this disclosure to the SEC can the auditor be sued by the company? Did KPMG perform its illegal acts duties while auditing Wells Fargo? Explain the reasons for your answers. 5) Does Wells Fargo's auditor appear to have complied with the PCAOB's standards for obtaining sufficient appropriate audit evidence (AS 1105.08 and AS 1105.29)? Provide your reasoning. 6) Read the auditor's opinion on Wells Fargo's December 31. 2015 nancial statements [Wells Fargo & Company. 2015). What opinion was given (unqualied, qualied, adverse or disclaimer]? Do you believe this was the right opinion to give? if not, what opinion should have been given? Explain the reasons for your answers. 7) \"Given the severity of the fraudulent account activity and KPMG's prior knowledge of the incident, we believe shareholders may question whether KPMG is adequately ensuring the integrity and transparency of financial information". said advisory firm Glass Lewis. recommending a vote against rcappointing KPMG, the auditor since 1931 (Roberts, 2013). in the European Union (EU), every 10years a public company must engage a new Certified Public Accountant firm (CPA firm). to enhance auditor independence. The PCAOB has no such rule. Should the PCAOB have such a rule? Provide your reasoning. S) The Wells Fargo audited financial statements for the year ended December 31,2015. were not used in a securities offering. Could KPMG be sued under the Securities Act of 1933'? Explain the reasons for your answer. You can nd information in auditing texts. 9) Could KPMG be sued under the Securities Exchange Act of 1934? Explain the reasons for your answer. You can find information in auditing texts. 1 Imps /lwww.govtlii'o gpv/contznl/pkyCOMPS-ISSA/pdf/COMPS-l884md7 mt TUS 4. TEACHING STRATEGY AND CASE IMPLEMENTATION GUIDANCE 4.1. Case introduction Wells Fargo's senior executives orchestrated a massive consumer fraud. They did not disclose it, which caused a financial reporting fraud. This is current (some of the proceedings are pending as of 2021). which means students find it to be more relevant. Our case study consists of three parts. First. there is the case itself which provides students background information and questions to answer. Second. there is the teaching strategy and case implementation guidance which will assist the instructor in achieving the learning objectives. Third, the authors have developed answers to the case questions. These answers will not be published but will be provided to instructors upon request. 4.2. Learning objectives Critical thinking and professional skepticism are essential for auditors to provide high-quality auditing. Auditing is a rather complicated process, requiring the application of concepts, auditing standards, and laws to fact patterns, Upon successful completion of this case study, snidents should be able to achieve the following learning objectives: Ql: Define and identify consumer fraud. Q2: Analyze potential liabilities under the three- part classification required by the Generally Accepted Accounting Principles (GAAP) to identify contingent liabilities. Q3: Define and analyze materiality, considering all the stakeholders of a public company. Q4: Apply the duty of a public company auditor under section 10A of the Securities Exchange Act of 1934 to disclose illegal acts. (25. Know how to apply the duty of a pubhc company auditor to obtain sufficient appropriate audit evidence. Q6: Determine the appropriate audit opinion. This question leverages off of the sequential learning from the previous questions. Q7: Understand auditor independence and the mandatory rotation of the CPA firm controversy. Q8: Apply the liability under the Securities Act of 1933 to Wells Fargo's auditor. Q9: Apply the liability under the Securities Exchange Act of 1934 to the auditor. The questions (learning objectives) above are shown in the order of their suggested use. 4.3. Intended audience This case was implemented in three auditing classes in Fall 2020. Two sections were at the undergraduate level, with juniors and seniors majoring in accounting. One was at the graduate level, with most students in the Masters of Science in accounting program. These classes were at a mediumVsized university in Boston. The classes are normally facer toface but were taught remotely due to the coronavirus pandemic. I to ma rkzss 4.4. Implementation suggestions This case is compatible with any auditing textbook. both at the undergraduate and graduate levels. Students worked on the case in teams (assigned by the instructor) of three outside of the regular class time. Students usually had a week to work on the questions. At the beginning of the semester. students answered Q1 (this question would also be appropriate for a fraud examination class). Later. they answered (22. Q3. Q4 and Q5. Near the end of the semester. students answered Q6. Q7. Q8 and Q9. Only the materials essential for the case requirements are hyperlinked into the case document. If an instructor wants to provide any additional materials to students, they are linked in the References. The case was linked to the online syllabus and course schedule. Little class time was required to explain the case because its requirements are clear. However, for some undergraduate classes, it may be useful to go over parts of the May 4. 2015 LA City Attorney complaint (The Office of the City Attorney, 2015), and the Wells Fargo financials for the year ended December 31. 2015 (Wells Fargo 8r Company. 2015). to increase students' understanding of how the material in those documents relates to the case and the questions. Students emailed their team's answers in a Word document. Comments were inserted into each group's submitted Word document evaluating the submission and explaining the team's evaluation. By the end of the semester. each student had a better understanding of consumer fraud. financial reporting fraud, materiality, audit evidence. audit opinions auditor liability under the federal securities statutes, independence. mandatory rotation of the CPA firm, contingent liabilities. and illegal acts. These last three topics are important. but often omitted from auditing texts. What is also omitted from auditing texts is the discussion of stakeholders beyond the obvious stockholders. bondholders and creditors. and the need for the expanded group of stakeholders of a public corporation to receive materially correct financial reporting. All these topics are interrelated in the Wells Fargo case, as they are in actual audit practice. which makes this case an effective and relevant learning experience. Each student in a group received the same grade. Instructors could also include peer evaluation as part of the group Work if applicable. The rigor of the grading varied. For example, more is expected of graduate students than of undergraduate students. To reinforce the learning. the Wells Fargo case was referred to throughout the semester in class lectures. In the semester tests. questions were asked about the case. Students' opinion survey was conducted. The results are shown in Table 2. Table 2. Student survcy result Mean Item uo Compictin the Wells Fargo casc hclpcd me understand consumer fraud ((11). 4.50 Completing the Wells Fargo case helped me understand contingent liabilities iQZ. 4.26 Completing the Wells Fargo case helped me understand matsnaliry ((13). 4.13 Complain thc Wells Fargo casc- hclpcd mc undcrstaud thc auditor's duty to disclosc rilcgai acts (Q4). 4.59 Completing the Wells Fargo case helped me understand audit evidence rosy. 4.35 completing the Wells Fargo case helped me understand the process for the auditor to decide on 4 26 the agpropnare audit opinion (on). . Complcting the Wells Fargo casc helped me understand auditor rndcpcndoncc and thc mandatory 4 .5 4 .4 rotation of the CPA firm controversy (Q7). ' ' ' Completing the Wells Fargo case helped me understand auditor liabilit under Ihe Securities Act of 1933 too. am 4.14 Completing the Wells Fargo case helped me understand auditor liability under the Secunnes rxchange 4 26 4 07 Act of 1934 1119). . ~ I recommend that this case be part of the auditin course in the future. 4.47 4.64 The level of difficulty of the Wells Fargo case is apnmpnare for me auditing course. 4.33 4.71 collaborating With other students to complete this case was beneficial. 4.53 4.29 Overall. the Wells Fargo case was a useful method for learning, 4.59 417] Notes: 5 : strongly agree; 4 : agree neutral; 2 : disagree; 5. CONCLUSION Both graduate and undergraduate auditing students were enthusiastic in learning the facts described in the case and the outside linked documents. Since tins is an actual. recent case. concerning a Big 4 CPA firm. students were able to apply and gain an understanding of the interrelationship of important contemporary issues that are often underemphasized or even omitted from auditing textbooks. The participating students enhanced their ; VIR TUS} : strongly disagree. critical thinking by developing detailed answers for questions on topics that require substantial professional judgment for practicing auditors. Students worked in teams and thus developed their collaborative and interpersonal skills. A limitation of this case is that we have survey data for only one semester. We would have drawn firmer conclusions about its pedagogical efficacy. However. we hope to conduct more surveys in future semesters once the coronavirus pandemic is over

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance