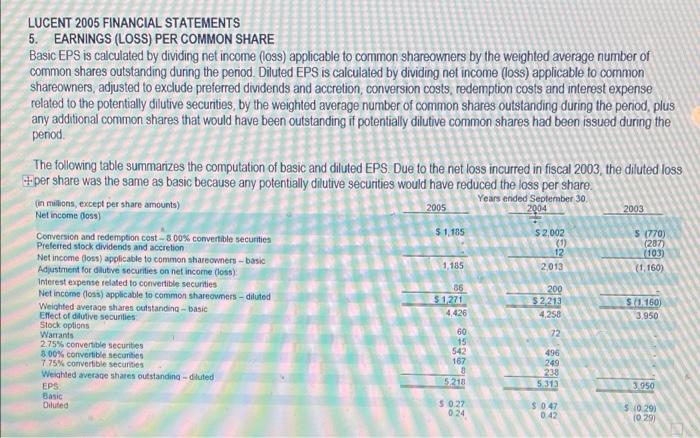

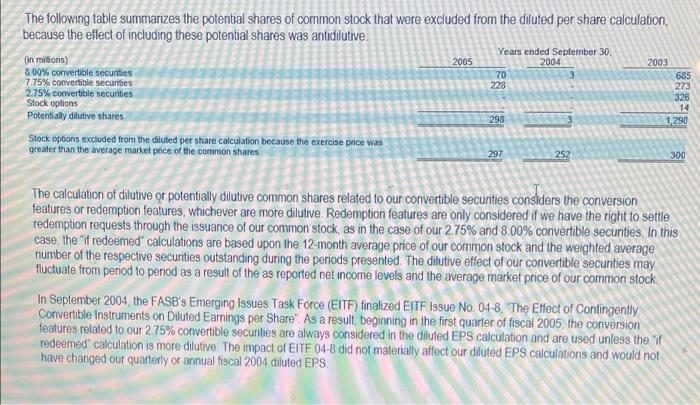

REQUIRED 1. For 2005, what adjustments were made to the numerator and denominator of the basic EPS equation in the company's calculation of diluted EPS? PARA MAKAN Ons het hon valinn to the usar 0092 LUCENT 2005 FINANCIAL STATEMENTS 5. EARNINGS (LOSS) PER COMMON SHARE Basic EPS is calculated by dividing net income (1038) applicable to common shareowners by the weighted average number of common shares outstanding during the penod. Diluted EPS is calculated by dividing net income (loss) applicable to common shareowners, adjusted to exclude preferred dividends and accretion, conversion costs, redemption costs and interest expense related to the potentially dilutive securities, by the weighted average number of common shares outstanding during the period, plus any additional common shares that would have been outstanding it potentially dilutive common shares had been issued during the period The following table summarizes the computation of basic and diluted EPS. Due to the net loss incurred in fiscal 2003, the diluted loss per share was the same as basic because any potentially dilutive securities would have reduced the loss per share. (in milions, except per share amounts) Years ended September 30 2005 2004 2003 Net income foss) Conversion and redemption cost -300% convertible securities $ 1.185 $ 2,002 S (770) (0) (287) Preferred stock dividends and accretion 12 (103) Net income doss) applicable to common shareowners-basic 1,185 2013 Adjustment for dutive securities on net income (oss) (1.160) Interest expense related to convertible securities 200 Net income (loss) applicable to common shareowners - diluted $2213 Weighted average shares outstanding - basic S10.160 Effect of dilutive secunties 4,258 3.950 Stock options Warrants 72 275% convertible securities 8.00% convertible securities 7.75% convertible Securities Weighted average shares outstanding-diluted 5218 EPS 3.950 Basic Diluted $ 0.29) 10.29) 56 $ 1,271 4426 60 15 542 167 9 496 249 238 5.31 5 0.27 0.24 $ 0.47 0.42 The following table summarizes the potential shares of common stock that were excluded from the diluted per share calculation, because the effect of including these potential shares was antidilutive Years ended September 30 (in Millions) 2005 2004 800% convertible securities 70 3 7.75% convertible securities 228 2.75% convertible securities Stock options Potentially dilutive shares 298 Stock options excluded from the diluted per share calculation because the exercise price was greater than the average market price of the common shares 297 252 300 2003 685 273 326 14 1,299 The calculation of dilutive or potentially dilutive common shares related to our convertible securities considers the conversion features or redemption features, whichever are more dilutive. Redemption features are only considered if we have the right to settle redemption requests through the issuance of our common stock, as in the case of our 2.75% and 8.00% convertible securities. In this case, the "if redeemed calculations are based upon the 12 month average price of our common stock and the weighted average number of the respective securities outstanding during the periods presented. The dilutive effect of our convertible securities may fluctuate from period to period as a result of the as reported net income levels and the average market price of our common stock In September 2004, the FASB's Emerging issues Task Force (EITF) finalized EITF Issue No. 04-8. The Effect of Contingently Convertible Instruments on Diluted Earnings per Share" As a result, beginning in the first quarter of fiscal 2005, the conversion features related to our 2 75% convertible securities are always considered in the diluted EPS calculation and are used unless the 'i redeemed calculation is more dilutive. The impact of EITF 04-8 did not materially affect our diluted EPS calculations and would not have changed our quarterly or annual fiscal 2004 diluted EPS REQUIRED 1. For 2005, what adjustments were made to the numerator and denominator of the basic EPS equation in the company's calculation of diluted EPS? PARA MAKAN Ons het hon valinn to the usar 0092 LUCENT 2005 FINANCIAL STATEMENTS 5. EARNINGS (LOSS) PER COMMON SHARE Basic EPS is calculated by dividing net income (1038) applicable to common shareowners by the weighted average number of common shares outstanding during the penod. Diluted EPS is calculated by dividing net income (loss) applicable to common shareowners, adjusted to exclude preferred dividends and accretion, conversion costs, redemption costs and interest expense related to the potentially dilutive securities, by the weighted average number of common shares outstanding during the period, plus any additional common shares that would have been outstanding it potentially dilutive common shares had been issued during the period The following table summarizes the computation of basic and diluted EPS. Due to the net loss incurred in fiscal 2003, the diluted loss per share was the same as basic because any potentially dilutive securities would have reduced the loss per share. (in milions, except per share amounts) Years ended September 30 2005 2004 2003 Net income foss) Conversion and redemption cost -300% convertible securities $ 1.185 $ 2,002 S (770) (0) (287) Preferred stock dividends and accretion 12 (103) Net income doss) applicable to common shareowners-basic 1,185 2013 Adjustment for dutive securities on net income (oss) (1.160) Interest expense related to convertible securities 200 Net income (loss) applicable to common shareowners - diluted $2213 Weighted average shares outstanding - basic S10.160 Effect of dilutive secunties 4,258 3.950 Stock options Warrants 72 275% convertible securities 8.00% convertible securities 7.75% convertible Securities Weighted average shares outstanding-diluted 5218 EPS 3.950 Basic Diluted $ 0.29) 10.29) 56 $ 1,271 4426 60 15 542 167 9 496 249 238 5.31 5 0.27 0.24 $ 0.47 0.42 The following table summarizes the potential shares of common stock that were excluded from the diluted per share calculation, because the effect of including these potential shares was antidilutive Years ended September 30 (in Millions) 2005 2004 800% convertible securities 70 3 7.75% convertible securities 228 2.75% convertible securities Stock options Potentially dilutive shares 298 Stock options excluded from the diluted per share calculation because the exercise price was greater than the average market price of the common shares 297 252 300 2003 685 273 326 14 1,299 The calculation of dilutive or potentially dilutive common shares related to our convertible securities considers the conversion features or redemption features, whichever are more dilutive. Redemption features are only considered if we have the right to settle redemption requests through the issuance of our common stock, as in the case of our 2.75% and 8.00% convertible securities. In this case, the "if redeemed calculations are based upon the 12 month average price of our common stock and the weighted average number of the respective securities outstanding during the periods presented. The dilutive effect of our convertible securities may fluctuate from period to period as a result of the as reported net income levels and the average market price of our common stock In September 2004, the FASB's Emerging issues Task Force (EITF) finalized EITF Issue No. 04-8. The Effect of Contingently Convertible Instruments on Diluted Earnings per Share" As a result, beginning in the first quarter of fiscal 2005, the conversion features related to our 2 75% convertible securities are always considered in the diluted EPS calculation and are used unless the 'i redeemed calculation is more dilutive. The impact of EITF 04-8 did not materially affect our diluted EPS calculations and would not have changed our quarterly or annual fiscal 2004 diluted EPS