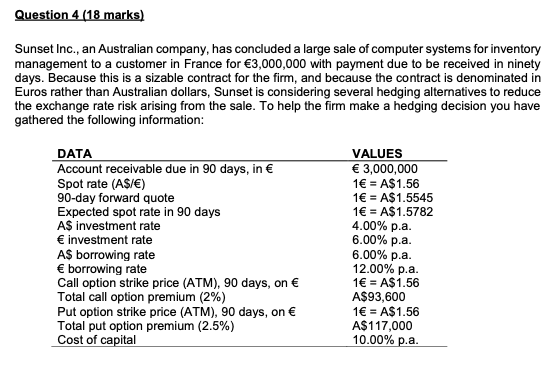

Question

Required: a) Does the market prediction (i.e. expectation) imply an appreciation or depreciation in the Australian dollar in relation to the Euro? Please explain why.

Required:

a) Does the market prediction (i.e. expectation) imply an appreciation or depreciation in the Australian dollar in relation to the Euro? Please explain why.

(2 marks)

b) What would be the outcome if Sunset does not hedge this transaction and the predicted (i.e. expected) exchange rate for 3 months proves to be correct?

(2 marks)

c) If Sunset hedges the transaction in the forward market, what should it do? What would be the proceeds of the transaction in 90 days time?

(3 marks)

-

d) If Sunset locks in a forward hedge and the actual spot rate in 90 days time turns out to be the expected spot rate, would this result in a foreign exchange gain or loss? What will be the amount of the gain or loss?

(3 marks)

-

e) If Sunset chooses to hedge its transaction exposure in the option market, what action will it take?

(2 marks)

-

f) If Sunset decides to hedge its position using the option suggested in part e), and the actual spot rate in 90 days time turns out to be the expected spot rate, should Sunset exercise the option? What will be the amount of the gross profit and net profit?

(3 marks)

-

g) If Sunset decides to hedge its position using the option suggested in part e), and the actual spot rate in 90 days time turns out to be A$1.53/, should Sunset exercise the option? What will be the amount of the gross profit and net profit?(3 marks)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Complacency And Collusion A Critical Introduction To Business And Financial Journalism

Authors: Keith J. Butterick

1st Edition

074533203X,1849648379