Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Required: Compute the payback period for the two alternatives. Assuming the company requires an 8% return from capital investments determine the net present value of

Required:

- Compute the payback period for the two alternatives.

- Assuming the company requires an 8% return from capital investments determine the net present value of the two alternatives. Based on the results of the calculated net present value, which investment would you recommend that Mike and Tim pursue?

- Perform net present value calculations using the original cash flows but modifying the companys required return from capital investment decisions. First, assume the required rate of return is 6%. Next, assume the required rate of return is 10%. How would these modifications affect the recommendation that you would make to Mike and Tim?

- Assuming the company has a hurdle rate for capital investments of 8% determine the internal rate of return for the two alternatives. Discuss the advantages and disadvantages of using the internal rate of return method to evaluate capital investment decisions. Based on the results of the calculated internal rate of return, which investment would you recommend that Mike and Tim pursue?

- During a discussion with Mike, he indicated that he believes the cash flow estimates for the new system are very conservative. He feels that the net cash flows will be 10% larger than the numbers provided in years 2 through 6. How will those changes affect the payback period, NPV, and IRR?

- Discuss any significant assumptions that are required when using each of the capital investment tools. Are there any concerns that you would want to bring to Mike and Tims attention related to these assumptions?

- What is your final recommendation?

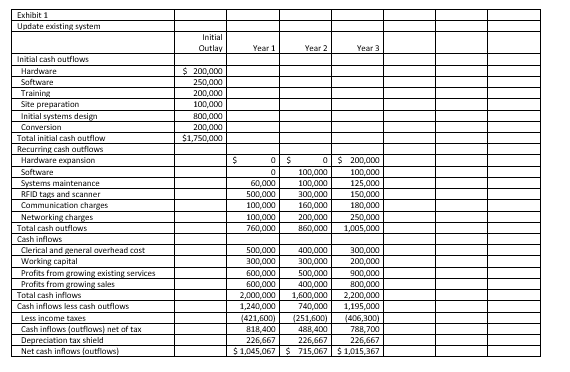

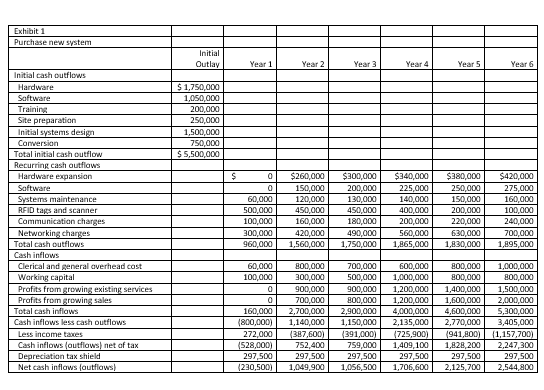

xhibit 1 ear 1 Year 2 Year 3 nitial cash outflows $1,750,000 Recurring cash autflaws RFID tags and scanner Communication charges 200,0002 250,000 Clerical and general averhead cast Profits from growing existing services 2,000,000 1,600,0002,200,000 Cash inflows less tash outflows Cash inflows (autflaws) net af tax Depreciation tax shield Net cash inflaws fautflaws Purchase new system Outlay tial cash outflows Hardware 1,050,000 200,000 250,000 1,500,000 750,000 $ 5,500,000 Recurring cash autflaws Hardware expansian RFID tags and scanner Communication charges Networking ch 250,000 150,000 200,000 220,000 630,000 960,000 1,560,000 1,750,000 1,865,000 1830,000 60,000 500,000 100,000 300,000 150,000 120,000 450,000 160,000 420,000 200,000 130,000 450,000 180,000 490,000 225,000 140,000 400,000 200,000 560,000 275,000 160,000 100,000 240,000 700,000 1,895,000 Clerical and general averhead cast 60,000 100,000 800,000 300,000 900,000 700,000 700,000 500,000 1,000,000 600,000 800,000 800,000 1,000,000 800,000 arking capital Profits from growing existing services Profits from growing sales Total cash inflaws Cash inflows less cash outflows 160,0002,700,000 2,900,00O 4,0O0,000 4,600,000 5,300,000 800,000 272,000 528,000) 297,500 1,140,00 1,150,0002,135,0002770,000 3,405,000 759,0001,409,100 1,828,200 2,247,300 2,125,700 2,544,800 87,600) 752,400 297,500 391,000) 725,900) 941,800 Cash inflows (autflaws) net af tax Depreciation tax shield Net cash inflaws fautflaws 297,500 1,049,900 1,0S6,5001,706,600 230,500) xhibit 1 ear 1 Year 2 Year 3 nitial cash outflows $1,750,000 Recurring cash autflaws RFID tags and scanner Communication charges 200,0002 250,000 Clerical and general averhead cast Profits from growing existing services 2,000,000 1,600,0002,200,000 Cash inflows less tash outflows Cash inflows (autflaws) net af tax Depreciation tax shield Net cash inflaws fautflaws Purchase new system Outlay tial cash outflows Hardware 1,050,000 200,000 250,000 1,500,000 750,000 $ 5,500,000 Recurring cash autflaws Hardware expansian RFID tags and scanner Communication charges Networking ch 250,000 150,000 200,000 220,000 630,000 960,000 1,560,000 1,750,000 1,865,000 1830,000 60,000 500,000 100,000 300,000 150,000 120,000 450,000 160,000 420,000 200,000 130,000 450,000 180,000 490,000 225,000 140,000 400,000 200,000 560,000 275,000 160,000 100,000 240,000 700,000 1,895,000 Clerical and general averhead cast 60,000 100,000 800,000 300,000 900,000 700,000 700,000 500,000 1,000,000 600,000 800,000 800,000 1,000,000 800,000 arking capital Profits from growing existing services Profits from growing sales Total cash inflaws Cash inflows less cash outflows 160,0002,700,000 2,900,00O 4,0O0,000 4,600,000 5,300,000 800,000 272,000 528,000) 297,500 1,140,00 1,150,0002,135,0002770,000 3,405,000 759,0001,409,100 1,828,200 2,247,300 2,125,700 2,544,800 87,600) 752,400 297,500 391,000) 725,900) 941,800 Cash inflows (autflaws) net af tax Depreciation tax shield Net cash inflaws fautflaws 297,500 1,049,900 1,0S6,5001,706,600 230,500)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started