Answered step by step

Verified Expert Solution

Question

1 Approved Answer

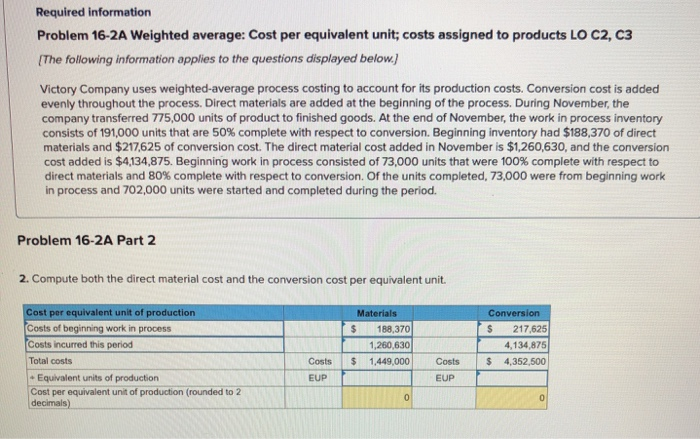

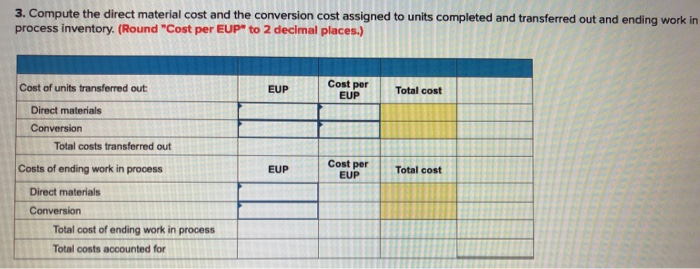

Required information Problem 16-2A Weighted average: Cost per equivalent unit; costs assigned to products LO C2, C3 The following information applies to the questions displayed

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Value Added Auditing CERM Academy Series On Enterprise Risk Management

Authors: Greg Hutchins

4th Edition

978-0965466554