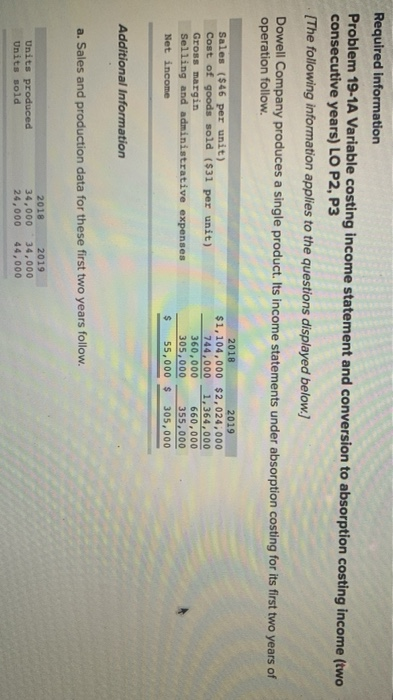

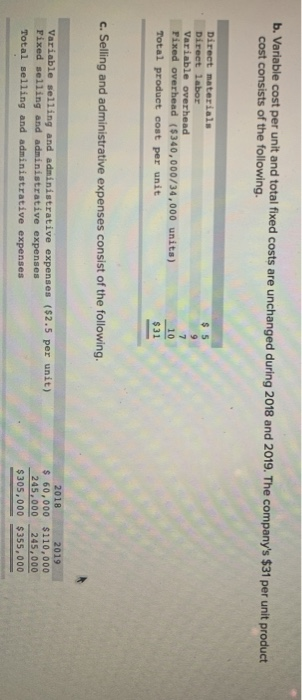

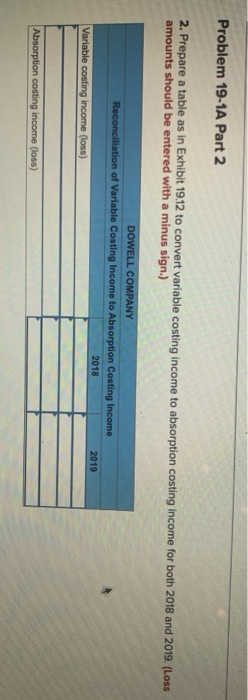

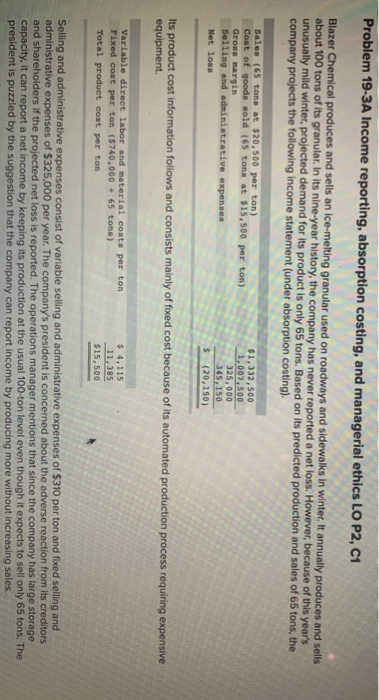

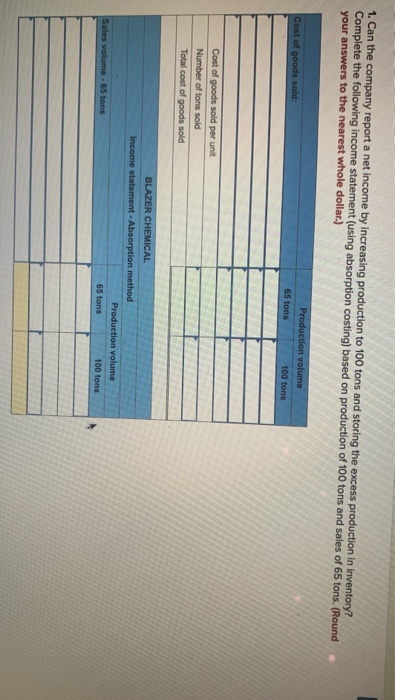

Required information Problem 19-1A Variable costing income statement and conversion to absorption costing income (two consecutive years) LO P2, P3 [The following information applies to the questions displayed below.) Dowell Company produces a single product. Its income statements under absorption costing for its first two years of operation follow Sales ($46 per unit) Cost of goods sold ($31 per unit) Gross margin Selling and administrative expenses Net income 2018 $1,104,000 $2,024,000 744,000 1,364,000 360,000 660,000 305,000 355,000 55,000 $ 305,000 Additional Information a. Sales and production data for these first two years follow. Units produced Units sold 2018 34,000 24,000 2019 34,000 44,000 b. Variable cost per unit and total fixed costs are unchanged during 2018 and 2019. The company's $31 per unit product cost consists of the following. $ 5 Direet materials Direct labor Variable overhead Fixed overhead ($340,000/34,000 units) Total product cost per unit 10 $31 c. Selling and administrative expenses consist of the following. Variable selling and administrative expenses ($2.5 per unit) Fixed selling and administrative expenses Total selling and administrative expenses 2018 2019 $ 60,000 $110,000 245,000 245,000 $305,000 $355,000 Problem 19-1A Part 2 2. Prepare a table as in Exhibit 19.12 to convert variable costing income to absorption costing income for both 2018 and 2019. (Loss amounts should be entered with a minus sign.) DOWELL COMPANY Reconciliation of Variable Costing Income to Absorption Costing Income 2018 Variable costing income (loss) 2019 Absorption costing income (loss) Problem 19-3A Income reporting, absorption costing, and managerial ethics LO P2, C1 Blazer Chemical produces and sells an ice-melting granular used on roadways and sidewalks in winter. It annually produces and sells about 100 tons of its granular. In its nine-year history, the company has never reported a net loss. However, because of this year's unusually mild winter, projected demand for its product is only 65 tons. Based on its predicted production and sales of 65 tons, the company projects the following income statement (under absorption costing). Sales (65 tons at $20,500 per ton) Cost of goods sold (65 tons at $15,500 per ton) Gross margin Selling and administrative expenses Net loss $1,332,500 1.007,500 325,000 345,150 $ (20,150) Its product cost information follows and consists mainly of fixed cost because of its automated production process requiring expensive equipment Variable direct labor and material costs per ton Fixed cost per ton (5740,000 - 65 tons) Total product cost per ton $ 4,115 11,385 $15,500 Selling and administrative expenses consist of variable selling and administrative expenses of $310 per ton and fixed selling and administrative expenses of $325,000 per year. The company's president is concerned about the adverse reaction from its creditors and shareholders if the projected net loss is reported. The operations manager mentions that since the company has large storage capacity, it can report a net income by keeping its production at the usual 100-ton level even though it expects to sell only 65 tons. The president is puzzled by the suggestion that the company can report income by producing more without increasing sales. 1. Can the company report a net income by increasing production to 100 tons and storing the excess production in inventory? Complete the following income statement (using absorption costing) based on production of 100 tons and sales of 65 tons. (Round your answers to the nearest whole dollar.) Cost of goods sold: Production volume 65 tons 100 tons Cost of goods sold per unit Number of tons sold Total cost of goods sold BLAZER CHEMICAL Income statement-Absorption method Production volume 65 tons 100 tons Sales volume - 65 tons Required information Problem 19-1A Variable costing income statement and conversion to absorption costing income (two consecutive years) LO P2, P3 [The following information applies to the questions displayed below.) Dowell Company produces a single product. Its income statements under absorption costing for its first two years of operation follow Sales ($46 per unit) Cost of goods sold ($31 per unit) Gross margin Selling and administrative expenses Net income 2018 $1,104,000 $2,024,000 744,000 1,364,000 360,000 660,000 305,000 355,000 55,000 $ 305,000 Additional Information a. Sales and production data for these first two years follow. Units produced Units sold 2018 34,000 24,000 2019 34,000 44,000 b. Variable cost per unit and total fixed costs are unchanged during 2018 and 2019. The company's $31 per unit product cost consists of the following. $ 5 Direet materials Direct labor Variable overhead Fixed overhead ($340,000/34,000 units) Total product cost per unit 10 $31 c. Selling and administrative expenses consist of the following. Variable selling and administrative expenses ($2.5 per unit) Fixed selling and administrative expenses Total selling and administrative expenses 2018 2019 $ 60,000 $110,000 245,000 245,000 $305,000 $355,000 Problem 19-1A Part 2 2. Prepare a table as in Exhibit 19.12 to convert variable costing income to absorption costing income for both 2018 and 2019. (Loss amounts should be entered with a minus sign.) DOWELL COMPANY Reconciliation of Variable Costing Income to Absorption Costing Income 2018 Variable costing income (loss) 2019 Absorption costing income (loss) Problem 19-3A Income reporting, absorption costing, and managerial ethics LO P2, C1 Blazer Chemical produces and sells an ice-melting granular used on roadways and sidewalks in winter. It annually produces and sells about 100 tons of its granular. In its nine-year history, the company has never reported a net loss. However, because of this year's unusually mild winter, projected demand for its product is only 65 tons. Based on its predicted production and sales of 65 tons, the company projects the following income statement (under absorption costing). Sales (65 tons at $20,500 per ton) Cost of goods sold (65 tons at $15,500 per ton) Gross margin Selling and administrative expenses Net loss $1,332,500 1.007,500 325,000 345,150 $ (20,150) Its product cost information follows and consists mainly of fixed cost because of its automated production process requiring expensive equipment Variable direct labor and material costs per ton Fixed cost per ton (5740,000 - 65 tons) Total product cost per ton $ 4,115 11,385 $15,500 Selling and administrative expenses consist of variable selling and administrative expenses of $310 per ton and fixed selling and administrative expenses of $325,000 per year. The company's president is concerned about the adverse reaction from its creditors and shareholders if the projected net loss is reported. The operations manager mentions that since the company has large storage capacity, it can report a net income by keeping its production at the usual 100-ton level even though it expects to sell only 65 tons. The president is puzzled by the suggestion that the company can report income by producing more without increasing sales. 1. Can the company report a net income by increasing production to 100 tons and storing the excess production in inventory? Complete the following income statement (using absorption costing) based on production of 100 tons and sales of 65 tons. (Round your answers to the nearest whole dollar.) Cost of goods sold: Production volume 65 tons 100 tons Cost of goods sold per unit Number of tons sold Total cost of goods sold BLAZER CHEMICAL Income statement-Absorption method Production volume 65 tons 100 tons Sales volume - 65 tons