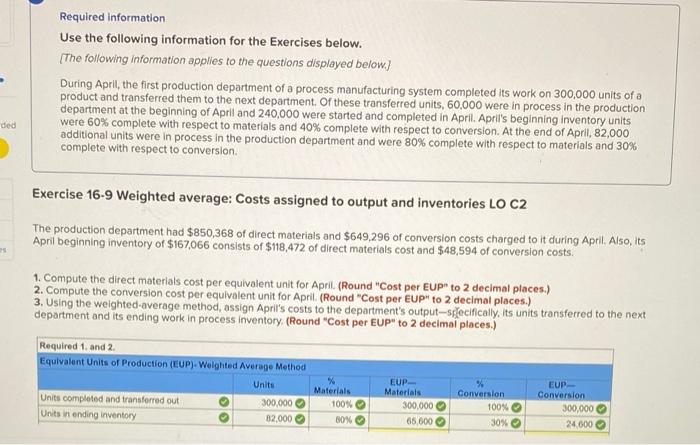

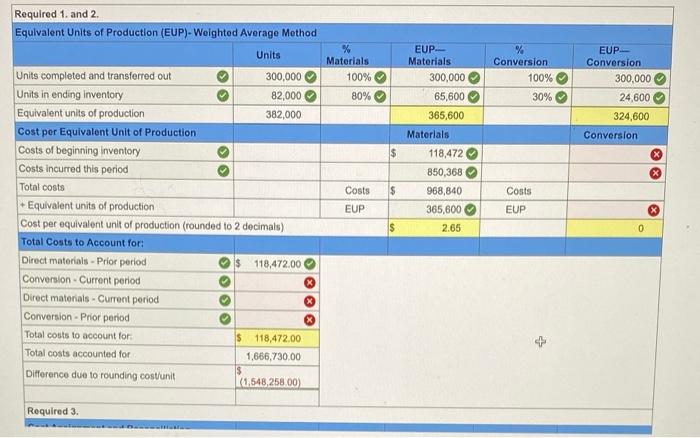

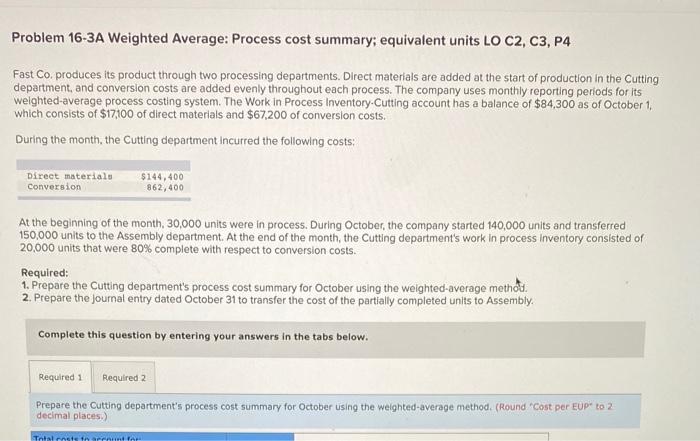

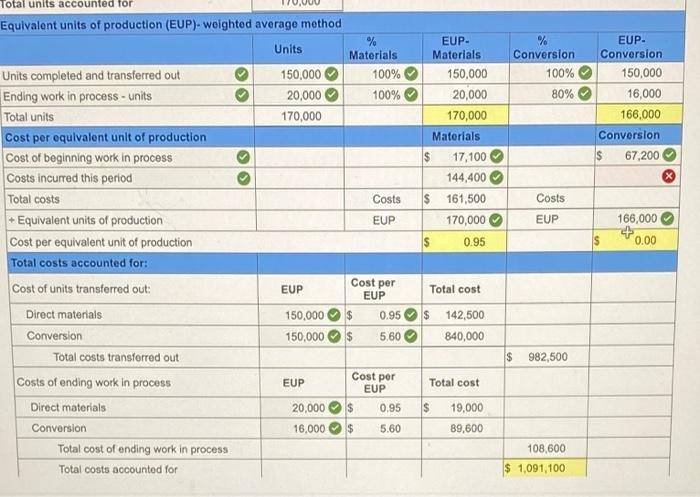

Required information Use the following information for the Exercises below. (The following information applies to the questions displayed below.) During April, the first production department of a process manufacturing system completed its work on 300,000 units of a product and transferred them to the next department of these transferred units, 60,000 were in process in the production department at the beginning of April and 240,000 were started and completed in April . April's beginning inventory units were 60% complete with respect to materials and 40% complete with respect to conversion. At the end of April, 82,000 additional units were in process in the production department and were 80% complete with respect to materials and 30% complete with respect to conversion ded Exercise 16-9 Weighted average: Costs assigned to output and inventories LO C2 The production department had $850,368 of direct materials and $649,296 of conversion costs charged to it during April. Also, its April beginning inventory of $167,066 consists of $118,472 of direct materials cost and $48,594 of conversion costs. 1. Compute the direct materials cost per equivalent unit for April (Round "Cost per Eup to 2 decimal places.) 2. Compute the conversion cost per equivalent unit for April (Round "Cost per EUP" to 2 decimal places.) 3. Using the weighted average method, assign April's costs to the department's output-specifically, its units transferred to the next department and its ending work in process inventory (Round "Cost per EUP" to 2 decimal places.) Required 1 and 2 Equivalent Units of Production (IUP). Weighted Average Method Units Units completed and transferred out Unitsin ending inventory % Materials 100% 80% 300,000 82.000 EUP Materials 300,000 65,600 Conversion 100% EUP Conversion 300,000 24.000 30% % Materials 100% 80% Conversion 100% 30% EUP Conversion 300,000 24,600 324,600 EUP Materials 300,000 65,600 365,600 Materials 118,472 850,368 968,840 365,600 2.65 Conversion $ X Required 1 and 2 Equivalent Units of Production (EUP)-Weighted Average Mothod Units Units completed and transferred out 300,000 Unitsin ending inventory 82,000 Equivalent units of production 382,000 Cost per Equivalent Unit of Production Costs of beginning inventory Costs incurred this period Total costs Equivalent units of production Cost per equivalent unit of production (rounded to 2 decimals) Total Costs to Account for: Direct materials - Prior period $ 118,472.00 Conversion Current period Direct materials. Current period Conversion - Prior period Total costs to account for $ 118,472.00 Total costs accounted for 1,686,730.00 is Difference due to rounding costunit (0.548,258.00) $ Costs EUP Costs EUP & * 0 $ 0 Required 3. Problem 16-3A Weighted Average: Process cost summary; equivalent units LO C2, C3, P4 Fast Co. produces its product through two processing departments. Direct materials are added at the start of production in the Cutting department, and conversion costs are added evenly throughout each process. The company uses monthly reporting periods for its weighted average process costing system. The Work in Process Inventory-Cutting account has a balance of $84,300 as of October 1 which consists of $17,100 of direct materials and $67,200 of conversion costs. During the month, the Cutting department incurred the following costs Direct materiale Conversion $144,400 862,400 At the beginning of the month, 30,000 units were in process. During October, the company started 140,000 units and transferred 150,000 units to the Assembly department. At the end of the month, the Cutting department's work in process inventory consisted of 20.000 units that were 80% complete with respect to conversion costs. Required: 1. Prepare the Cutting department's process cost summary for October using the weighted average method 2. Prepare the journal entry dated October 31 to transfer the cost of the partially completed units to Assembly. Complete this question by entering your answers in the tabs below. Required 1 Required 2 Prepare the cutting department's process cost summary for October using the weighted average method. (Round 'Cost per EUP" to 2 decimal places.) Total Total units accounted for EUP- Conversion % Conversion 100% 80% 150,000 EUP- Materials 150,000 20,000 170,000 Materials $ 17,100 144,400 $ 161,500 170,000 16,000 166,000 Conversion S 67,200 Costs EUP 166,000 Equivalent units of production (EUP)-weighted average method % Units Materials Units completed and transferred out 150,000 100% Ending work in process - units 20,000 100% Total units 170,000 Cost per equivalent unit of production Cost of beginning work in process Costs incurred this period Total costs Costs + Equivalent units of production EUP Cost per equivalent unit of production Total costs accounted for: Cost of units transferred out: EUP EUP Direct materials 150,000 $ 0.95 Conversion 150,000 $ 5.60 Total costs transferred out Costs of ending work in process Cost per EUP EUP Direct materials 20,000 $ 0.95 Conversion 16,000 $ 5.60 Total cost of ending work in process Total costs accounted for 0.95 0.00 Cost per Total cost $ 142,500 840,000 $ 982,500 Total cost $ 19,000 89,600 108,600 $ 1,091,100