Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Required: The weights of X, Y, and Z in the MVE portfolio are? You wish to construct the minimum variance efficient (MVE) portfolio that consists

Required:

The weights of X, Y, and Z in the MVE portfolio are?

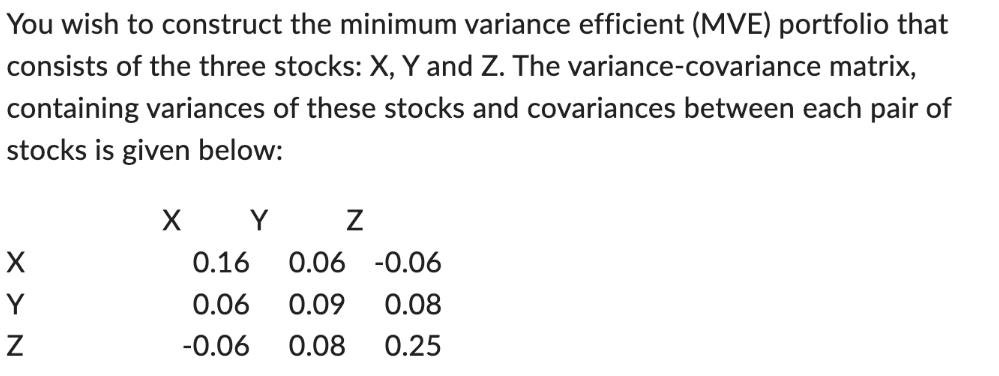

You wish to construct the minimum variance efficient (MVE) portfolio that consists of the three stocks: X, Y and Z. The variance-covariance matrix, containing variances of these stocks and covariances between each pair of stocks is given below: X > N Y X Y 0.16 0.06 -0.06 0.06 0.09 0.08 -0.06 0.08 0.25 Z

Step by Step Solution

★★★★★

3.37 Rating (147 Votes )

There are 3 Steps involved in it

Step: 1

To construct the Minimum Variance Efficient MVE portfolio we need to find the weights of stocks X Y and Z that minimize the portfolio variance while satisfying some constraints The MVE portfolio is ty...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Introduction to Algorithms

Authors: Thomas H. Cormen, Charles E. Leiserson, Ronald L. Rivest

3rd edition

978-0262033848