Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Research and critically discuss whether the fraud committeed by Brooks could have risked the collapse of DHB industries Inc in 2004 Justify your opinion,stating any

Research and critically discuss whether the fraud committeed by Brooks could have risked the collapse of DHB industries Inc in 2004 Justify your opinion,stating any assumptions

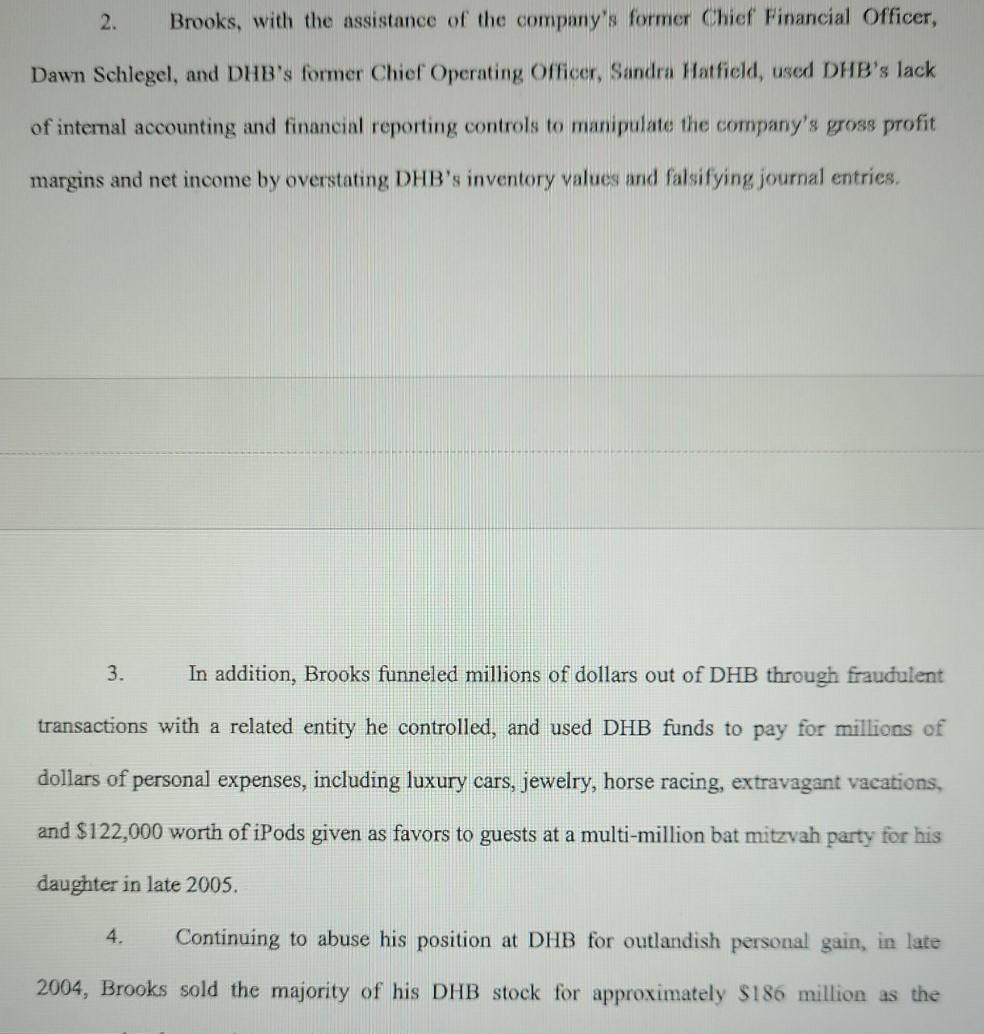

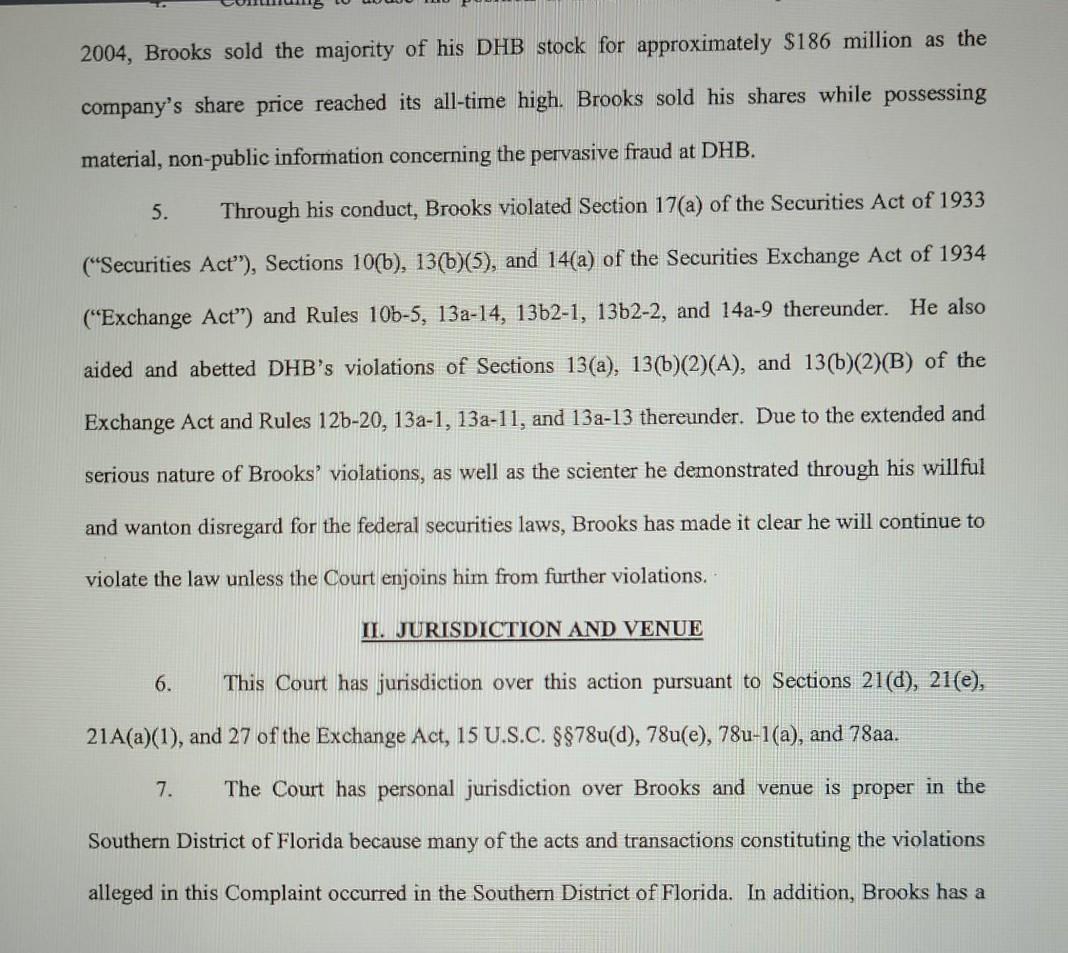

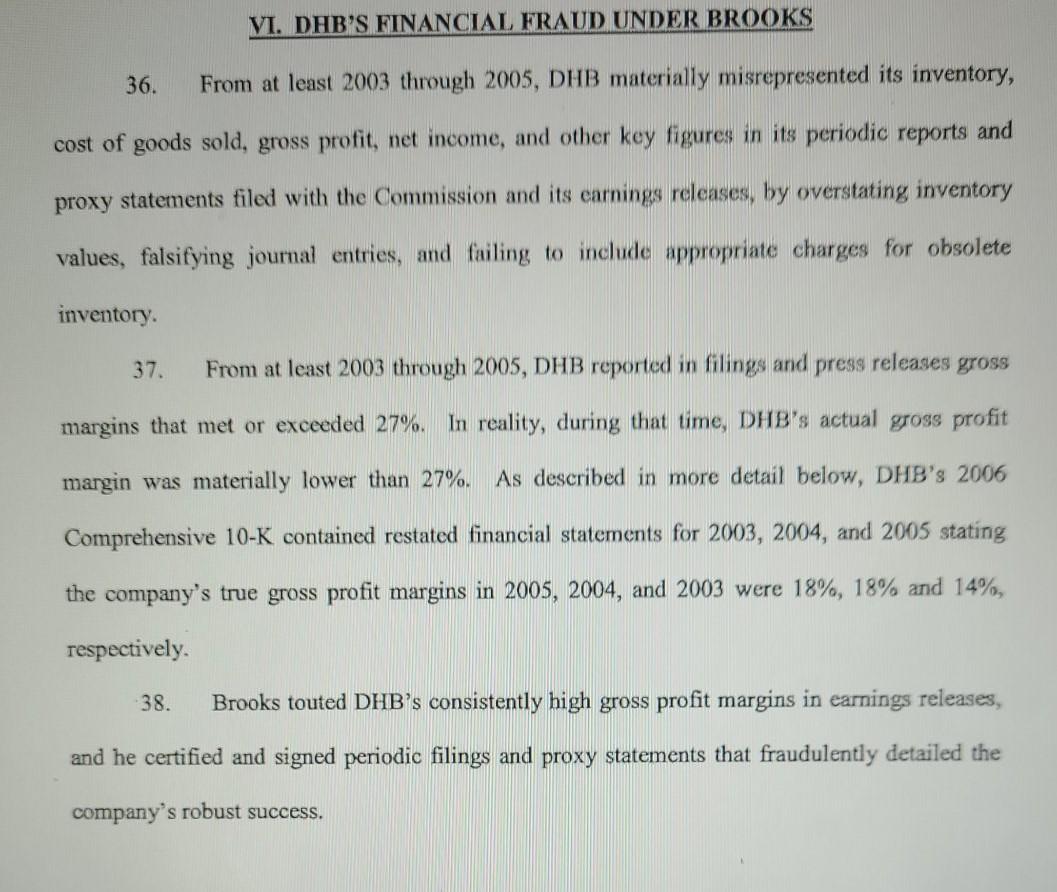

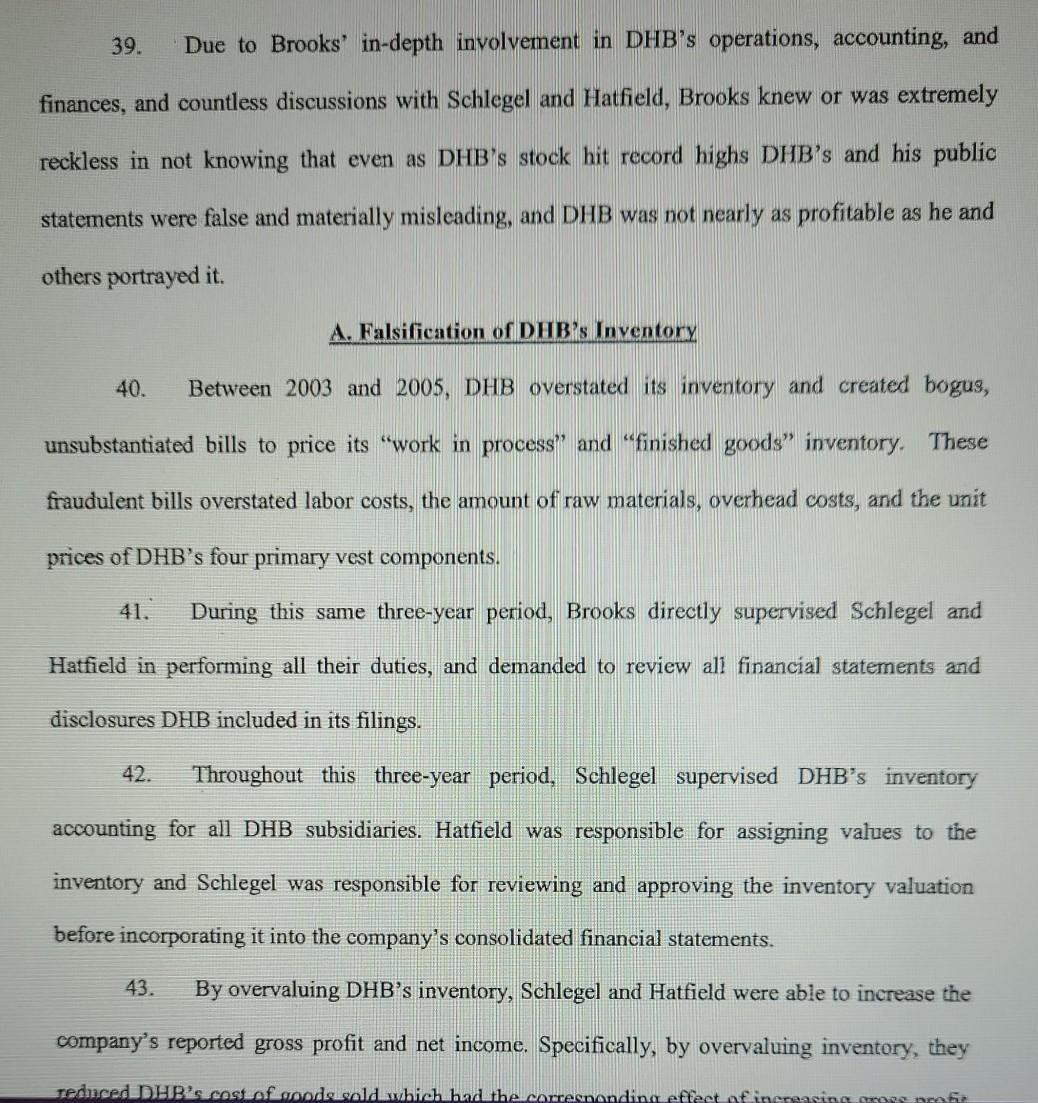

2. Brooks, with the assistance of the company's former Chief Financial Officer, Dawn Schlegel, and DHB's former Chief Operating Officer, Sandra Hatfield, used DHB's lack of internal accounting and financial reporting controls to manipulate the company's gross profit margins and net income by overstating DHB's inventory values and falsifying journal entries. 3. In addition, Brooks funneled millions of dollars out of DHB through fraudulent transactions with a related entity he controlled, and used DHB funds to pay for millions of dollars of personal expenses, including luxury cars, jewelry, horse racing, extravagant vacations, and $122,000 worth of iPods given as favors to guests at a multi-million bat mitzvah party for his daughter in late 2005. 4. Continuing to abuse his position at DHB for outlandish personal gain, in late 2004, Brooks sold the majority of his DHB stock for approximately $186 million as the 2004, Brooks sold the majority of his DHB stock for approximately $186 million as the company's share price reached its all-time high. Brooks sold his shares while possessing material, non-public information concerning the pervasive fraud at DHB. 5. Through his conduct, Brooks violated Section 17(a) of the Securities Act of 1933 (Securities Act"), Sections 10(b), 13(b)(5), and 14(a) of the Securities Exchange Act of 1934 (Exchange Act") and Rules 105-5, 132-14, 1362-1, 13b2-2, and 14a-9 thereunder. He also aided and abetted DHB's violations of Sections 13(a), 13(b)(2)(A), and 13(b)(2)(B) of the Exchange Act and Rules 12b-20, 13a-1, 13a-11, and 132-13 thereunder. Due to the extended and serious nature of Brooks' violations, as well as the scienter he demonstrated through his willful and wanton disregard for the federal securities laws, Brooks has made it clear he will continue to violate the law unless the Court enjoins him from further violations. II. JURISDICTION AND VENUE 6. This Court has jurisdiction over this action pursuant to Sections 21(d), 21(e), 21A(a)(1), and 27 of the Exchange Act, 15 U.S.C. 8878u(d), 78u(e), 78u-1(a), and 78aa. 7. The Court has personal jurisdiction over Brooks and venue is proper in the Southern District of Florida because many of the acts and transactions constituting the violations alleged in this Complaint occurred in the Southern District of Florida. In addition, Brooks has a VI. DAB'S FINANCIAL FRAUD UNDER BROOKS 36. From at least 2003 through 2005, DHB materially misrepresented its inventory, cost of goods sold, gross profit, net income, and other key figures in its periodic reports and proxy statements filed with the Commission and its earnings releases, by overstating inventory values, falsifying journal entries, and failing to include appropriate charges for obsolete inventory 37. From at least 2003 through 2005, DHB reported in filings and press releases gross margins that met or exceeded 27%. In reality, during that time, DHB's actual gross profit margin was materially lower than 27%. As described in more detail below, DHB's 2006 Comprehensive 10-K contained restated financial statements for 2003, 2004, and 2005 stating the company's true gross profit margins in 2005, 2004, and 2003 were 18%, 18% and 14%, respectively. 38. Brooks touted DHB's consistently high gross profit margins in earnings releases, and he certified and signed periodic filings and proxy statements that fraudulently detailed the company's robust success. 39. Due to Brooks' in-depth involvement in DHB's operations, accounting, and finances, and countless discussions with Schlegel and Hatfield, Brooks knew or was extremely reckless in not knowing that even as DHB's stock hit record highs DHB's and his public statements were false and materially misleading, and DHB was not nearly as profitable as he and others portrayed it. A. Falsification of DHBs Inventory 40. Between 2003 and 2005, DHB overstated its inventory and created bogus, unsubstantiated bills to price its "work in process and "finished goods inventory. These fraudulent bills overstated labor costs, the amount of raw materials, overhead costs, and the unit prices of DHB's four primary vest components. 41. During this same three-year period, Brooks directly supervised Schlegel and Hatfield in performing all their duties, and demanded to review all financial statements and disclosures DHB included in its filings. 42. Throughout this three-year period, Schlegel supervised DHB's inventory accounting for all DHB subsidiaries. Hatfield was responsible for assigning values to the inventory and Schlegel was responsible for reviewing and approving the inventory valuation before incorporating it into the company's consolidated financial statements. 43. By overvaluing DHB's inventory, Schlegel and Hatfield were able to increase the company's reported gross profit and net income. Specifically, by overvaluing inventory, they reduced DHBs.cost of produsold which had the corresponding effect of increasing cose non 2. Brooks, with the assistance of the company's former Chief Financial Officer, Dawn Schlegel, and DHB's former Chief Operating Officer, Sandra Hatfield, used DHB's lack of internal accounting and financial reporting controls to manipulate the company's gross profit margins and net income by overstating DHB's inventory values and falsifying journal entries. 3. In addition, Brooks funneled millions of dollars out of DHB through fraudulent transactions with a related entity he controlled, and used DHB funds to pay for millions of dollars of personal expenses, including luxury cars, jewelry, horse racing, extravagant vacations, and $122,000 worth of iPods given as favors to guests at a multi-million bat mitzvah party for his daughter in late 2005. 4. Continuing to abuse his position at DHB for outlandish personal gain, in late 2004, Brooks sold the majority of his DHB stock for approximately $186 million as the 2004, Brooks sold the majority of his DHB stock for approximately $186 million as the company's share price reached its all-time high. Brooks sold his shares while possessing material, non-public information concerning the pervasive fraud at DHB. 5. Through his conduct, Brooks violated Section 17(a) of the Securities Act of 1933 (Securities Act"), Sections 10(b), 13(b)(5), and 14(a) of the Securities Exchange Act of 1934 (Exchange Act") and Rules 105-5, 132-14, 1362-1, 13b2-2, and 14a-9 thereunder. He also aided and abetted DHB's violations of Sections 13(a), 13(b)(2)(A), and 13(b)(2)(B) of the Exchange Act and Rules 12b-20, 13a-1, 13a-11, and 132-13 thereunder. Due to the extended and serious nature of Brooks' violations, as well as the scienter he demonstrated through his willful and wanton disregard for the federal securities laws, Brooks has made it clear he will continue to violate the law unless the Court enjoins him from further violations. II. JURISDICTION AND VENUE 6. This Court has jurisdiction over this action pursuant to Sections 21(d), 21(e), 21A(a)(1), and 27 of the Exchange Act, 15 U.S.C. 8878u(d), 78u(e), 78u-1(a), and 78aa. 7. The Court has personal jurisdiction over Brooks and venue is proper in the Southern District of Florida because many of the acts and transactions constituting the violations alleged in this Complaint occurred in the Southern District of Florida. In addition, Brooks has a VI. DAB'S FINANCIAL FRAUD UNDER BROOKS 36. From at least 2003 through 2005, DHB materially misrepresented its inventory, cost of goods sold, gross profit, net income, and other key figures in its periodic reports and proxy statements filed with the Commission and its earnings releases, by overstating inventory values, falsifying journal entries, and failing to include appropriate charges for obsolete inventory 37. From at least 2003 through 2005, DHB reported in filings and press releases gross margins that met or exceeded 27%. In reality, during that time, DHB's actual gross profit margin was materially lower than 27%. As described in more detail below, DHB's 2006 Comprehensive 10-K contained restated financial statements for 2003, 2004, and 2005 stating the company's true gross profit margins in 2005, 2004, and 2003 were 18%, 18% and 14%, respectively. 38. Brooks touted DHB's consistently high gross profit margins in earnings releases, and he certified and signed periodic filings and proxy statements that fraudulently detailed the company's robust success. 39. Due to Brooks' in-depth involvement in DHB's operations, accounting, and finances, and countless discussions with Schlegel and Hatfield, Brooks knew or was extremely reckless in not knowing that even as DHB's stock hit record highs DHB's and his public statements were false and materially misleading, and DHB was not nearly as profitable as he and others portrayed it. A. Falsification of DHBs Inventory 40. Between 2003 and 2005, DHB overstated its inventory and created bogus, unsubstantiated bills to price its "work in process and "finished goods inventory. These fraudulent bills overstated labor costs, the amount of raw materials, overhead costs, and the unit prices of DHB's four primary vest components. 41. During this same three-year period, Brooks directly supervised Schlegel and Hatfield in performing all their duties, and demanded to review all financial statements and disclosures DHB included in its filings. 42. Throughout this three-year period, Schlegel supervised DHB's inventory accounting for all DHB subsidiaries. Hatfield was responsible for assigning values to the inventory and Schlegel was responsible for reviewing and approving the inventory valuation before incorporating it into the company's consolidated financial statements. 43. By overvaluing DHB's inventory, Schlegel and Hatfield were able to increase the company's reported gross profit and net income. Specifically, by overvaluing inventory, they reduced DHBs.cost of produsold which had the corresponding effect of increasing cose nonStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting

Authors: John Hoggett, Lew Edwards, John Medlin

6th Edition

0470806583, 978-0470806586