Answered step by step

Verified Expert Solution

Question

1 Approved Answer

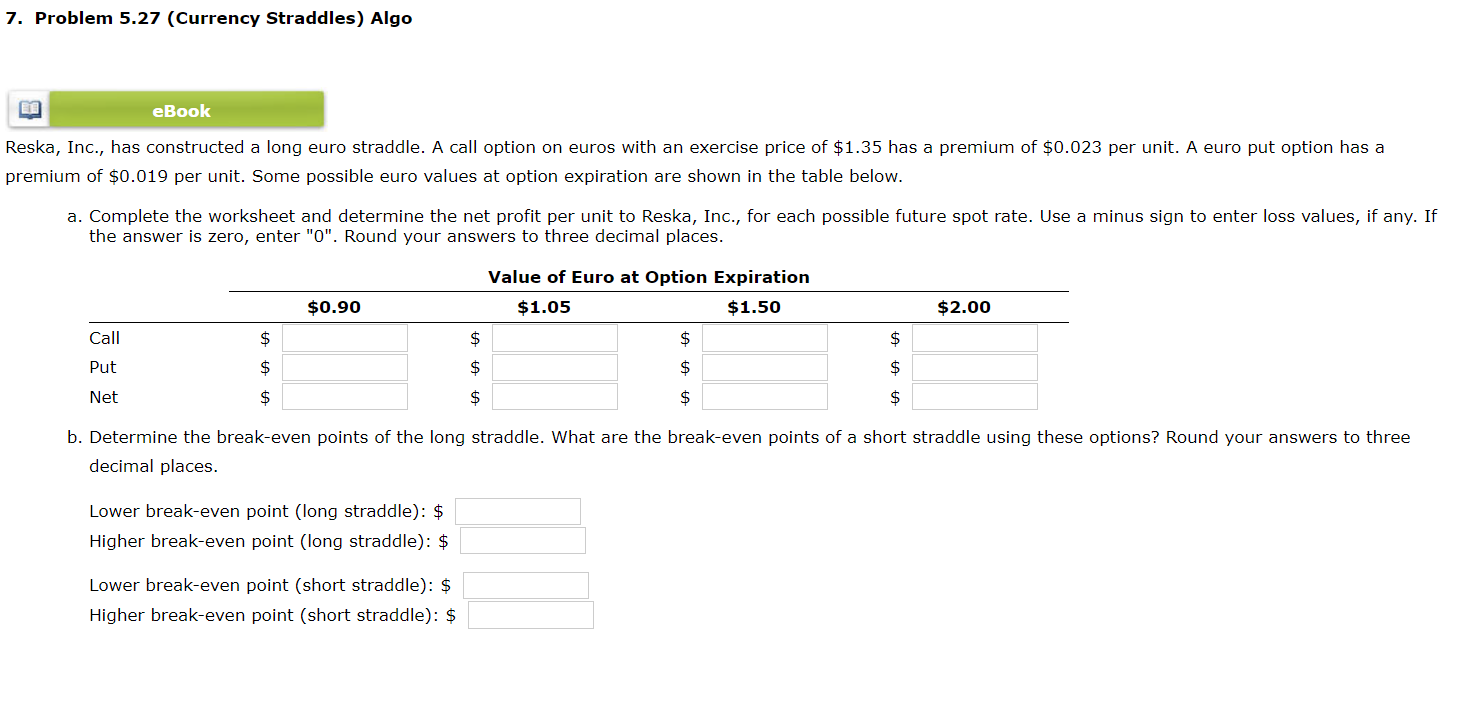

Reska, Inc., has constructed a long euro straddle. A call option on euros with an exercise price of $ 1 . 3 5 has a

Reska, Inc., has constructed a long euro straddle. A call option on euros with an exercise price of $ has a premium of $ per unit. A euro put option has a

premium of $ per unit. Some possible euro values at option expiration are shown in the table below.

a Complete the worksheet and determine the net profit per unit to Reska, Inc., for each possible future spot rate. Use a minus sign to enter loss values, if any. If

the answer is zero, enter Round your answers to three decimal places.

b Determine the breakeven points of the long straddle. What are the breakeven points of a short straddle using these options? Round your answers to three

decimal places.

Lower breakeven point long straddle: $

Higher breakeven point long straddle: $

Lower breakeven point short straddle: $

Higher breakeven point short straddle: $

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

A Course In Derivative Securities

Authors: Kerry Back

2005th Edition

3540253734, 978-3540253730