Answered step by step

Verified Expert Solution

Question

1 Approved Answer

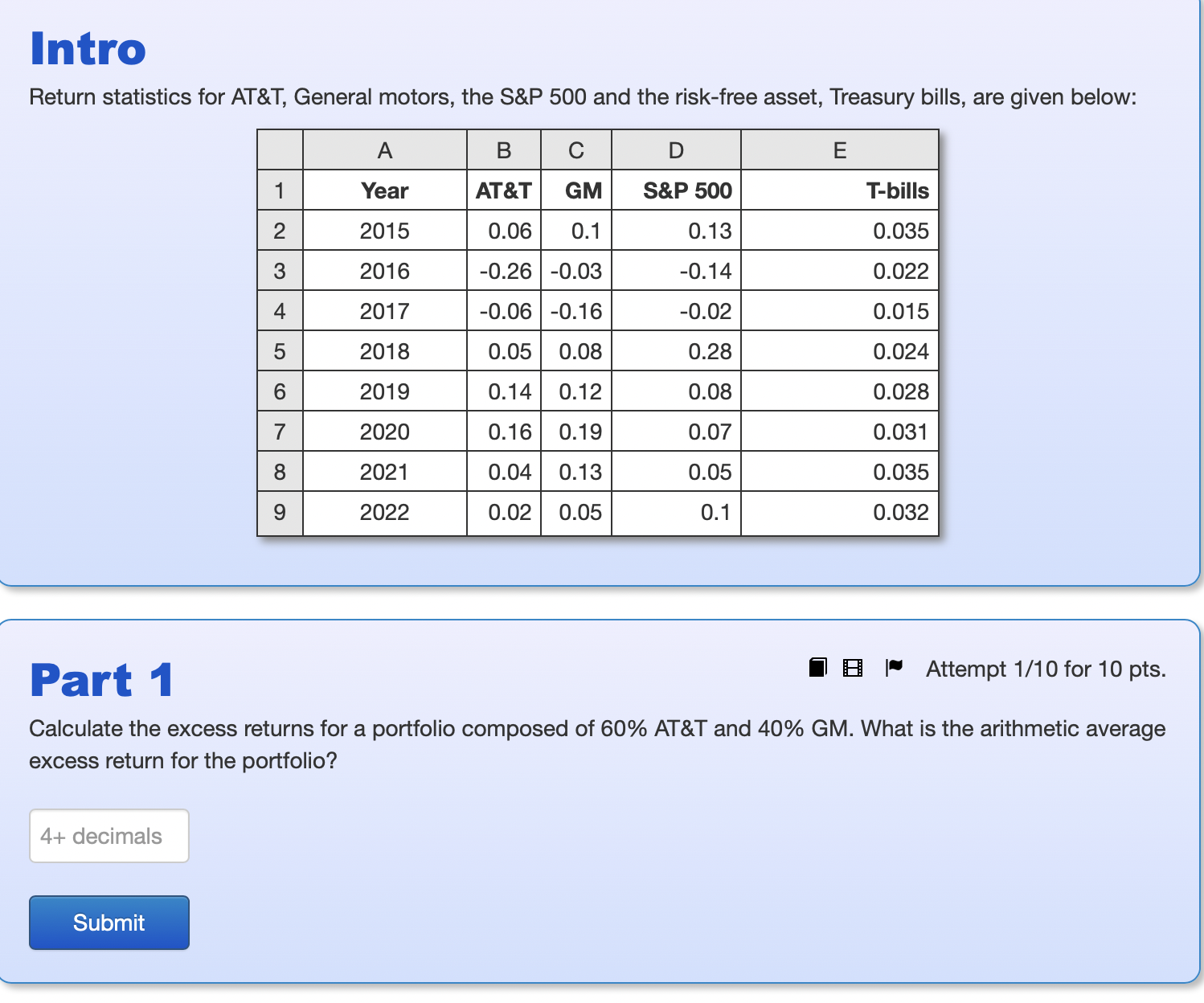

Return statistics for AT&T, General motors, the S&P 500 and the risk-free asset, Treasury bills, are given below: Part 1 Attempt 1/10 for 10 pts.

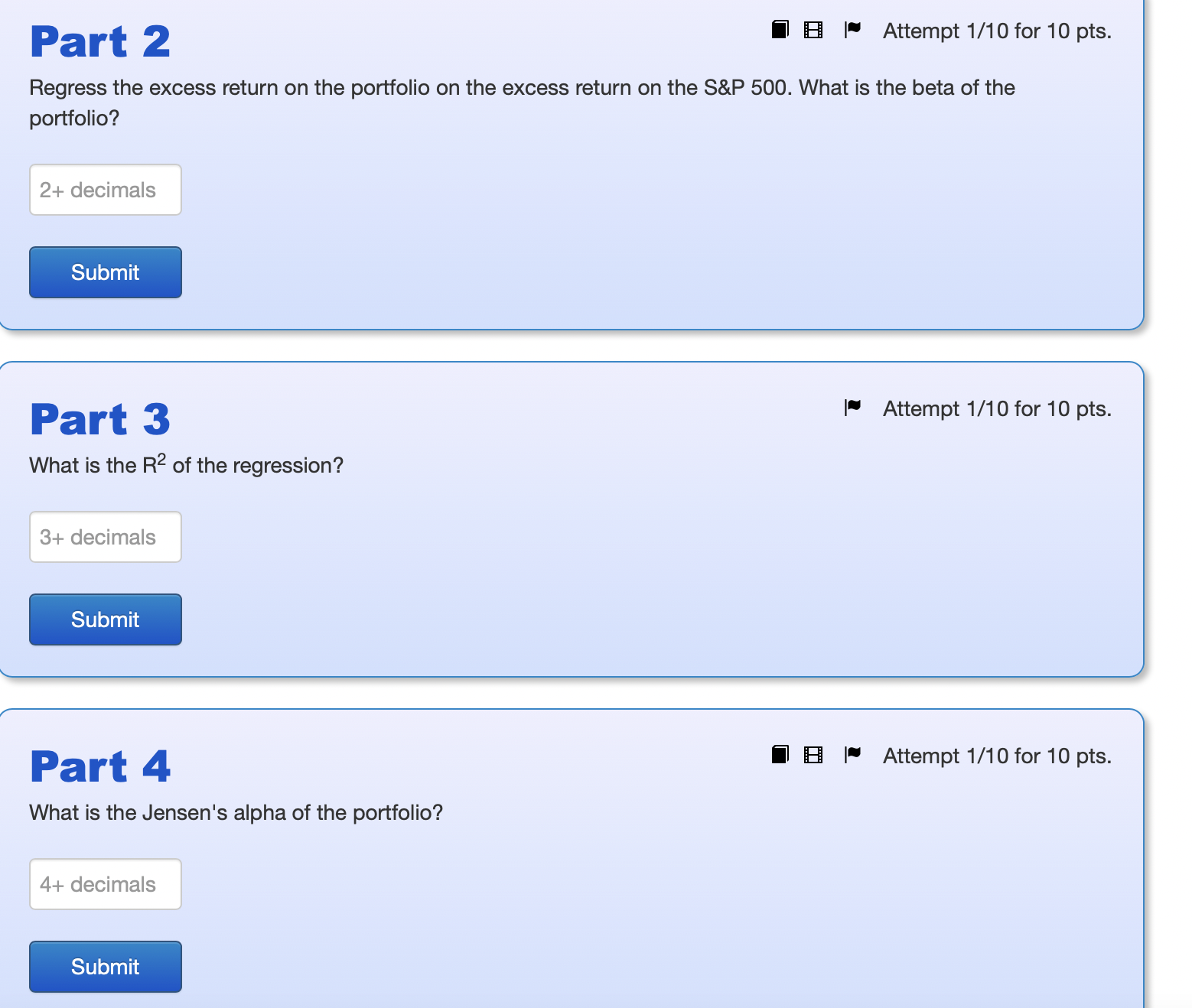

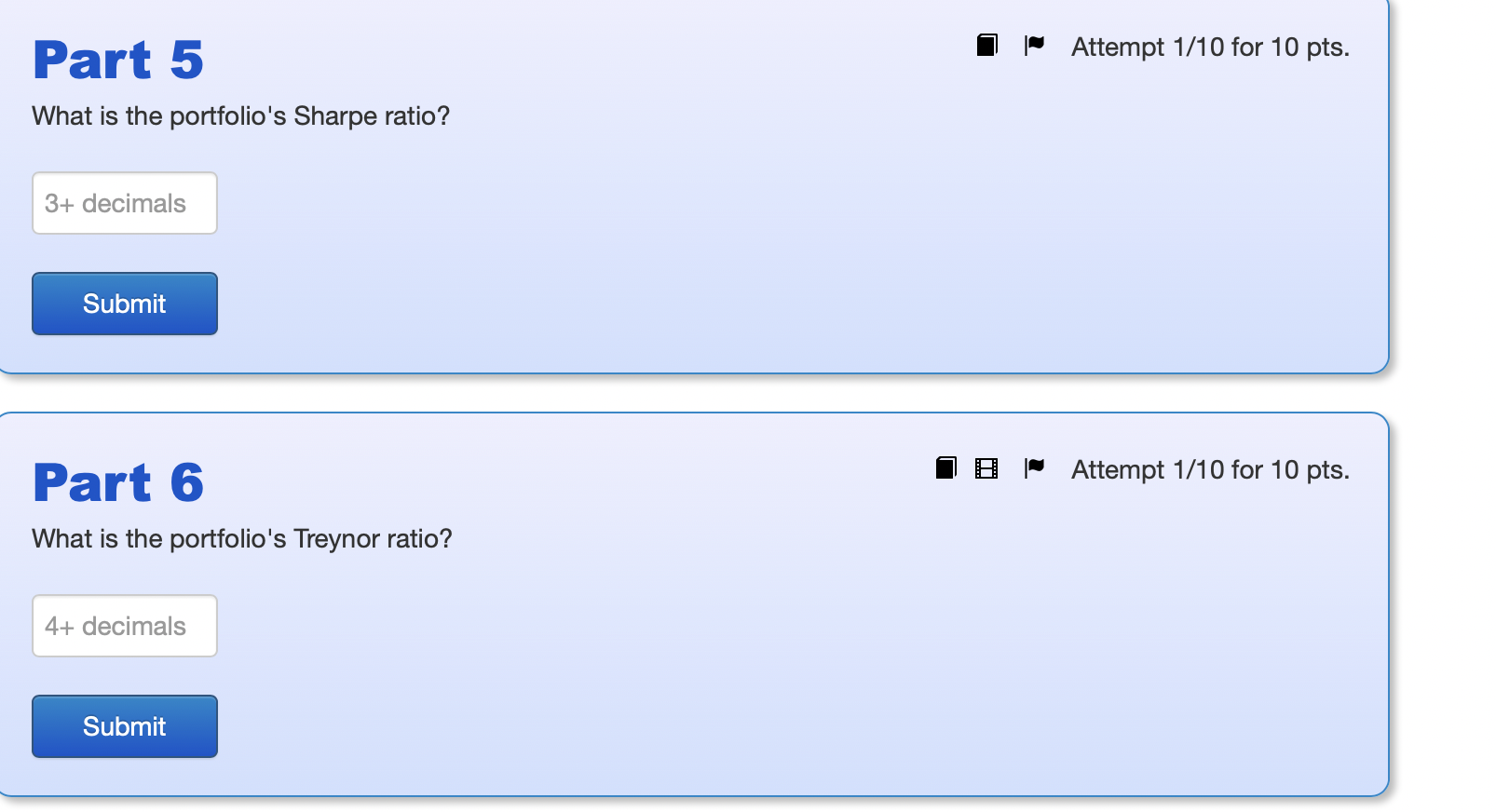

Return statistics for AT\&T, General motors, the S\&P 500 and the risk-free asset, Treasury bills, are given below: Part 1 Attempt 1/10 for 10 pts. Calculate the excess returns for a portfolio composed of 60% AT\&T and 40% GM. What is the arithmetic average excess return for the portfolio? Regress the excess return on the portfolio on the excess return on the S\&P 500. What is the beta of the portfolio? Part 3 Attempt 1/10 for 10 What is the R2 of the regression? Part 4 Attempt 1/10 for 10p What is the Jensen's alpha of the portfolio? What is the portfolio's Sharpe ratio? Part 6 What is the portfolio's Treynor ratio

Return statistics for AT\&T, General motors, the S\&P 500 and the risk-free asset, Treasury bills, are given below: Part 1 Attempt 1/10 for 10 pts. Calculate the excess returns for a portfolio composed of 60% AT\&T and 40% GM. What is the arithmetic average excess return for the portfolio? Regress the excess return on the portfolio on the excess return on the S\&P 500. What is the beta of the portfolio? Part 3 Attempt 1/10 for 10 What is the R2 of the regression? Part 4 Attempt 1/10 for 10p What is the Jensen's alpha of the portfolio? What is the portfolio's Sharpe ratio? Part 6 What is the portfolio's Treynor ratio Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Institutions Management

Authors: Anthony Saunders

1st Edition

0256110565, 9780256110562