Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Right click and open image in a new tab for full size. This question has two sub-questions and the data of the portfolios is given

Right click and open image in a new tab for full size.

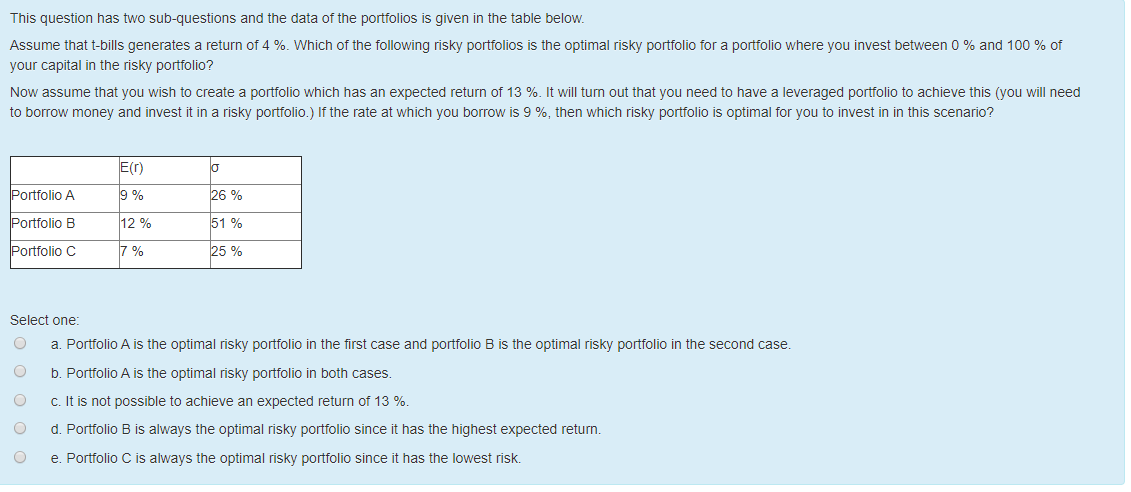

This question has two sub-questions and the data of the portfolios is given in the table below. Assume that t-bills generates a return of 4 %. Which of the following risky portfolios is the optimal risky portfolio for a portfolio where you invest between 0% and 100 % of your capital in the risky portfolio? Now assume that you wish to create a portfolio which has an expected return of 13 %. It will turn out that you need to have a leveraged portfolio to achieve this (you will need to borrow money and invest it in a risky portfolio.) If the rate at which you borrow is 9 %, then which risky portfolio is optimal for you to invest in in this scenario? EN 19% 26 % Portfolio A Portfolio B Portfolio C 51 % 12% 7 % Select one: a. Portfolio A is the optimal risky portfolio in the first case and portfolio B is the optimal risky portfolio in the second case. o o c d b. Portfolio A is the optimal risky portfolio in both cases. . It is not possible to achieve an expected return of 13 %. Portfolio B is always the optimal risky portfolio since it has the highest expected return. e. Portfolio C is always the optimal risky portfolio since it has the lowest riskStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Management And Policy

Authors: James C. Van Horne

12th Edition

0130326577, 9780130326577