Answered step by step

Verified Expert Solution

Question

1 Approved Answer

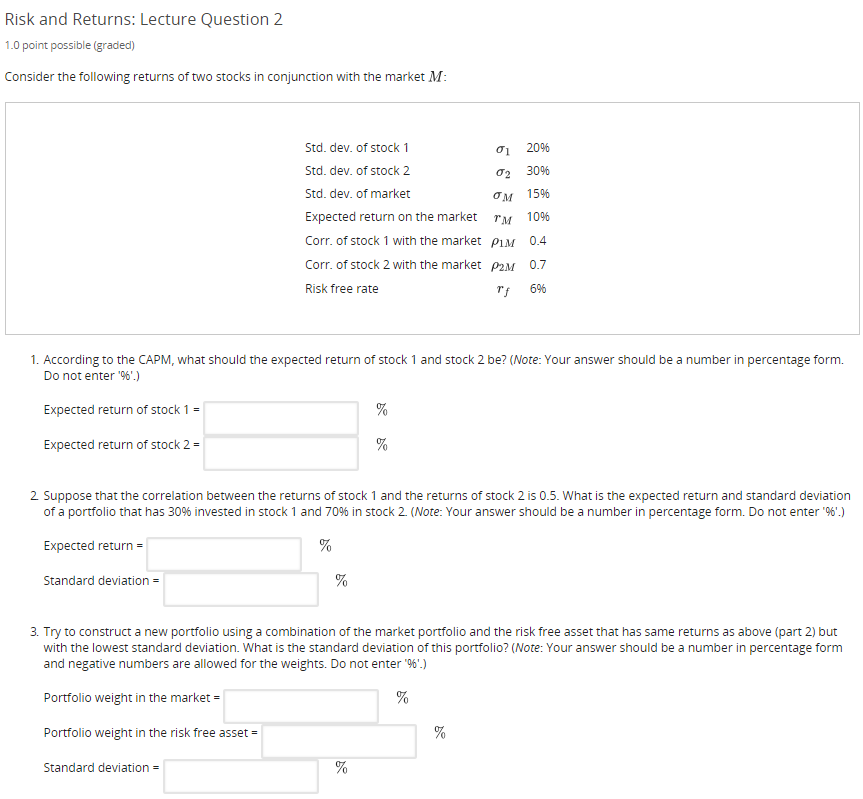

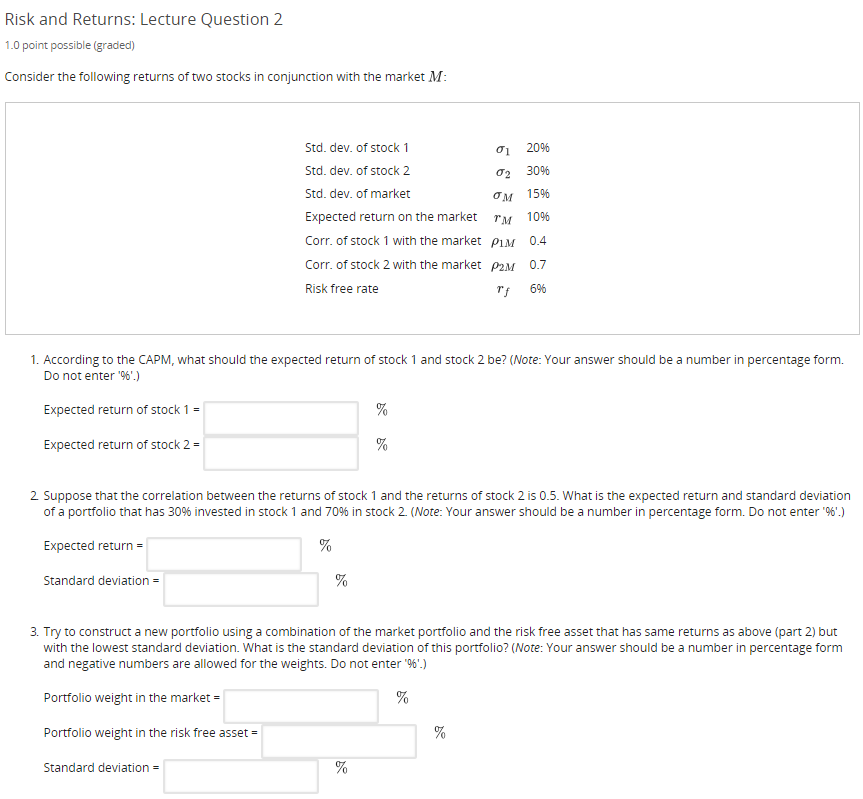

Risk and Returns: Lecture Question 2 1.0 point possible (graded) Consider the following returns of two stocks in conjunction with the market M: Std.

Risk and Returns: Lecture Question 2 1.0 point possible (graded) Consider the following returns of two stocks in conjunction with the market M: Std. dev. of stock 1 20% Std. dev. of stock 2 02 30% Std. dev. of market 15% Expected return on the market r 10% Corr. of stock 1 with the market PIM 0.4 Corr. of stock 2 with the market P2M 0.7 Risk free rate rf 6% 1. According to the CAPM, what should the expected return of stock 1 and stock 2 be? (Note: Your answer should be a number in percentage form. Do not enter '%'.) Expected return of stock 1 = Expected return of stock 2 = % % 2. Suppose that the correlation between the returns of stock 1 and the returns of stock 2 is 0.5. What is the expected return and standard deviation of a portfolio that has 30% invested in stock 1 and 70% in stock 2. (Note: Your answer should be a number in percentage form. Do not enter '%'.) Expected return= % Standard deviation = % 3. Try to construct a new portfolio using a combination of the market portfolio and the risk free asset that has same returns as above (part 2) but with the lowest standard deviation. What is the standard deviation of this portfolio? (Note: Your answer should be a number in percentage form and negative numbers are allowed for the weights. Do not enter '%'.) Portfolio weight in the market = % Portfolio weight in the risk free asset = % Standard deviation = %

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Markets and Institutions

Authors: Frederic S. Mishkin, Stanley G. Eakins

5th edition

321280299, 321280296, 978-0321280299