Answered step by step

Verified Expert Solution

Question

1 Approved Answer

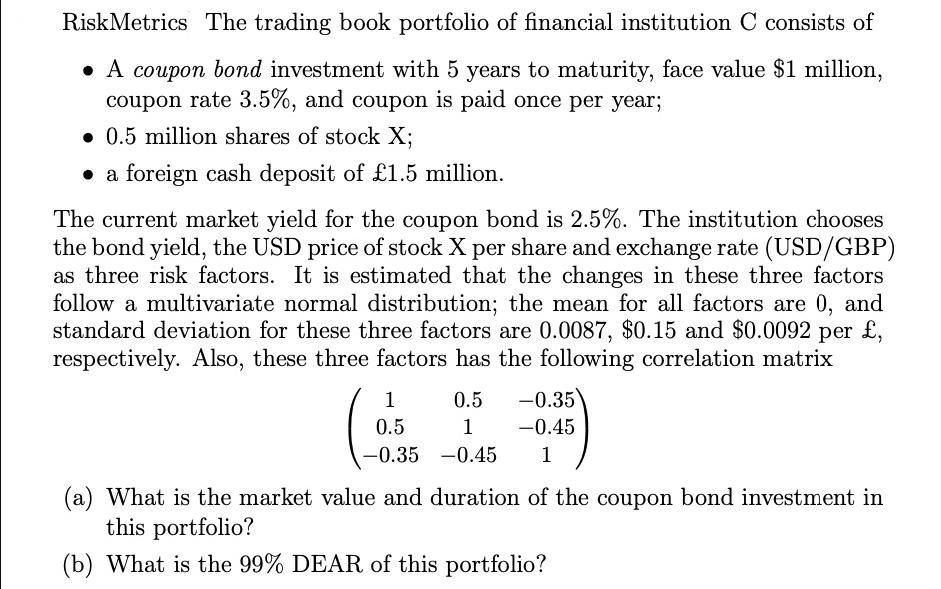

RiskMetrics The trading book portfolio of financial institution C consists of A coupon bond investment with 5 years to maturity, face value $1 million,

RiskMetrics The trading book portfolio of financial institution C consists of A coupon bond investment with 5 years to maturity, face value $1 million, coupon rate 3.5%, and coupon is paid once per year; 0.5 million shares of stock X; a foreign cash deposit of 1.5 million. The current market yield for the coupon bond is 2.5%. The institution chooses the bond yield, the USD price of stock X per share and exchange rate (USD/GBP) as three risk factors. It is estimated that the changes in these three factors follow a multivariate normal distribution; the mean for all factors are 0, and standard deviation for these three factors are 0.0087, $0.15 and $0.0092 per , respectively. Also, these three factors has the following correlation matrix 1 0.5 -0.35 0.5 1 -0.45 -0.35 -0.45 1 (a) What is the market value and duration of the coupon bond investment in this portfolio? (b) What is the 99% DEAR of this portfolio?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Essentials of Corporate Finance

Authors: Stephen Ross, Randolph Westerfield, Bradford Jordan

10th edition

1260013955, 1260013952, 978-1260013955