Answered step by step

Verified Expert Solution

Question

1 Approved Answer

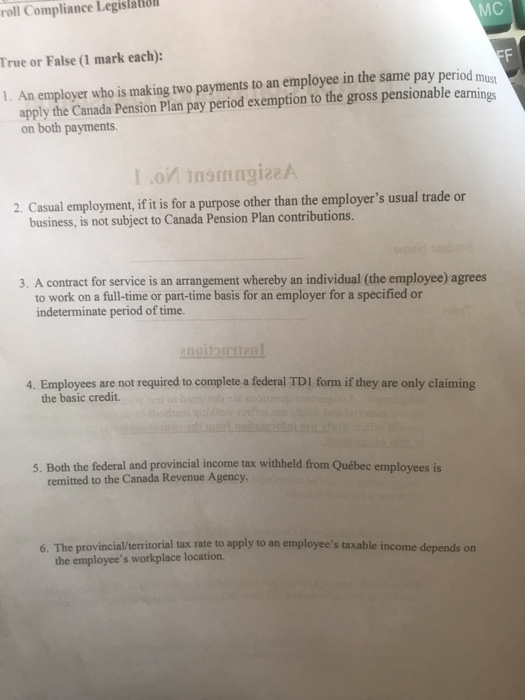

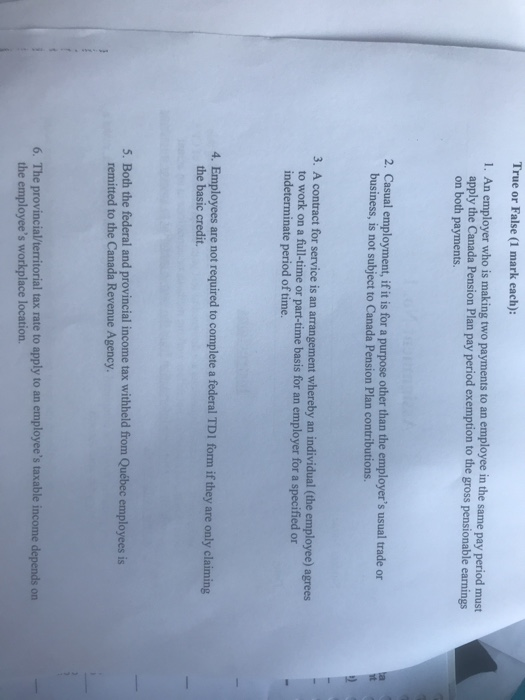

roll Compliance Legislation MC True or False (1 mark each): 1. An employer who is making two payments to an employee in the same pay

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Study Guide For Use With Managerial Accounting

Authors: Ronald M. Copeland, Paul E. Dascher, Jerry R. Strawser, Robert H. Strawser

1st Edition

0873937651, 978-0873937658