Question: Roomrunner Security Solutions (RSS) is a global leader in the market for security monitoring systems. The company offers its clients two platform products: (i) camera

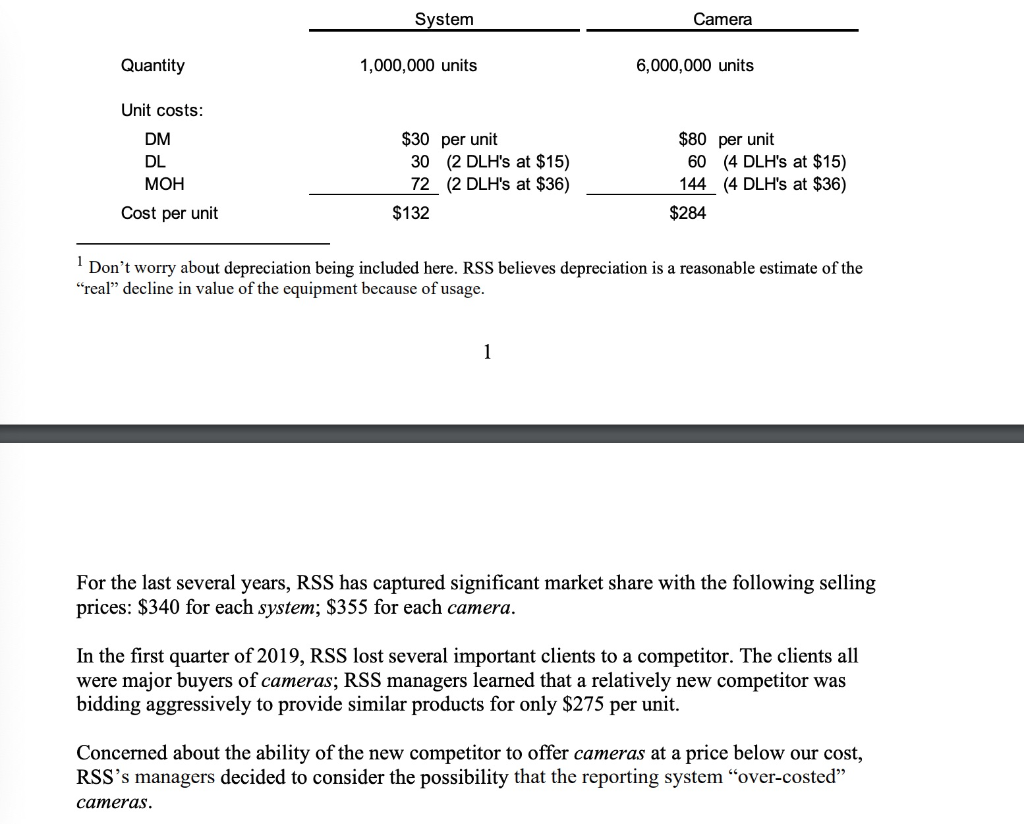

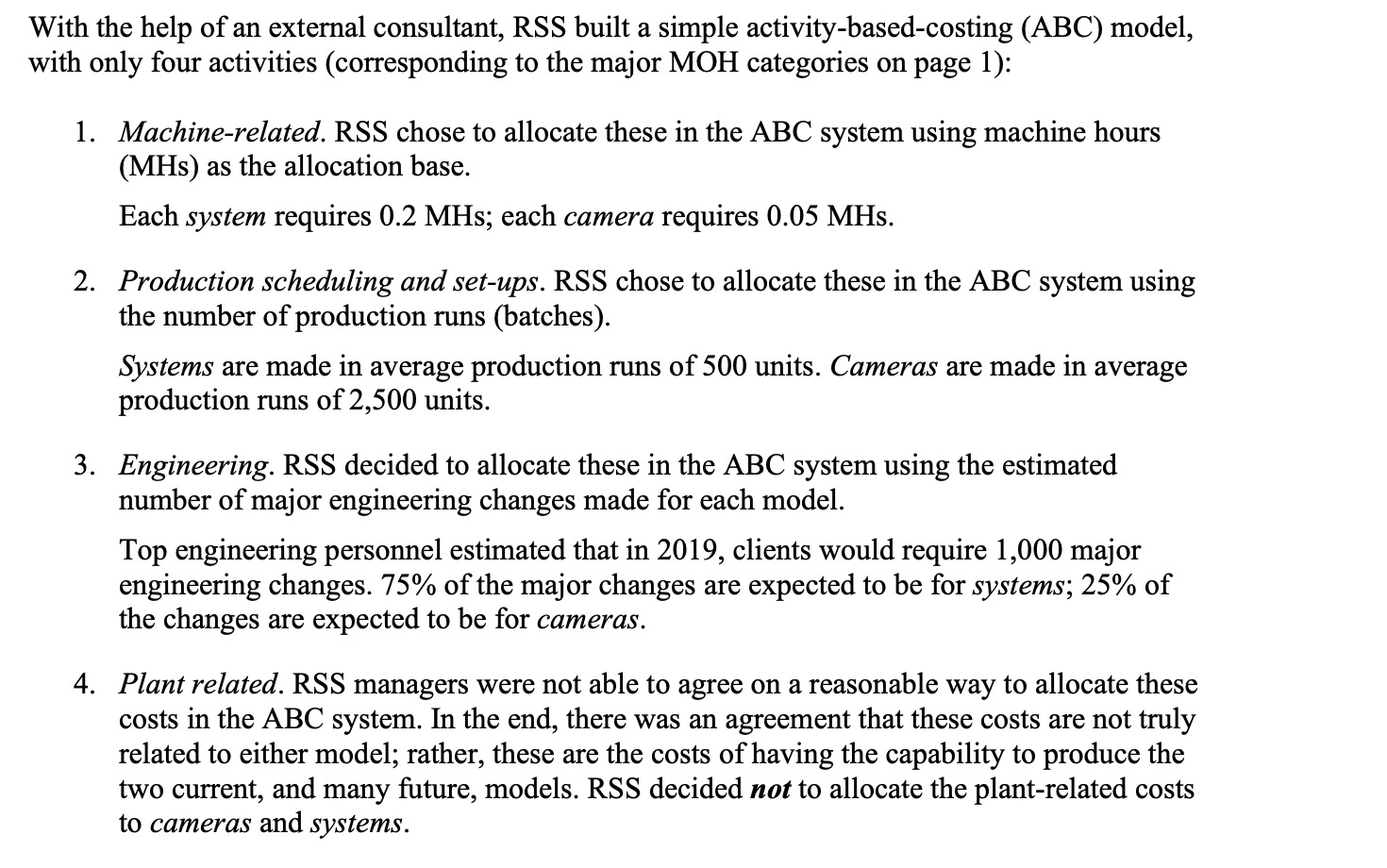

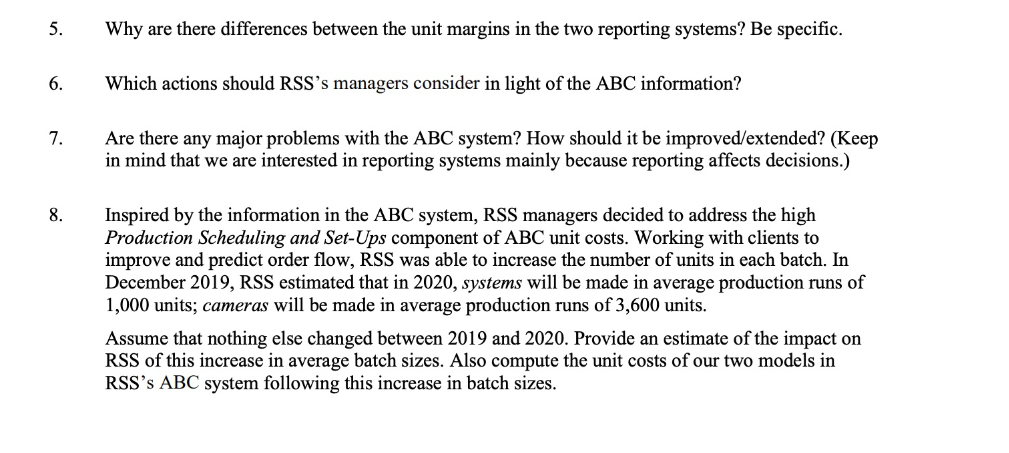

Roomrunner Security Solutions (RSS) is a global leader in the market for security monitoring systems. The company offers its clients two platform" products: (i) camera - a simple motion-detector camera, and (ii) system - a complex, integrated security system. The products are made under contract for other companies; our clients brand and sell the cameras and systems. Each "platform model can be heavily customized to a specific client's needs. Because we focus on manufacturing only, we don't have any SG&A expenses. To estimate unit margins and to support pricing, RSS uses normal absorption costing. The company's manufacturing overhead costs (MOH) are allocated using direct labor hours (DLHS). In 2019, the company's MOH costs included four major categories: 1. Machine-related costs. These include equipment depreciation, wear-and-tear, energy, and maintenance. These costs are largely variable. 2019 machine-related MOH costs were estimated at $500,000,000. 2. Production scheduling and set-ups. These are the indirect costs incurred when setting up equipment to produce a batch or either cameras or systems for a specific client. The costs include programming, engineering, and other labor devoted to production scheduling and set-ups; the extensive testing and quality control conducted on the first several units of each batch; and payments for process patents required to perform setups. These are largely capacity costs: in the short- and medium-run, these costs are largely fixed. 2019 production scheduling and set-up MOH costs were estimated at $200,000,000. 3. Engineering. These are the costs of development and engineering personnel and equipment. The costs are incurred to modify a model to specific client needs. These are largely capacity costs: in the short- and medium-run, these costs are largely fixed. 2019 engineering MOH costs were estimated at $100,000,000. 4. Plant related costs. These include the costs of renting, owning, maintaining, and managing the company's production facilities. 2019 plant-related MOH costs were estimated at $136,000,000. The company's 2019 unit sales and unit-cost estimates are below (this uses RSSs normal absorption costing with MOH allocated using DLHs as the allocation base): System Camera Quantity 1,000,000 units 6,000,000 units Unit costs: DM DL MOH $30 per unit 30 (2 DLH's at $15) 72 (2 DLH's at $36) $132 $80 per unit 60 (4 DLH's at $15) 144 (4 DLH's at $36) $284 Cost per unit Don't worry about depreciation being included here. RSS believes depreciation is a reasonable estimate of the "real" decline in value of the equipment because of usage. 1 For the last several years, RSS has captured significant market share with the following selling prices: $340 for each system; $355 for each camera. In the first quarter of 2019, RSS lost several important clients to a competitor. The clients all were major buyers of cameras; RSS managers learned that a relatively new competitor was bidding aggressively to provide similar products for only $275 per unit. Concerned about the ability of the new competitor to offer cameras at a price below our cost, RSS's managers decided to consider the possibility that the reporting system "over-costed cameras. With the help of an external consultant, RSS built a simple activity-based-costing (ABC) model, with only four activities (corresponding to the major MOH categories on page 1): 1. Machine-related. RSS chose to allocate these in the ABC system using machine hours (MHs) as the allocation base. Each system requires 0.2 MHs; each camera requires 0.05 MHs. 2. Production scheduling and set-ups. RSS chose to allocate these in the ABC system using the number of production runs (batches). Systems are made in average production runs of 500 units. Cameras are made in average production runs of 2,500 units. 3. Engineering. RSS decided to allocate these in the ABC system using the estimated number of major engineering changes made for each model. Top engineering personnel estimated that in 2019, clients would require 1,000 major engineering changes. 75% of the major changes are expected to be for systems; 25% of the changes are expected to be for cameras. 4. Plant related. RSS managers were not able to agree on a reasonable way to allocate these costs in the ABC system. In the end, there was an agreement that these costs are not truly related to either model; rather, these are the costs of having the capability to produce the two current, and many future, models. RSS decided not to allocate the plant-related costs to cameras and systems. 5. Why are there differences between the unit margins in the two reporting systems? Be specific. 6. Which actions should RSS's managers consider in light of the ABC information? 7. Are there any major problems with the ABC system? How should it be improved/extended? (Keep in mind that we are interested in reporting systems mainly because reporting affects decisions.) 8. Inspired by the information in the ABC system, RSS managers decided to address the high Production Scheduling and Set-Ups component of ABC unit costs. Working with clients to improve and predict order flow, RSS was able to increase the number of units in each batch. In December 2019, RSS estimated that in 2020, systems will be made in average production runs of 1,000 units; cameras will be made in average production runs of 3,600 units. Assume that nothing else changed between 2019 and 2020. Provide an estimate of the impact on RSS of this increase in average batch sizes. Also compute the unit costs of our two models in RSS's ABC system following this increase in batch sizes. Roomrunner Security Solutions (RSS) is a global leader in the market for security monitoring systems. The company offers its clients two platform" products: (i) camera - a simple motion-detector camera, and (ii) system - a complex, integrated security system. The products are made under contract for other companies; our clients brand and sell the cameras and systems. Each "platform model can be heavily customized to a specific client's needs. Because we focus on manufacturing only, we don't have any SG&A expenses. To estimate unit margins and to support pricing, RSS uses normal absorption costing. The company's manufacturing overhead costs (MOH) are allocated using direct labor hours (DLHS). In 2019, the company's MOH costs included four major categories: 1. Machine-related costs. These include equipment depreciation, wear-and-tear, energy, and maintenance. These costs are largely variable. 2019 machine-related MOH costs were estimated at $500,000,000. 2. Production scheduling and set-ups. These are the indirect costs incurred when setting up equipment to produce a batch or either cameras or systems for a specific client. The costs include programming, engineering, and other labor devoted to production scheduling and set-ups; the extensive testing and quality control conducted on the first several units of each batch; and payments for process patents required to perform setups. These are largely capacity costs: in the short- and medium-run, these costs are largely fixed. 2019 production scheduling and set-up MOH costs were estimated at $200,000,000. 3. Engineering. These are the costs of development and engineering personnel and equipment. The costs are incurred to modify a model to specific client needs. These are largely capacity costs: in the short- and medium-run, these costs are largely fixed. 2019 engineering MOH costs were estimated at $100,000,000. 4. Plant related costs. These include the costs of renting, owning, maintaining, and managing the company's production facilities. 2019 plant-related MOH costs were estimated at $136,000,000. The company's 2019 unit sales and unit-cost estimates are below (this uses RSSs normal absorption costing with MOH allocated using DLHs as the allocation base): System Camera Quantity 1,000,000 units 6,000,000 units Unit costs: DM DL MOH $30 per unit 30 (2 DLH's at $15) 72 (2 DLH's at $36) $132 $80 per unit 60 (4 DLH's at $15) 144 (4 DLH's at $36) $284 Cost per unit Don't worry about depreciation being included here. RSS believes depreciation is a reasonable estimate of the "real" decline in value of the equipment because of usage. 1 For the last several years, RSS has captured significant market share with the following selling prices: $340 for each system; $355 for each camera. In the first quarter of 2019, RSS lost several important clients to a competitor. The clients all were major buyers of cameras; RSS managers learned that a relatively new competitor was bidding aggressively to provide similar products for only $275 per unit. Concerned about the ability of the new competitor to offer cameras at a price below our cost, RSS's managers decided to consider the possibility that the reporting system "over-costed cameras. With the help of an external consultant, RSS built a simple activity-based-costing (ABC) model, with only four activities (corresponding to the major MOH categories on page 1): 1. Machine-related. RSS chose to allocate these in the ABC system using machine hours (MHs) as the allocation base. Each system requires 0.2 MHs; each camera requires 0.05 MHs. 2. Production scheduling and set-ups. RSS chose to allocate these in the ABC system using the number of production runs (batches). Systems are made in average production runs of 500 units. Cameras are made in average production runs of 2,500 units. 3. Engineering. RSS decided to allocate these in the ABC system using the estimated number of major engineering changes made for each model. Top engineering personnel estimated that in 2019, clients would require 1,000 major engineering changes. 75% of the major changes are expected to be for systems; 25% of the changes are expected to be for cameras. 4. Plant related. RSS managers were not able to agree on a reasonable way to allocate these costs in the ABC system. In the end, there was an agreement that these costs are not truly related to either model; rather, these are the costs of having the capability to produce the two current, and many future, models. RSS decided not to allocate the plant-related costs to cameras and systems. 5. Why are there differences between the unit margins in the two reporting systems? Be specific. 6. Which actions should RSS's managers consider in light of the ABC information? 7. Are there any major problems with the ABC system? How should it be improved/extended? (Keep in mind that we are interested in reporting systems mainly because reporting affects decisions.) 8. Inspired by the information in the ABC system, RSS managers decided to address the high Production Scheduling and Set-Ups component of ABC unit costs. Working with clients to improve and predict order flow, RSS was able to increase the number of units in each batch. In December 2019, RSS estimated that in 2020, systems will be made in average production runs of 1,000 units; cameras will be made in average production runs of 3,600 units. Assume that nothing else changed between 2019 and 2020. Provide an estimate of the impact on RSS of this increase in average batch sizes. Also compute the unit costs of our two models in RSS's ABC system following this increase in batch sizes

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts