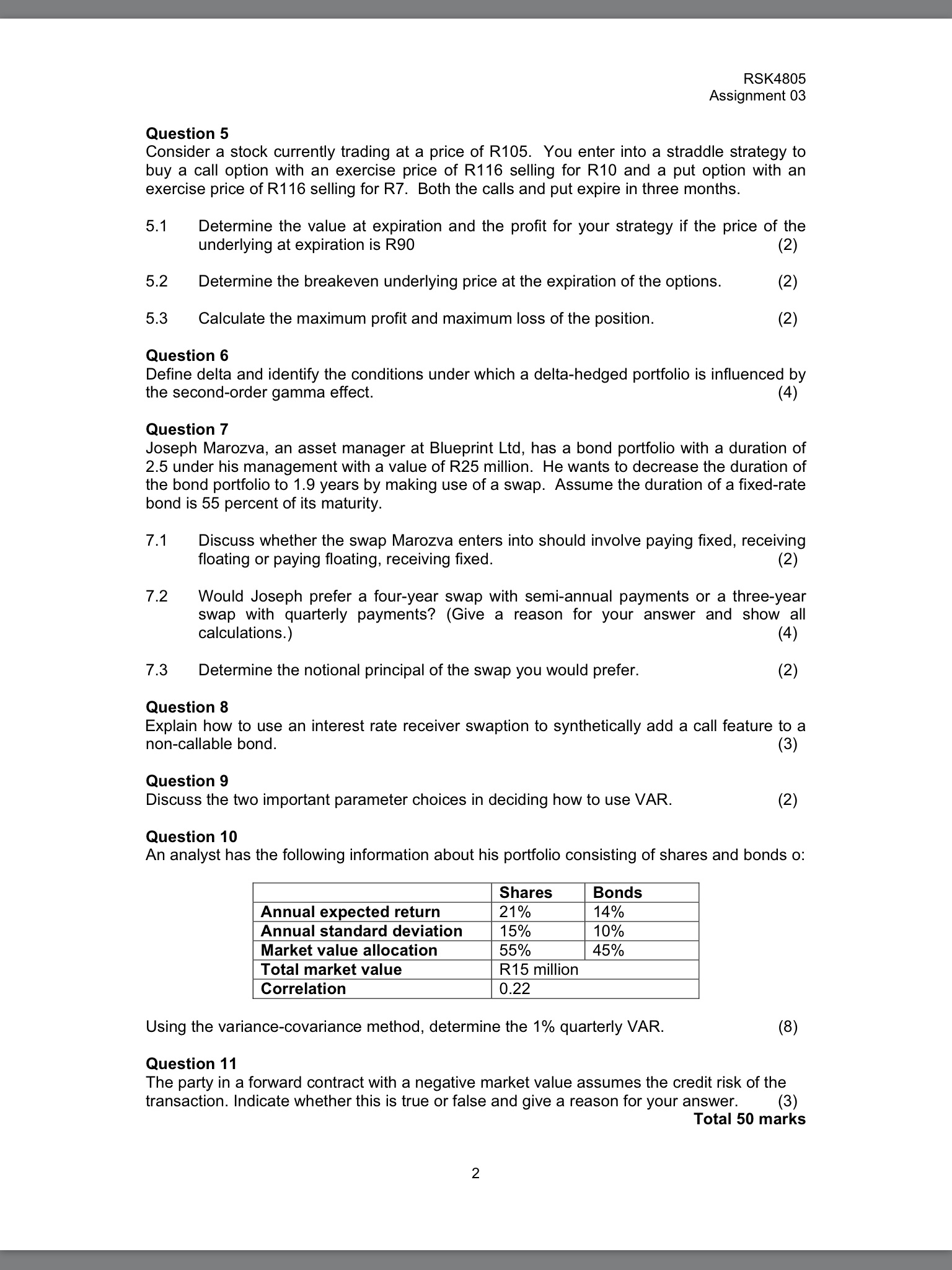

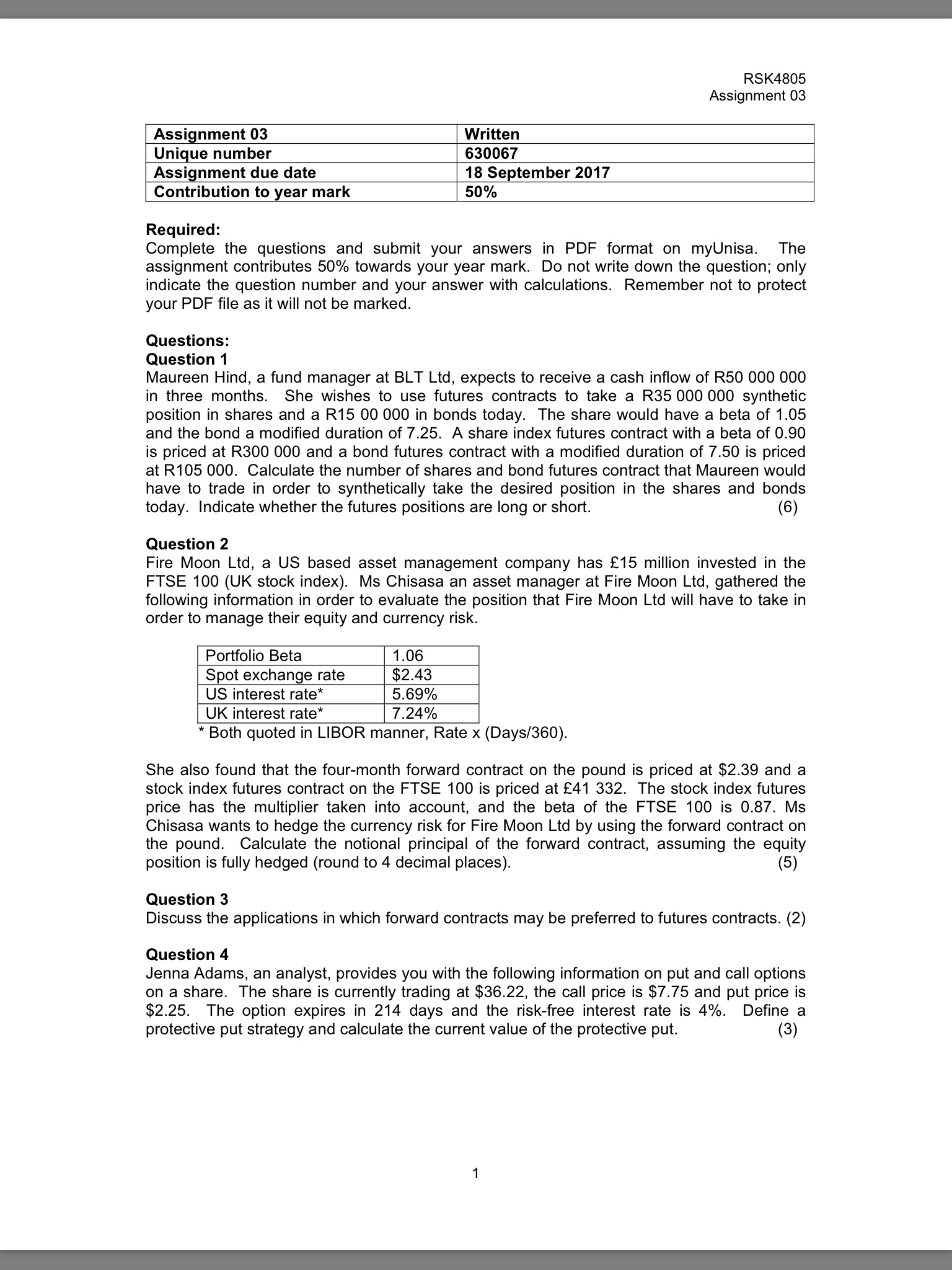

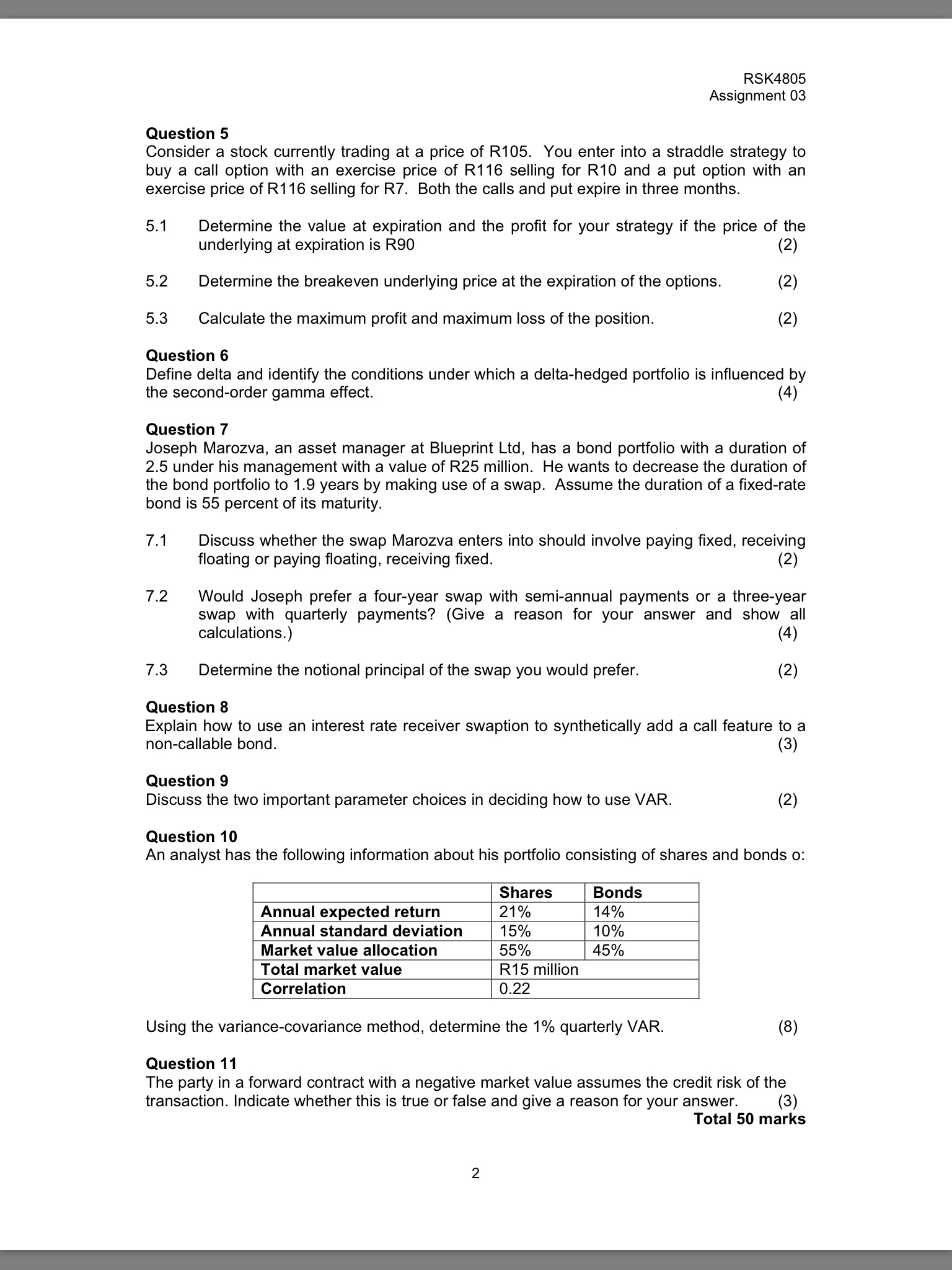

RSK4805 Assignment 03 Assignment 03 Written Unique number 630057 Assignment due date 18 September 2017 Contribution to year mark 50% Required: Complete the questions and submit your answers in PDF format on myUnisa. The assignment contributes 50% towards your year mark. Do not write down the question; only indicate the question number and your answer with calculations. Remember not to protect your PDF le as it will not be marked. Questions: Question 1 Maureen Hind, a fund manager at BLT Ltd, expects to receive a cash inow of R50 000 000 in three months. She wishes to use futures contracts to take a R35 000 000 synthetic position in shares and a R15 00 000 in bonds today. The share would have a beta of 1.05 and the bond a modied duration of 7.25. A share index futures contract with a beta of 0.90 is priced at R300 000 and a bond futures contract with a modied duration of 7.50 is priced at R105 000. Calculate the number of shares and bond futures contract that Maureen would have to trade in order to synthetically take the desired position in the shares and bonds today. Indicate whether the futures positions are long or short. (6) Question 2 Fire Moon Ltd, a US based asset management company has 15 million invested in the FTSE 100 (UK stock index). Ms Chisasa an asset manager at Fire Moon Ltd, gathered the following information in order to evaluate the position that Fire Moon Ltd will have to take in order to manage their equity and currency risk. Portfolio Beta Spot exchan -e rate $2.43 US interest rate" 5.69% UK interest rate\" 7.24% * Both quoted in LIBOR manner, Rate x (Days/360). She also found that the four-month forward contract on the pound is priced at $2.39 and a stock index futures contract on the FTSE 100 is priced at 41 332. The stock index futures price has the multiplier taken into account, and the beta of the FTSE 100 is 0.87. Ms Chisasa wants to hedge the currency risk for Fire Moon Ltd by using the forward contract on the pound. Calculate the notional principal of the forward contract, assuming the equity position is fully hedged (round to 4 decimal places). (5) Question 3 Discuss the applications in which forward contracts may be preferred to futures contracts. (2) Question 4 Jenna Adams, an analyst, provides you with the following information on put and call options on a share. The share is currently trading at $36.22, the call price is $7.75 and put price is $2.25. The option eXpires in 214 days and the risk-free interest rate is 4%. Define a protective put strategy and calculate the current value of the protective put. (3) RSK4805 Assignment 03 Question 5 Consider a stock currently trading at a price of R105. You enter into a straddle strategy to buy a call option with an exercise price of R116 selling for R10 and a put option with an exercise price of R116 selling for R7. Both the calls and put expire in three months. 5.1 Determine the value at expiration and the prot for your strategy if the price of the underlying at expiration is R90 (2) 5.2 Determine the breakeven underlying price at the expiration of the options. (2) 5.3 Calculate the maximum profit and maximum loss of the position. (2) Question 6 Define delta and identify the conditions under which a delta-hedged portfolio is inuenced by the second-order gamma effect. (4) Question 7 Joseph Marozva, an asset manager at Blueprint Ltd, has a bond portfolio with a duration of 2.5 under his management with a value of R25 million. He wants to decrease the duration of the bond portfolio to 1.9 years by making use of a swap. Assume the duration of a fixed-rate bond is 55 percent of its maturity. 7.1 Discuss whether the swap Marozva enters into should involve paying xed, receiving floating or paying oating, receiving xed. (2) 7.2 Would Joseph prefer a four-year swap with semi-annual payments or a three-year swap with quarterly payments? (Give a reason for your answer and show all calculations.) (4) 7.3 Determine the notional principal of the swap you would prefer. (2) Question 8 Explain how to use an interest rate receiver swaption to synthetically add a call feature to a non-callable bond. (3) Question 9 Discuss the two important parameter choices in deciding how to use VAR. (2) Question 10 An analyst has the following information about his portfolio consisting of shares and bonds 0: Emt- Annual expected return Annual standard deviation Market value allocation Total market value R15 million Using the variance-covariance method, determine the 1% quarterly VAR. (8) Question 11 The party in a forward contract with a negative market value assumes the credit risk of the transaction. Indicate whether this is true or false and give a reason for your answer. (3) Total 50 marks