Answered step by step

Verified Expert Solution

Question

1 Approved Answer

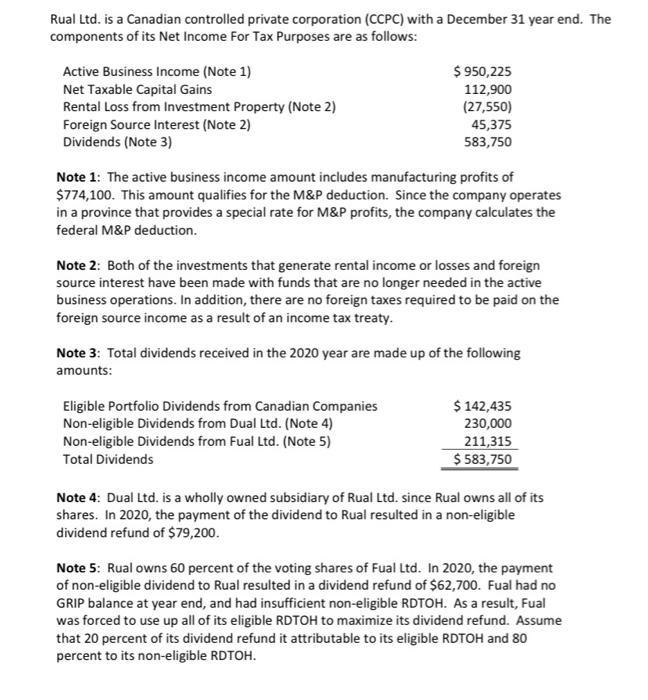

Rual Ltd. is a Canadian controlled private corporation (CCPC) with a December 31 year end. The components of its Net Income For Tax Purposes

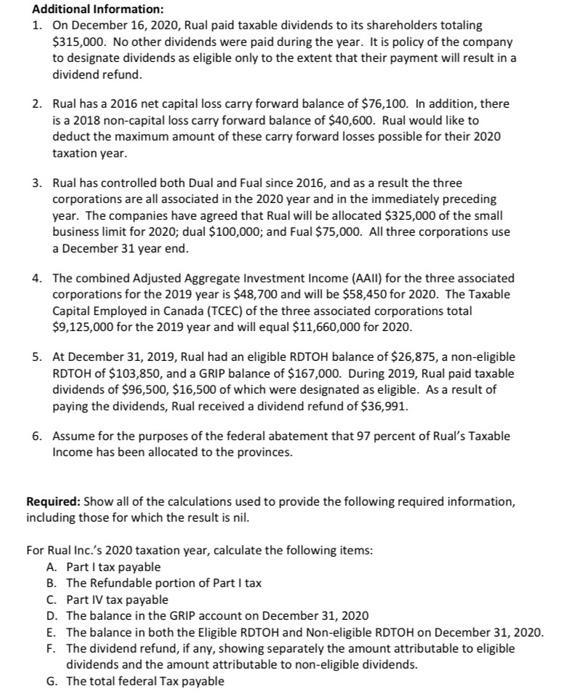

Rual Ltd. is a Canadian controlled private corporation (CCPC) with a December 31 year end. The components of its Net Income For Tax Purposes are as follows: Active Business Income (Note 1) Net Taxable Capital Gains Rental Loss from Investment Property (Note 2) Foreign Source Interest (Note 2) Dividends (Note 3) $ 950,225 112,900 (27,550) 45,375 583,750 Note 1: The active business income amount includes manufacturing profits of $774,100. This amount qualifies for the M&P deduction. Since the company operates in a province that provides a special rate for M&P profits, the company calculates the federal M&P deduction. Note 2: Both of the investments that generate rental income or losses and foreign source interest have been made with funds that are no longer needed in the active business operations. In addition, there are no foreign taxes required to be paid on the foreign source income as a result of an income tax treaty. Note 3: Total dividends received in the 2020 year are made up of the following amounts: Eligible Portfolio Dividends from Canadian Companies Non-eligible Dividends from Dual Ltd. (Note 4) Non-eligible Dividends from Fual Ltd. (Note 5) Total Dividends $ 142,435 230,000 211,315 $ 583,750 Note 4: Dual Ltd. is a wholly owned subsidiary of Rual Ltd. since Rual owns all of its shares. In 2020, the payment of the dividend to Rual resulted in a non-eligible dividend refund of $79,200. Note 5: Rual owns 60 percent of the voting shares of Fual Ltd. In 2020, the payment of non-eligible dividend to Rual resulted in a dividend refund of $62,700. Fual had no GRIP balance at year end, and had insufficient non-eligible RDTOH. As a result, Fual was forced to use up all of its eligible RDTOH to maximize its dividend refund. Assume that 20 percent of its dividend refund it attributable to its eligible RDTOH and 80 percent to its non-eligible RDTOH. Additional Information: 1. On December 16, 2020, Rual paid taxable dividends to its shareholders totaling $315,000. No other dividends were paid during the year. It is policy of the company to designate dividends as eligible only to the extent that their payment will result in a dividend refund. 2. Rual has a 2016 net capital loss carry forward balance of $76,100. In addition, there is a 2018 non-capital loss carry forward balance of $40,600. Rual would like to deduct the maximum amount of these carry forward losses possible for their 2020 taxation year. 3. Rual has controlled both Dual and Fual since 2016, and as a result the three corporations are all associated in the 2020 year and in the immediately preceding year. The companies have agreed that Rual will be allocated $325,000 of the small business limit for 2020; dual $100,000; and Fual $75,000. All three corporations use a December 31 year end. 4. The combined Adjusted Aggregate Investment Income (AAII) for the three associated corporations for the 2019 year is $48,700 and will be $58,450 for 2020. The Taxable Capital Employed in Canada (TCEC) of the three associated corporations total $9,125,000 for the 2019 year and will equal $11,660,000 for 2020. 5. At December 31, 2019, Rual had an eligible RDTOH balance of $26,875, a non-eligible RDTOH of $103,850, and a GRIP balance of $167,000. During 2019, Rual paid taxable dividends of $96,500, $16,500 of which were designated as eligible. As a result of paying the dividends, Rual received a dividend refund of $36,991. 6. Assume for the purposes of the federal abatement that 97 percent of Rual's Taxable Income has been allocated to the provinces. Required: Show all of the calculations used to provide the following required information, including those for which the result is nil. For Rual Inc.'s 2020 taxation year, calculate the following items: A. Part I tax payable B. The Refundable portion of Part I tax C. Part IV tax payable D. The balance in the GRIP account on December 31, 2020 E. The balance in both the Eligible RDTOH and Non-eligible RDTOH on December 31, 2020. F. The dividend refund, if any, showing separately the amount attributable to eligible dividends and the amount attributable to non-eligible dividends. G. The total federal Tax payable

Step by Step Solution

★★★★★

3.46 Rating (162 Votes )

There are 3 Steps involved in it

Step: 1

Lets go step by step to calculate the required information for Rual Incs 2020 taxation year A Part I Tax Payable 1 Calculate the federal Part I tax on ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Canadian Income Taxation Planning And Decision Making

Authors: Joan Kitunen, William Buckwold

17th Edition 2014-2015 Version

1259094332, 978-1259094330