| Sales Budget |

| | Quarter | |

| | 1 | 2 | 3 | 4 | Year |

| Expected Unit sales | 40,200 | 11,200 | 47,600 | 87,300 | 1,86,300 |

| Unit selling price | 455 | 455 | 455 | 455 | 455 |

| Total sales | 1,82,91,000 | 50,96,000 | 2,16,58,000 | 3,97,21,500 | 8,47,66,500 |

| | | | | | |

| Production Budget |

| | Quarter | |

| | 1 | 2 | 3 | 4 | Year |

| Total sales | 40,200 | 11,200 | 47,600 | 87,300 | 1,86,300 |

| Desired Ending Finished Goods | | 2464 | 10472 | 19206 | 13552 | 13552 |

| | 42,664 | 21,672 | 66,806 | 1,00,852 | 1,99,852 |

| Beginning finished goods | 8,844 | 2464 | 10472 | 19206 | 8844 |

| Total production | 33,820 | 19,208 | 56,334 | 81,646 | 1,91,008 |

| | | | | | |

| Direct material Budget |

| | Quarter | |

| | 1 | 2 | 3 | 4 | Year |

| Budgeted production | 33,820 | 19,208 | 56,334 | 81,646 | 1,91,008 |

| raw material required for 1 unit | 8 | 8 | 8 | 8 | 8 |

| Total Raw material Required | 2,70,560 | 1,53,664 | 4,50,672 | 6,53,168 | 15,28,064 |

| Add: Ending Raw material | 12,544 | 53,312 | 97,776 | 68,992 | 68,992 |

| Less: Opening raw material | 45,024 | 12,544 | 53,312 | 97,776 | 45,024 |

| Total raw material purchase | 2,38,080 | 1,94,432 | 4,95,136 | 6,24,384 | 15,52,032 |

| Cost of 1 pound | 5.69 | 5.69 | 5.69 | 5.69 | 5.69 |

| Cost of Material purchased | 13,54,675 | 11,06,318 | 28,17,324 | 35,52,745 | 88,31,062 |

| | | | | | |

| Direct labour budget |

| | Quarter | |

| | 1 | 2 | 3 | 4 | Year |

| Budgeted production | 33,820 | 19,208 | 56,334 | 81,646 | 1,91,008 |

| Direct labour hour per unit | 3 | 3 | 3 | 3 | 3 |

| Total hour needed | 1,01,460 | 57,624 | 1,69,002 | 2,44,938 | 5,73,024 |

| wages per hour | 75.83 | 75.83 | 75.83 | 75.83 | 75.83 |

| Total direct labour cost | 76,93,712 | 43,69,628 | 1,28,15,422 | 1,85,73,649 | 4,34,52,410 |

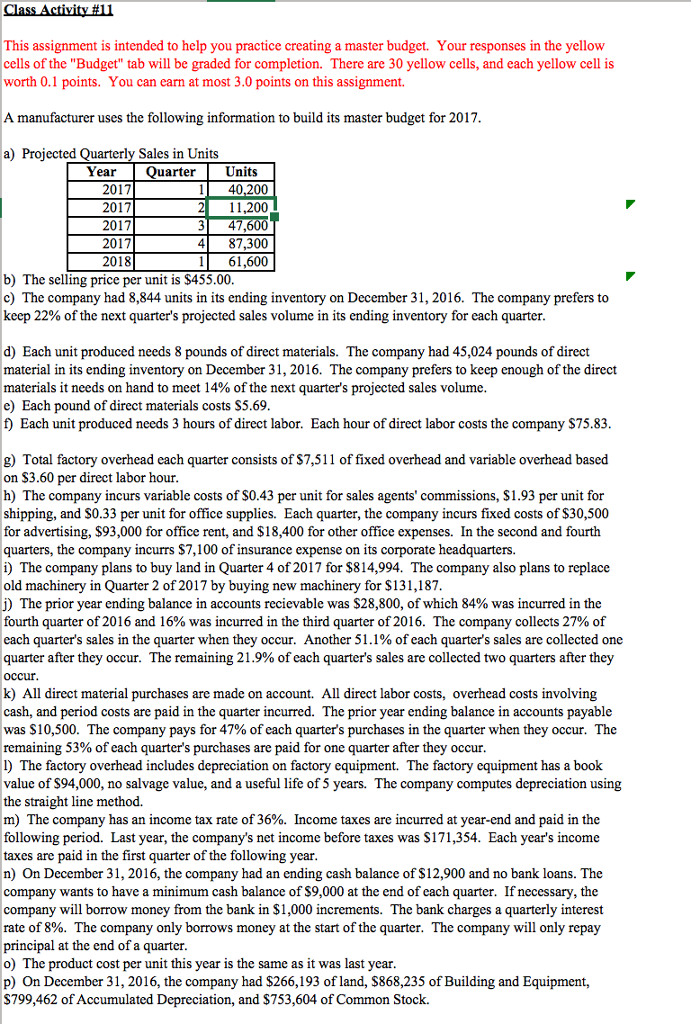

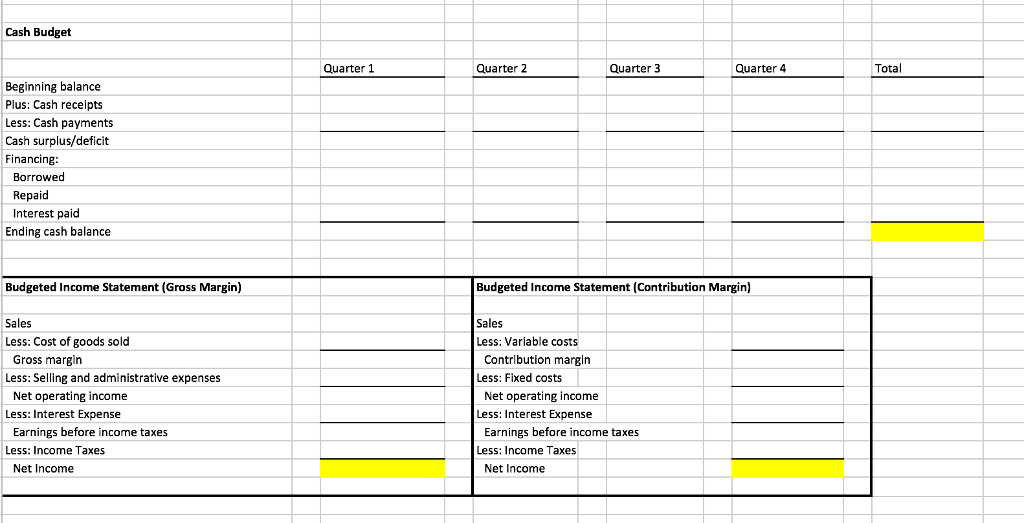

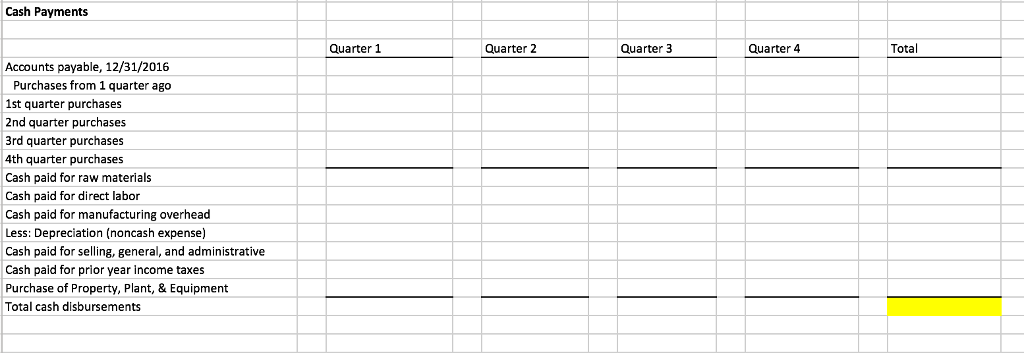

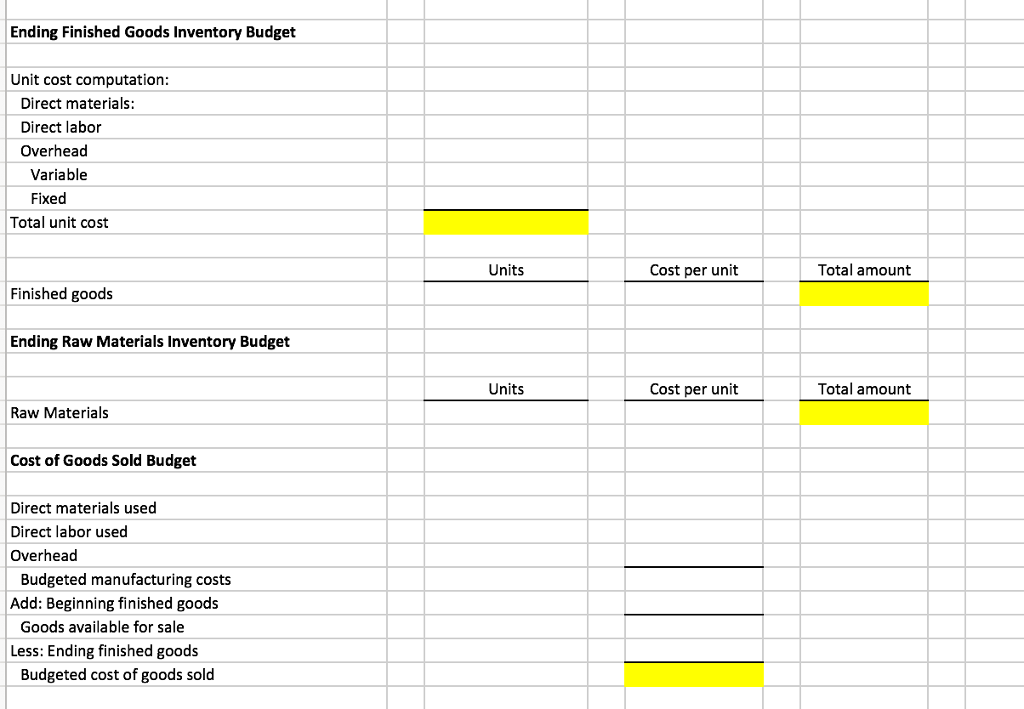

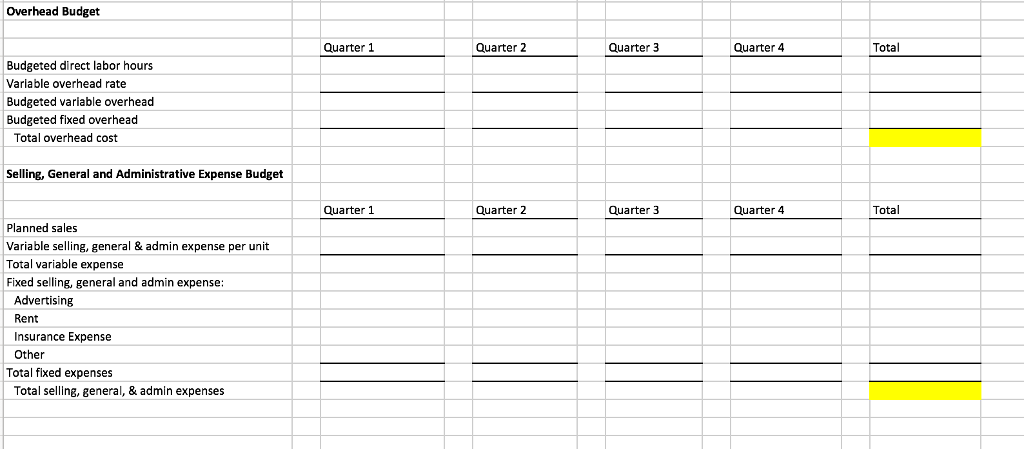

Class Activity This assignment is intended to help you practice creating a master budget. Your responses in the yellow cells of the "Budget" tab will be graded for completion. There are 30 yellow cells, and each yellow cell is worth 0.1 points. You can earn at most 3.0 points on this assignment. A manufacturer uses the following information to build its master budget for 2017 a) Projected Quarterly Sales in Units Year Quarter Units 2017 1 40,200 2017 2 11,200 2017 3 47600 2017 4 871300 2018 1 ,600 b) The selling price per unit is $455.00. c) The company had 8,844 units in its ending inventory on December 31, 2016. The company prefers to keep 22% of the next quarter's projected sales volume in its ending inventory for each quarter d) Each unit produced needs 8 pounds of direct materials. The company had 45,024 pounds of direct material in its ending inventory on December 31, 2016. The company prefers to keep enough of the direc materials it needs on hand to meet 14% of the next quarter's projected sales volume Each pound of direct materials costs S5.69 f) Each unit produced needs 3 hours of direct labor. Each hour of direct labor costs the company $75.83 g) Total factory overhead each quarter consists of S7,511 of fixed overhead and variable overhead based on $3.60 per direct labor hour h) The company incurs variable costs of $0.43 per unit for sales agents' commissions, $1.93 per unit for shipping, and S0.33 per unit for office supplies. Each quarter, the company incurs fixed costs of $30,500 for advertising, $93,000 for office rent, and $18,400 for other office expenses. In the second and fourth quarters, the company incurrs S7,100 of insurance expense on its corporate headquarters. The company plans to buy land in Quarter 4 of 2017 for $814,994. The company also plans to replace old machinery in Quarter 2 of 2017 by buying new machinery for $131,187 j) The prior year ending balance in accounts recievable was $28,800, of which 84% was incurred in the fourth quarter of 2016 and 16% was incurred in the third quarter of 2016. The company collects 27% of each quarter's sales in the quarter when they occur. Another 51.1% of each quarters sales are collected one quarter after they occur. The remaining 21.9% of each quarter's sales are collected two quarters after they k) All direct material purchases are made on account. All direct labor costs, overhead costs involving cash, and period costs are paid in the quarter incurred. The prior year ending balance in accounts payable was S10,500. The company pays for 47% of each quarters purchases in the quarter when they occur. The remaining 53% of each quarter's purchases are paid for one quarter after they occur. The factory overhead includes depreciation on factory equipment. The facto equipment has a book value of S94,000, no salvage value, and a useful life of 5 years. The company computes depreciation using the straight line method. m) The company has an income tax rate of 36%. Income taxes are incurred at year-end and paid in the following period. Last year, the company's net income before taxes was S171,354. Each year's income taxes are paid in the first quarter of the following year n) On December 31, 2016, the company had an ending cash balance of $12,900 and no bank loans. The company wants to have a minimum cash balance of S9,000 at the end of each quarter. If necessary, the company will borrow money from the bank in $1,000 increments. The bank charges a quarterly interest rate of 8%. The company only borrows money at the start of the quarter. The company will only principal at the end of a quarter. o) The product cost per unit this year is the same as it was last year p) On December 31, 2016, the company had S266,193 ofiand, S868,235 of Building and Equipment, S799,462 of Accumulated Depreciation, and $753,604 ofCommon Stock