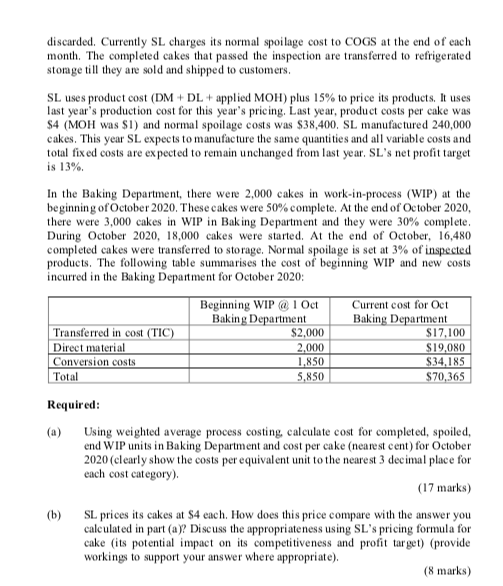

Sarah Lee ("SL") manufactures cakes. Its main product is a frozen butter cake. SL uses normal costing and weighted average process costing. It closes MOH variance to Cost of Goods Sold (COGS) at the end of the year. Last year's MOH variance was $2,400. Frozen butter cakes are produced in a 2-step process in 2 departments: Mixing and Baking Departments. Cake ingredients are mixed in the Mixing Department and kept in chillers until they are transferred to the Baking Department. In the Baking Department, all other ingredients are added at the start of the manufacturing process. Conversion costs are incurred evenly throughout the manufacturing process. Inspection takes place when the production is 100% completed in the Baking Department. All spoiled products are discarded. Currently SL charges its normal spoilage cost to COGS at the end of each month. The completed cakes that passed the inspection are transferred to refrigerated storage till they are sold and shipped to customers. SL uses product cost (DM + DL + applied MOH) plus 15% to price its products. It uses last year's production cost for this year's pricing. Last year, product costs per cake was $4 (MOH was $1) and normal spoilage costs was $38,400 SL manufactured 240,000 cakes. This year SL expects to manufacture the same quantities and all variable costs and total fixed costs are expected to remain unchanged from last year. SL's net profit target is 13%. In the Baking Department, there were 2,000 cakes in work-in-process (WIP) at the beginning of October 2020. These cakes were 50% complete. At the end of October 2020, there were 3,000 cakes in WIP in Baking Department and they were 30% complete. During October 2020, 18,000 cakes were started. At the end of October, 16,480 completed cakes were transferred to storage. Normal spoilage is set at 3% of inspected products. The following table summarises the cost of beginning WIP and new costs incurred in the Baking Department for October 2020: Beginning WIP @ 1 Oct Current cost for Oct Baking Department Baking Department Transferred in cost (TIC) $2,000 $17,100 Direct material 2.000 $19,080 Conversion costs 1.850 $34,185 Total 5,850 $70,365 Required: (a) Using weighted average process costing, calculate cost for completed, spoiled, end WIP units in Baking Department and cost per cake (nearest cent) for October 2020 (clearly show the costs per equivalent unit to the nearest 3 decimal place for each cost category). (17 marks) (b) SL prices its cakes at $4 each. How does this price compare with the answer you calculated in part (a)? Discuss the appropriateness using SL's pricing formula for cake (its potential impact on its competitiveness and profit target) (provide workings to support your answer where appropriate). (8 marks) Sarah Lee ("SL") manufactures cakes. Its main product is a frozen butter cake. SL uses normal costing and weighted average process costing. It closes MOH variance to Cost of Goods Sold (COGS) at the end of the year. Last year's MOH variance was $2,400. Frozen butter cakes are produced in a 2-step process in 2 departments: Mixing and Baking Departments. Cake ingredients are mixed in the Mixing Department and kept in chillers until they are transferred to the Baking Department. In the Baking Department, all other ingredients are added at the start of the manufacturing process. Conversion costs are incurred evenly throughout the manufacturing process. Inspection takes place when the production is 100% completed in the Baking Department. All spoiled products are discarded. Currently SL charges its normal spoilage cost to COGS at the end of each month. The completed cakes that passed the inspection are transferred to refrigerated storage till they are sold and shipped to customers. SL uses product cost (DM + DL + applied MOH) plus 15% to price its products. It uses last year's production cost for this year's pricing. Last year, product costs per cake was $4 (MOH was $1) and normal spoilage costs was $38,400 SL manufactured 240,000 cakes. This year SL expects to manufacture the same quantities and all variable costs and total fixed costs are expected to remain unchanged from last year. SL's net profit target is 13%. In the Baking Department, there were 2,000 cakes in work-in-process (WIP) at the beginning of October 2020. These cakes were 50% complete. At the end of October 2020, there were 3,000 cakes in WIP in Baking Department and they were 30% complete. During October 2020, 18,000 cakes were started. At the end of October, 16,480 completed cakes were transferred to storage. Normal spoilage is set at 3% of inspected products. The following table summarises the cost of beginning WIP and new costs incurred in the Baking Department for October 2020: Beginning WIP @ 1 Oct Current cost for Oct Baking Department Baking Department Transferred in cost (TIC) $2,000 $17,100 Direct material 2.000 $19,080 Conversion costs 1.850 $34,185 Total 5,850 $70,365 Required: (a) Using weighted average process costing, calculate cost for completed, spoiled, end WIP units in Baking Department and cost per cake (nearest cent) for October 2020 (clearly show the costs per equivalent unit to the nearest 3 decimal place for each cost category). (17 marks) (b) SL prices its cakes at $4 each. How does this price compare with the answer you calculated in part (a)? Discuss the appropriateness using SL's pricing formula for cake (its potential impact on its competitiveness and profit target) (provide workings to support your answer where appropriate). (8 marks)