Answered step by step

Verified Expert Solution

Question

1 Approved Answer

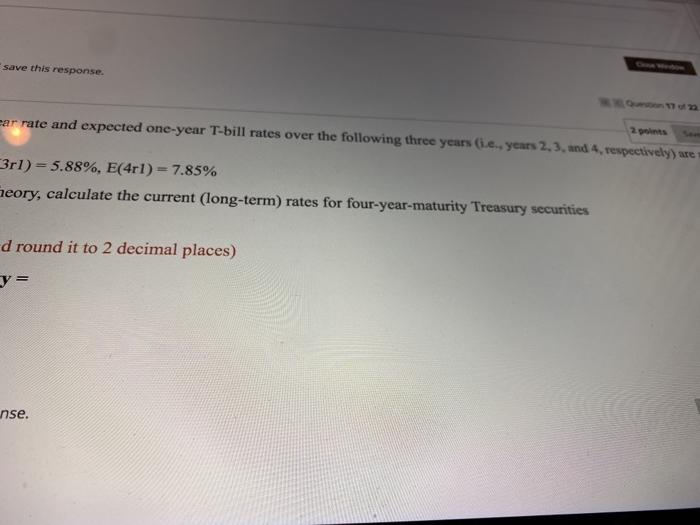

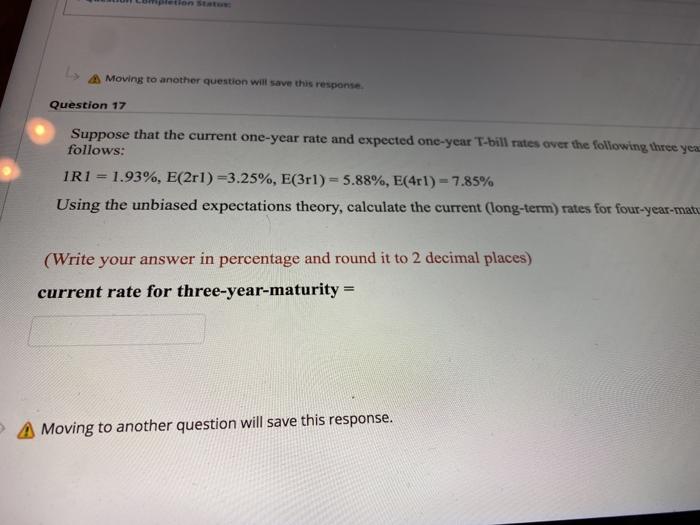

save this response. ear rate and expected one-year T-bill rates over the following three years (ie.. years 2, 3, and 4, respectively) we 3rl) =

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Credit Rating Agencies On The Watch List Analysis Of European Regulation

Authors: Raquel García Alcubilla , Javier Ruiz Del Pozo

1st Edition

0199608865,0191640999