Answered step by step

Verified Expert Solution

Question

1 Approved Answer

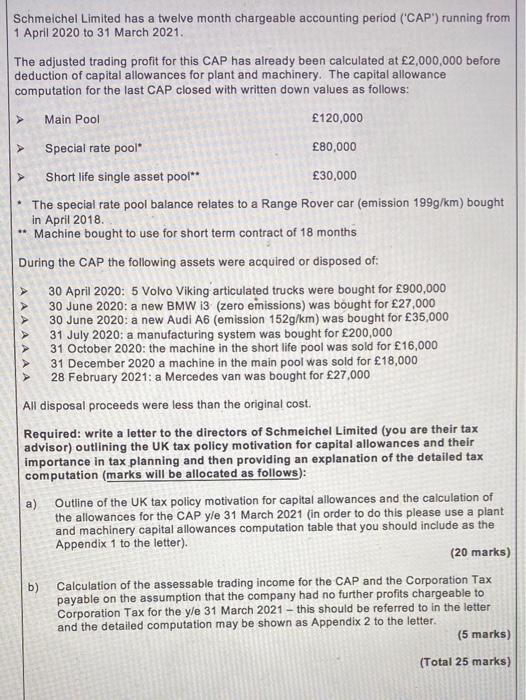

Schmeichel Limited has a twelve month chargeable accounting period ('CAP') running from 1 April 2020 to 31 March 2021. The adjusted trading profit for

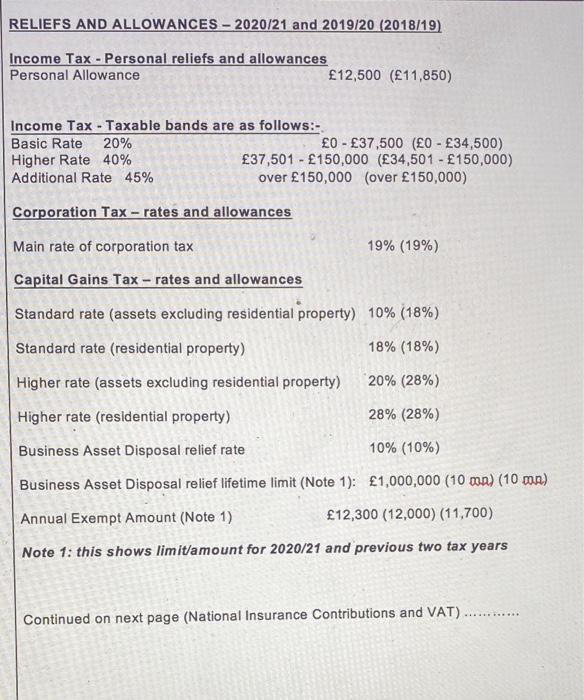

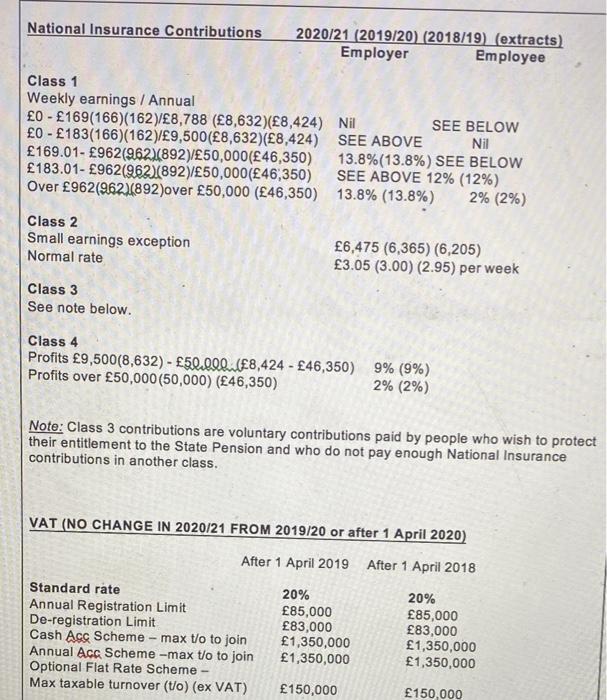

Schmeichel Limited has a twelve month chargeable accounting period ('CAP') running from 1 April 2020 to 31 March 2021. The adjusted trading profit for this CAP has already been calculated at 2,000,000 before deduction of capital allowances for plant and machinery. The capital allowance computation for the last CAP closed with written down values as follows: Main Pool 120,000 Special rate pool* 80,000 Short life single asset pool** 30,000 * The special rate pool balance relates to a Range Rover car (emission 199g/km) bought in April 2018. ** Machine bought to use for short term contract of 18 months During the CAP the following assets were acquired or disposed of: 30 April 2020: 5 Volvo Viking articulated trucks were bought for 900,000 30 June 2020: a new BMW 13 (zero emissions) was bought for 27,000 30 June 2020: a new Audi A6 (emission 152g/km) was bought for 35,000 31 July 2020: a manufacturing system was bought for 200,000 31 October 2020: the machine in the short life pool was sold for 16,000 31 December 2020 a machine in the main pool was sold for 18,000 28 February 2021: a Mercedes van was bought for 27,000 All disposal proceeds were less than the original cost. Required: write a letter to the directors of Schmeichel Limited (you are their tax advisor) outlining the UK tax policy motivation for capital allowances and their importance in tax planning and then providing an explanation of the detailed tax computation (marks will be allocated as follows): Outline of the UK tax policy motivation for capital allowances and the calculation of a) the allowances for the CAP y/e 31 March 2021 (in order to do this please use a plant and machinery capital allowances computation table that you should include as the Appendix 1 to the letter). (20 marks) Calculation of the assessable trading income for the CAP and the Corporation Tax b) payable on the assumption that the company had no further profits chargeable to Corporation Tax for the yle 31 March 2021 - this should be referred to in the letter and the detailed computation may be shown as Appendix 2 to the letter. (5 marks) (Total 25 marks) RELIEFS AND ALLOWANCES - 2020/21 and 2019/20 (2018/19) Income Tax - Personal reliefs and allowances Personal Allowance 12,500 (11,850) Income Tax - Taxable bands are as follows:- Basic Rate 20% Higher Rate 40% Additional Rate 45% 0 - 37,500 (O - 34,500) 37,501 - 150,000 (34,501 - 150,000) over 150,000 (over 150,000) Corporation Tax - rates and allowances Main rate of corporation tax 19% (19%) Capital Gains Tax - rates and allowances Standard rate (assets excluding residential property) 10% (18%) Standard rate (residential property) 18% (18%) Higher rate (assets excluding residential property) 20% (28%) Higher rate (residential property) 28% (28%) Business Asset Disposal relief rate 10% (10%) Business Asset Disposal relief lifetime limit (Note 1): 1,000,000 (10 mn) (10 mn) Annual Exempt Amount (Note 1) 12,300 (12,000) (11,700) Note 1: this shows limit/amount for 2020/21 and previous two tax years Continued on next page (National Insurance Contributions and VAT) National Insurance Contributions 2020/21 (2019/20) (2018/19) (extracts) Employer Employee Class 1 Weekly earnings / Annual 0 - 169(166)(162)/8,788 (8,632)(8,424) Nil 0 - 183(166)(162)/9,500(8,632)(8,424) SEE ABOVE 169.01- 962(962)(892)/50,000(46,350) 183.01- 962(962)(892)/50,000(46,350) Over 962(962)(892)over 50,000 (46,350) 13.8% (13.8%) SEE BELOW Nil 13.8%(13.8%) SEE BELOW SEE ABOVE 12% (12%) 2% (2%) Class 2 Small earnings exception 6,475 (6,365) (6,205) 3.05 (3.00) (2.95) per week Normal rate Class 3 See note below. Class 4 Profits 9,500(8,632) - 50.000 (8,424 - 46,350) 9% (9%) Profits over 50,000 (50,000) (46,350) 2% (2%) Note: Class 3 contributions are voluntary contributions paid by people who wish to protect their entitlement to the State Pension and who do not pay enough National Insurance contributions in another class. VAT (NO CHANGE IN 2020/21 FROM 2019/20 or after 1 April 2020) After 1 April 2019 After 1 April 2018 Standard rate 20% 20% Annual Registration Limit De-registration Limit Cash Acc Scheme - max t/o to join Annual Ac Scheme -max t/o to join Optional Flat Rate Scheme Max taxable turnover (t/o) (ex VAT) 85,000 83,000 85,000 83,000 1,350,000 1,350,000 1,350,000 1,350,000 150,000 150,000 Schmeichel Limited has a twelve month chargeable accounting period ('CAP') running from 1 April 2020 to 31 March 2021. The adjusted trading profit for this CAP has already been calculated at 2,000,000 before deduction of capital allowances for plant and machinery. The capital allowance computation for the last CAP closed with written down values as follows: Main Pool 120,000 Special rate pool* 80,000 Short life single asset pool** 30,000 * The special rate pool balance relates to a Range Rover car (emission 199g/km) bought in April 2018. ** Machine bought to use for short term contract of 18 months During the CAP the following assets were acquired or disposed of: 30 April 2020: 5 Volvo Viking articulated trucks were bought for 900,000 30 June 2020: a new BMW 13 (zero emissions) was bought for 27,000 30 June 2020: a new Audi A6 (emission 152g/km) was bought for 35,000 31 July 2020: a manufacturing system was bought for 200,000 31 October 2020: the machine in the short life pool was sold for 16,000 31 December 2020 a machine in the main pool was sold for 18,000 28 February 2021: a Mercedes van was bought for 27,000 All disposal proceeds were less than the original cost. Required: write a letter to the directors of Schmeichel Limited (you are their tax advisor) outlining the UK tax policy motivation for capital allowances and their importance in tax planning and then providing an explanation of the detailed tax computation (marks will be allocated as follows): Outline of the UK tax policy motivation for capital allowances and the calculation of a) the allowances for the CAP y/e 31 March 2021 (in order to do this please use a plant and machinery capital allowances computation table that you should include as the Appendix 1 to the letter). (20 marks) Calculation of the assessable trading income for the CAP and the Corporation Tax b) payable on the assumption that the company had no further profits chargeable to Corporation Tax for the yle 31 March 2021 - this should be referred to in the letter and the detailed computation may be shown as Appendix 2 to the letter. (5 marks) (Total 25 marks) RELIEFS AND ALLOWANCES - 2020/21 and 2019/20 (2018/19) Income Tax - Personal reliefs and allowances Personal Allowance 12,500 (11,850) Income Tax - Taxable bands are as follows:- Basic Rate 20% Higher Rate 40% Additional Rate 45% 0 - 37,500 (O - 34,500) 37,501 - 150,000 (34,501 - 150,000) over 150,000 (over 150,000) Corporation Tax - rates and allowances Main rate of corporation tax 19% (19%) Capital Gains Tax - rates and allowances Standard rate (assets excluding residential property) 10% (18%) Standard rate (residential property) 18% (18%) Higher rate (assets excluding residential property) 20% (28%) Higher rate (residential property) 28% (28%) Business Asset Disposal relief rate 10% (10%) Business Asset Disposal relief lifetime limit (Note 1): 1,000,000 (10 mn) (10 mn) Annual Exempt Amount (Note 1) 12,300 (12,000) (11,700) Note 1: this shows limit/amount for 2020/21 and previous two tax years Continued on next page (National Insurance Contributions and VAT) National Insurance Contributions 2020/21 (2019/20) (2018/19) (extracts) Employer Employee Class 1 Weekly earnings / Annual 0 - 169(166)(162)/8,788 (8,632)(8,424) Nil 0 - 183(166)(162)/9,500(8,632)(8,424) SEE ABOVE 169.01- 962(962)(892)/50,000(46,350) 183.01- 962(962)(892)/50,000(46,350) Over 962(962)(892)over 50,000 (46,350) 13.8% (13.8%) SEE BELOW Nil 13.8%(13.8%) SEE BELOW SEE ABOVE 12% (12%) 2% (2%) Class 2 Small earnings exception 6,475 (6,365) (6,205) 3.05 (3.00) (2.95) per week Normal rate Class 3 See note below. Class 4 Profits 9,500(8,632) - 50.000 (8,424 - 46,350) 9% (9%) Profits over 50,000 (50,000) (46,350) 2% (2%) Note: Class 3 contributions are voluntary contributions paid by people who wish to protect their entitlement to the State Pension and who do not pay enough National Insurance contributions in another class. VAT (NO CHANGE IN 2020/21 FROM 2019/20 or after 1 April 2020) After 1 April 2019 After 1 April 2018 Standard rate 20% 20% Annual Registration Limit De-registration Limit Cash Acc Scheme - max t/o to join Annual Ac Scheme -max t/o to join Optional Flat Rate Scheme Max taxable turnover (t/o) (ex VAT) 85,000 83,000 85,000 83,000 1,350,000 1,350,000 1,350,000 1,350,000 150,000 150,000 Schmeichel Limited has a twelve month chargeable accounting period ('CAP') running from 1 April 2020 to 31 March 2021. The adjusted trading profit for this CAP has already been calculated at 2,000,000 before deduction of capital allowances for plant and machinery. The capital allowance computation for the last CAP closed with written down values as follows: Main Pool 120,000 Special rate pool* 80,000 Short life single asset pool** 30,000 * The special rate pool balance relates to a Range Rover car (emission 199g/km) bought in April 2018. ** Machine bought to use for short term contract of 18 months During the CAP the following assets were acquired or disposed of: 30 April 2020: 5 Volvo Viking articulated trucks were bought for 900,000 30 June 2020: a new BMW 13 (zero emissions) was bought for 27,000 30 June 2020: a new Audi A6 (emission 152g/km) was bought for 35,000 31 July 2020: a manufacturing system was bought for 200,000 31 October 2020: the machine in the short life pool was sold for 16,000 31 December 2020 a machine in the main pool was sold for 18,000 28 February 2021: a Mercedes van was bought for 27,000 All disposal proceeds were less than the original cost. Required: write a letter to the directors of Schmeichel Limited (you are their tax advisor) outlining the UK tax policy motivation for capital allowances and their importance in tax planning and then providing an explanation of the detailed tax computation (marks will be allocated as follows): Outline of the UK tax policy motivation for capital allowances and the calculation of a) the allowances for the CAP y/e 31 March 2021 (in order to do this please use a plant and machinery capital allowances computation table that you should include as the Appendix 1 to the letter). (20 marks) Calculation of the assessable trading income for the CAP and the Corporation Tax b) payable on the assumption that the company had no further profits chargeable to Corporation Tax for the yle 31 March 2021 - this should be referred to in the letter and the detailed computation may be shown as Appendix 2 to the letter. (5 marks) (Total 25 marks) RELIEFS AND ALLOWANCES - 2020/21 and 2019/20 (2018/19) Income Tax - Personal reliefs and allowances Personal Allowance 12,500 (11,850) Income Tax - Taxable bands are as follows:- Basic Rate 20% Higher Rate 40% Additional Rate 45% 0 - 37,500 (O - 34,500) 37,501 - 150,000 (34,501 - 150,000) over 150,000 (over 150,000) Corporation Tax - rates and allowances Main rate of corporation tax 19% (19%) Capital Gains Tax - rates and allowances Standard rate (assets excluding residential property) 10% (18%) Standard rate (residential property) 18% (18%) Higher rate (assets excluding residential property) 20% (28%) Higher rate (residential property) 28% (28%) Business Asset Disposal relief rate 10% (10%) Business Asset Disposal relief lifetime limit (Note 1): 1,000,000 (10 mn) (10 mn) Annual Exempt Amount (Note 1) 12,300 (12,000) (11,700) Note 1: this shows limit/amount for 2020/21 and previous two tax years Continued on next page (National Insurance Contributions and VAT) National Insurance Contributions 2020/21 (2019/20) (2018/19) (extracts) Employer Employee Class 1 Weekly earnings / Annual 0 - 169(166)(162)/8,788 (8,632)(8,424) Nil 0 - 183(166)(162)/9,500(8,632)(8,424) SEE ABOVE 169.01- 962(962)(892)/50,000(46,350) 183.01- 962(962)(892)/50,000(46,350) Over 962(962)(892)over 50,000 (46,350) 13.8% (13.8%) SEE BELOW Nil 13.8%(13.8%) SEE BELOW SEE ABOVE 12% (12%) 2% (2%) Class 2 Small earnings exception 6,475 (6,365) (6,205) 3.05 (3.00) (2.95) per week Normal rate Class 3 See note below. Class 4 Profits 9,500(8,632) - 50.000 (8,424 - 46,350) 9% (9%) Profits over 50,000 (50,000) (46,350) 2% (2%) Note: Class 3 contributions are voluntary contributions paid by people who wish to protect their entitlement to the State Pension and who do not pay enough National Insurance contributions in another class. VAT (NO CHANGE IN 2020/21 FROM 2019/20 or after 1 April 2020) After 1 April 2019 After 1 April 2018 Standard rate 20% 20% Annual Registration Limit De-registration Limit Cash Acc Scheme - max t/o to join Annual Ac Scheme -max t/o to join Optional Flat Rate Scheme Max taxable turnover (t/o) (ex VAT) 85,000 83,000 85,000 83,000 1,350,000 1,350,000 1,350,000 1,350,000 150,000 150,000

Step by Step Solution

★★★★★

3.47 Rating (163 Votes )

There are 3 Steps involved in it

Step: 1

Dear Directors I am writing to outline the UK tax policy motivation for capital allowances and the calculation of the allowances for the twelve month ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Introduction To Business Statistics

Authors: Ronald M. Weiers

7th Edition

978-0538452175, 538452196, 053845217X, 2900538452198, 978-1111524081