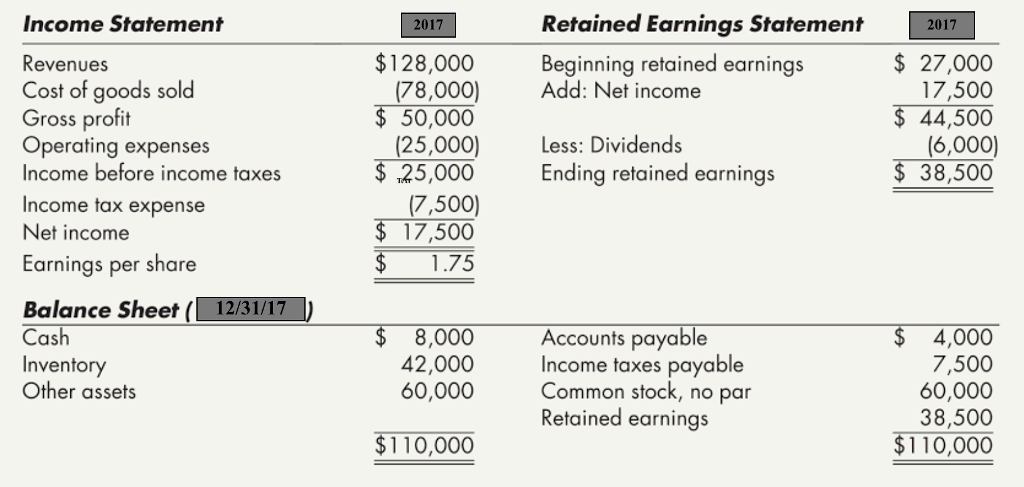

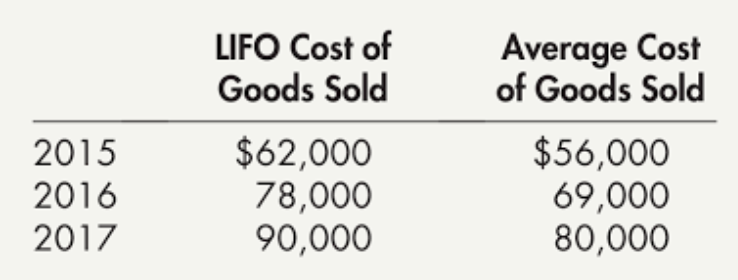

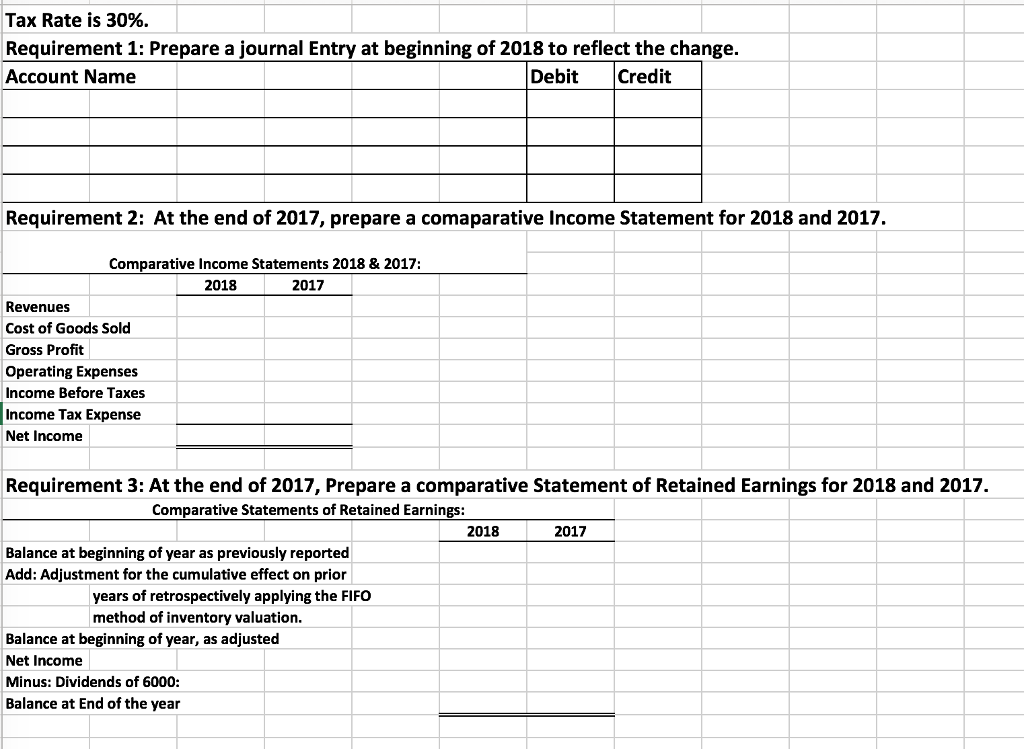

Schmidt Company began operations on January 1, 2017 (or any year before that) and used LIFO inventory method for both Financing reporting and Income tax reporting. However, at beginning of 2018, Schmidt decided to switch to FIFO inventory method for Financial and Income tax reporting. It had previously reported the following financial statements for 2017:

** It Shows Average cost of goods sold but that actually should be FIFO Cost of GOODS SOLD NOT AVERAGE**.

Income Statement 2017 Retained Earnings Statement 2017 $128,000 $ 27,000 17,500 44,500 (6,000) 38,500 Beginning retained earnings Add: Net income Revenues Cost of goods sold Gross profit Operating expenses Income before income taxes Income fax expense Net income Earnings per share 50,000 (25,000) : Dividends Ending retained earnings 25,000 (7,500) 17,500 1.75 Balance Sheet 12/31/17 8,000 42,000 60,000 Accounts payable Income taxes payable Common stock, no par Retained earnings 4,000 7,500 60,000 38,500 $110,000 as Inventory Other assets 110,000 LIFO Cost of Goods Sold Average Cost of Goods Sold 2015 2016 2017 $62,000 78,000 90,000 $56,000 69,000 80,000 Tax Rate is 30%. Requirement 1: Prepare a journal Entry at beginning of 2018 to reflect the change. Account Name Debit Credit Requirement 2: At the end of 2017, prepare a comaparative Income Statement for 2018 and 2017. Comparative Income Statements 2018 & 2017: 2018 2017 Revenues Cost of Goods Sold Gross Profit Operating Expenses Income Before Taxes Income Tax Expense Net Income Requirement 3: At the end of 2017, Prepare a comparative Statement of Retained Earnings for 2018 and 2017. Comparative Statements of Retained Earnings: 2018 2017 Balance at beginning of year as previously reported Add: Adjustment for the cumulative effect on prior years of retrospectively applying the FIFO method of inventory valuation. Balance at beginning of year, as adjusted Net Income Minus: Dividends of 6000: Balance at End of the year Income Statement 2017 Retained Earnings Statement 2017 $128,000 $ 27,000 17,500 44,500 (6,000) 38,500 Beginning retained earnings Add: Net income Revenues Cost of goods sold Gross profit Operating expenses Income before income taxes Income fax expense Net income Earnings per share 50,000 (25,000) : Dividends Ending retained earnings 25,000 (7,500) 17,500 1.75 Balance Sheet 12/31/17 8,000 42,000 60,000 Accounts payable Income taxes payable Common stock, no par Retained earnings 4,000 7,500 60,000 38,500 $110,000 as Inventory Other assets 110,000 LIFO Cost of Goods Sold Average Cost of Goods Sold 2015 2016 2017 $62,000 78,000 90,000 $56,000 69,000 80,000 Tax Rate is 30%. Requirement 1: Prepare a journal Entry at beginning of 2018 to reflect the change. Account Name Debit Credit Requirement 2: At the end of 2017, prepare a comaparative Income Statement for 2018 and 2017. Comparative Income Statements 2018 & 2017: 2018 2017 Revenues Cost of Goods Sold Gross Profit Operating Expenses Income Before Taxes Income Tax Expense Net Income Requirement 3: At the end of 2017, Prepare a comparative Statement of Retained Earnings for 2018 and 2017. Comparative Statements of Retained Earnings: 2018 2017 Balance at beginning of year as previously reported Add: Adjustment for the cumulative effect on prior years of retrospectively applying the FIFO method of inventory valuation. Balance at beginning of year, as adjusted Net Income Minus: Dividends of 6000: Balance at End of the year