Answered step by step

Verified Expert Solution

Question

1 Approved Answer

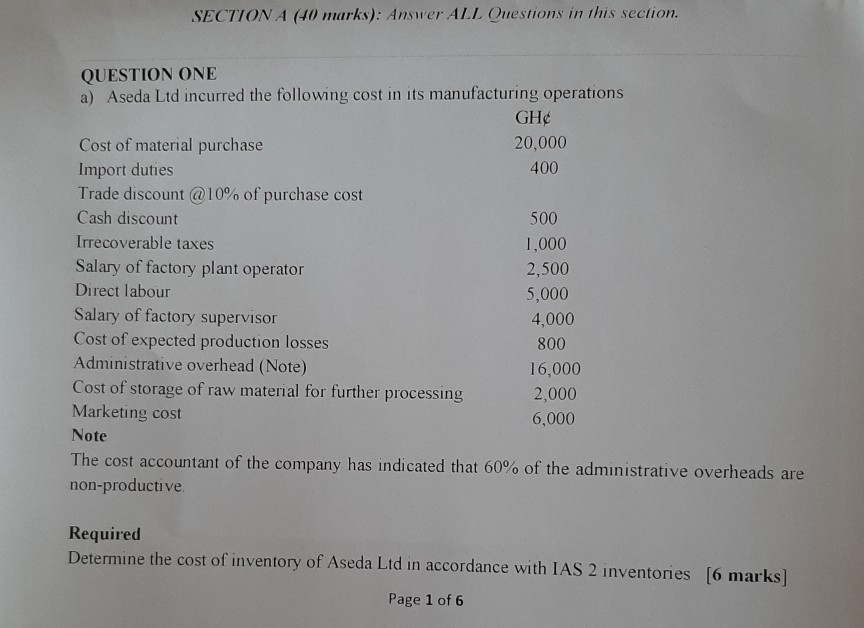

SECTION A (40 marks): Answer ALL Questions in this section. QUESTION ONE a) Aseda Ltd incurred the following cost in its manufacturing operations GH Cost

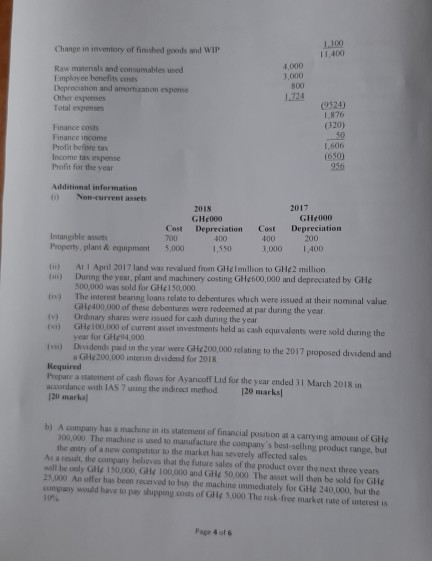

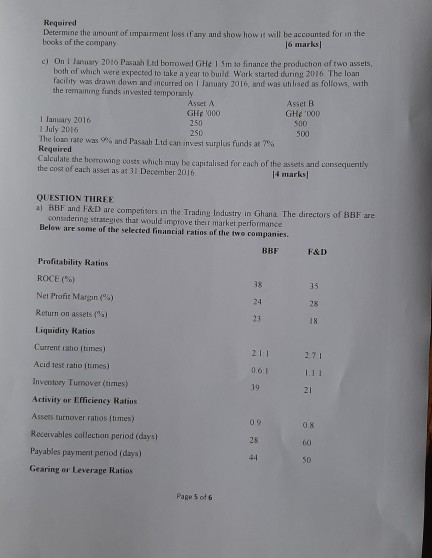

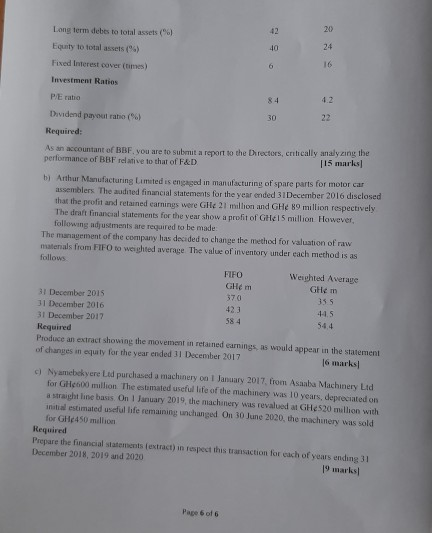

SECTION A (40 marks): Answer ALL Questions in this section. QUESTION ONE a) Aseda Ltd incurred the following cost in its manufacturing operations GH Cost of material purchase 20,000 Import duties 400 Trade discount @10% of purchase cost Cash discount 500 Irrecoverable taxes 1,000 Salary of factory plant operator 2,500 Direct labour 5,000 Salary of factory supervisor 4,000 Cost of expected production losses 800 Administrative overhead (Note) 16,000 Cost of storage of raw material for further processing 2,000 Marketing cost 6,000 Note The cost accountant of the company has indicated that 60% of the administrative overheads are non-productive Required Determine the cost of inventory of Aseda Ltd in accordance with IAS 2 inventories [6 marks] Page 1 of 6 b) Outlme five (5) purposes the IAS's conceptual framework of accounting seeks to achieve [5 marks c) Asanba Ltd receives a 20% grant towards the cost of a new item of machinery, which cost GHE 100.000 The machinery has an expected life of four years and a nil residual value The expected profits of the company, before accounting for depreciation on the new machine or the grant amount to GHE 50.000 per annum in each year of the machinery's life Required Show how Asaba Led should account for this grant in the financial statements over the life of the machinery in accordance with IAS 20 using the Netting of method Deferred Income method (12 marks 1 d) An entity is about to begin to operate a coal mine. At the end of the reporting period, the mineshaft has been prepared and all the necessary equipment has been constructed and is in place, but no coal has yet been extracted Linder local law, the entity is obliged to rectify all damage to the site once the mining operation has been completed (this is expected to be several years from now) Management estimates that 20% of the eventual costs of performing this work will relate to removing the equipment and vanius buildings and the remaining 80% will relate to restoring the damage caused by the actual extraction of coal Required Should a provision be recognised for the cost of restoring the damage" [5 marks e) On January 1, 2017 Bambo Ltd purchased a building for its investment potential. The building cost Gel million with transaction costs of GHE 10,000. Its depreciable amount at this date was GH 300.000 The property has a useful life of 50 years. At 11 December 2018 the property's fair value had risen to GH 13 million During the year 2018 the property was sold for GH 1,550,000, and that selling costs were GHE 50.000 i Required What amounts would be included in the statement of comprehensive income for 2018 in respect of this disposal under the cost model and the fair value model [6 marks) 1) Illustrate the effects of the events after the reporting period described below on the recognition and measurement in the financial statements if Arthur Lid's financial year ends 31 December 2018 1 Arthur Lid was sued on December 31, 2018 it is not clear whether the probability of conviction in the ongoing trial is more than 50% Shortly after December 31 2018 the entity is convicted Page 2 of 6 In January 2019. part of the manufacturing facilities and inventories of an Arthur Ledis destroyed by a flood The damages are not covered by insurance However, the entity's management expects that it will be possible to continue the business activities [6 marks SECTION 1 (wirksamer ALL. Owestions in this section. QUESTION TWO a) The statement of financial position and statement of profit or loss for Avaricoff Ltd for the year to 31 March 2018 are provided below Statement of financial position as al 31st March 2018 2017 GH000 GH_000 Non-current assets Intangible assets 300 200 Property, plant and equipment 3,450 1,600 Financial assets 400 200 4.50 2.000 Current assets Inventory 3,200 2.000 Trade receivables 2.400 2,0x30 Cash and cash equivalents 32 S80 5,612 4580 9.282 6.680 Equity Issued share capital 3.000 2.000 Share premium account 838 560 Retained earnings 910 354 Revaluation surplus 5,748 2914 Non-current liabilities Interest-bearing loans and liabilities 1,600 2.000 Current liabilities Bank overdraft Trade payables 1.600 1.266 Taxation 420 400 2.434 1.666 Total equity and liabilities 9.782 6,580 Statement of profit or loss for the year ended 31st March 2018 GHEXIO Revenue Other income GH000 10,000 100 Page 3 of 6 Change in inventory of fished goods and WIP 1.100 11.400 Raw materials and consumables used Employee benefits costs Deprecation and amortization expense Other expenses Total expenses 4 000 1.000 800 1.724 Finance costs Finance income Profit before tax Income tax expense Profit for the year 1876 (120) 50 1.606 (650) 956 200 Additional information Non-current assets 2018 2017 GH000 GHO Cast Depreciation Cost Depreciation Intangible assets 700 400 100 Property, plant & equipment 5.000 1.550 3,000 1,400 At 1 April 2017 land was revalued from GHeimillion to GH2 million During the year, plant and machinery costing GH600,000 and depreciated by GH 500,000 was sold for GH 150,000, The interest bearing loans relate to debentures which were issued at their nominal value GH400,000 of these debentures were redeemed at par during the year Ordinary shares were issued for cash during the year GH100,000 of current asset investments held as cash equivalents were sold during the year for GH 1.000 Dividends paid in the year were GH 200,000 relating to the 2017 proposed dividend and GH200,000 interim dividend for 2018 Required Prepare a statement of cash flows for Ayancol Lid for the year ended 31 March 2018 in accordance with LAS 7 using the indirect method 120 marks 20 markal b) A company has a machine in its statement of financial position at a carrying amount of GH 300.000 The machine is used to manufacture the company's best-selling product range, but the entry of a new competitor to the market has severely affected sales As a result, the company believes that the future sales of the product over the next three years will be only GH 150,000 GR 100.000 and Gl 50.000 The asset will then be sold for GH 25.000 An offer has been received to buy the machine immediately for GH 240,000, but the company would have to pay shipping costs of GH5.000 Thenisk-free market rate of interestis 10 Page 4 of 6 Required Determine the amount of impairment loss if any and show how it will be accounted for in the books of the company 16 marks c) On 1 January 2016 Pasnah Led borrowed GHE 1.5m to finance the production of two assets, both of which were expected to take a year to build Wark started during 2016 The loan facility was drawn down and incurred on January 2016, and was utilised as follows, with the remaining funds invested temporary Asset A Asier B GH 1000 GHOOD 1 January 2016 250 SOO 1 July 2016 250 500 The loan rate was and Pasal Ltd can invest surplus funds at 7% Required Calculate the borrowing costs which may be capitalised for each of the assets and consequently the cost of each asset as at 31 December 2016 14 marks QUESTION THREE al BBF and F&D are competitors in the Trading Industry in Ghana The directors of BBF are considering strategies that would improve their market performance Below are some of the selected financial ratios of the two companies BBF F&D Profitability Ratios ROCE(56) 38 35 Net Profit Margin() 24 28 Return on assets (9) 23 18 Liquidity Ratios Current ratio (times) 21:1 2.7.1 06:1 19 21 Acid test ratio times) Inventory Tumover (times) Activity or Efficiency Ratios Assets turnover ratios lumes) Receivables collection period (days) Payables payment period (days) Gearing or Leverage Ratios 09 08 28 00 44 SO Page 5 of 6 0 20 Long term debes to total assets (9) 40 24 Equity to total assets(") Fixed Interest cover (times) 16 Investment Ratios PE ratio 84 Dividend payout rabo (*) 30 22 Required: As an accountant of BBF, you are to submit a report to the Directors, critically analyzing the performance of BBF relative to that of F&D 115 marles b) Arthur Manufacturing Limited is engaged in manufacturing of spare parts for motor car assemblers. The audited financial statements for the year ended 31 December 2016 disclosed that the profit and retained earnings were GH 21 million and GHe 89 million respectively The draft financial statements for the year show a profit of GH15 million However, following adjustments are required to be made The management of the company has decided to change the method for valuation of raw materials from FIFO to weighted average The value of inventory under each method is as follows FIFO Weighted Average Ghem GHm 31 December 2015 370 355 31 December 2016 423 445 31 December 2017 584 544 Required Produce an extract showing the movement in retained earnings as would appear in the statement of changes in equity for the year ended 31 December 2017 16 marks! c) Nyamebekyere Ltd purchased a machinery on January 2017, from Asaba Machinery Ltd for GH600 million The estimated useful life of the machinery was 10 years, deprecated on a straight line basis on 1 January 2019, the machinery was revalued at GH4520 million with initial estimated useful life remaining unchanged On 30 June 2020, the machinery was sold for GH 450 million Required Prepare the financial statements extract) in respect this transaction for each of years ending 31 December 2018, 2019 and 2020 19 marks Page 6 of 6

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Practitioners Guide To Edp Auditing

Authors: Jack Mullen

1st Edition

0136912621, 978-0136912620