Question

SECTION A [40 MARKS] Study the article below and based on the requirement for the proposed study, answer the questions in this section. Managerial ability

SECTION A [40 MARKS]

Study the article below and based on the requirement for the proposed study, answer the questions in this section.

Managerial ability and Organisational performance

Recent research shows that differences in performance between firms are substantial, persistent over time and largely unexplained (Syverson, 2011). As a potential explanation, a growing body of work highlights the quality of top executives in shaping firm outcomes (Bertrand and Schoar, 2003? Bender, Bloom and Card, et al., 2018? Sauvagnat and Schivardi, 2023). However, we still have a poor understanding of the factors that determine the differences in managerial quality across firms. In particular, what are the frictions that account for the fact that some firms allocate control to inferior managerial talent, hurting firm performance and, through this, aggregate productivity?

Quantifying managerial talent is central to many important research questions, such as those examining managerial contributions to firm performance and investment decisions, R&D investment decisions, merger and acquisition activities, executive compensation, and corporate governance. Prior research indicates that manager-specific features (ability, talent, reputation, or style) affect economic outcomes and are therefore important to economics, finance, accounting, and management research as well as to practice (Bertrand and Schoar, 2003).

Bender et al. (2018) used matched employer-employee data to show that firm performance is disproportionately dependent on the human capital of the executives, rather than of the average worker. Several studies rely on the occurrence of exogenous events such as CEO deaths or hospitalisations to shed light on the importance of executives for firm outcomes (Jenter et al., 2018? Choi et al., 2019? Smith et al., 2019? Bennedsen et al., 2020? Becker and Hvide, 2021? Huber et al., 2021).

Managerial ability

In their seminal work, Upper Echelons: The Organization as a Reflection of Its Top Managers, Hambrick and Mason (1984) theorised that managerial characteristics are partial predictors of organisational outcomes such as strategic decisions or choices and performance levels. The extant literature on upper echelons theory firmly suggests that managerial behavioural factors are influential in complex decisions in a corporate context and that, in general, strategic decisions and organisational outcomes are predicted, to some degree, by CEO managerial characteristics.

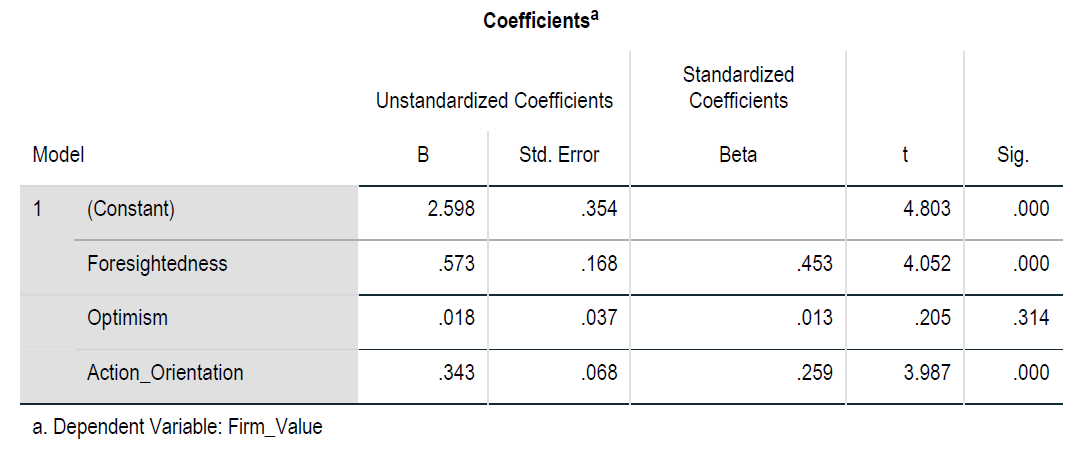

Subsequent studies, such as Chemmanur et al. (2001) and Chemmanur and Paeglis (2005), which use composite measures for managerial quality including management team size, knowledge and education, tenure, CEO dominance, and reputation have demonstrated the potential of managerial ability in predicting organisational outcomes. Furthermore, Demerjian, Lev, and McVay (2012) found that revenue generation is an outcome of CEOs' managerial efficiency, a variant of the managerial ability measure. Crucially, the CEO managerial efficiency measure advanced by Demerjian et al. (2012) is reported to contain less noise, captures better the manager-specific component of ability, and meaningfully reflects managerial efficiency and productivity as a product of CEOs' past and unobservable experiences, psychological traits, values, etc. In this sense, the efficiency measure is a summary proxy for CEO managerial ability. In addition, Demerjian et al. (2012) showed that the managerial efficiency measure outperforms existing ability measures, including past abnormal performance, CEO tenure, and media mentions.

Similarly, Demerjian, Lev, Lewis, and McVay (2013) examined the relation between managerial ability and earnings quality and found that earnings quality is positively associated with managerial ability. Specifically, more able managers are associated with fewer subsequent restatements, higher earnings and accruals persistence, lower errors in bad debt provisions, and higher quality accrual estimations. The results are consistent with the premise that managers can and do impact the quality of the judgments and estimates used to form earnings.

In a recent study, Gan (2019) investigated how higher ability CEOs behave differently from lower ability CEOs in making investment decisions and, particularly, whether CEO managerial ability contributes to improved investment efficiency. He reported that, firstly higher CEO managerial ability leads to more efficient investment decision-making and secondly that high managerial ability helps with overcoming the two sources of investment inefficiency: over- and under-investment. Specifically, talented CEOs increase (decrease) capital expenditures, acquisition expenditures, and total investments when their firms operate in settings more prone to under-investment (over-investment). The findings suggested that the positive impact of CEO managerial ability on investment efficiency generally persists across different levels of board monitoring, whereas it gets weaker as the CEOs are overly exposed to equity risk. Robustness tests of using alternative measures of CEO managerial ability and controlling for potential endogeneity issues generated consistent results.

More recently, using the sample of 246 firms listed at Pakistan Stock Exchange during 2009 to 2017, Bhutta, Sheikh, Munir, Naz, and Saif (2021) empirically examined the impact of managerial ability on firm performance and reported that more able managers significantly increase firm performance while less able managers significantly reduce the firm performance. These findings hold for both accounting and market measures of firm performance as well as alternative measures of managerial ability. Bhutta et al. (2021) concluded that able managers enhance firm value and that the effects of managerial ability are stronger in financially constrained firms.

Organisational performance

Organisation-level analysis involves looking at both the external variables and internal strategies and structures that impact organisational performance. Enhancing the performance of firms in their external environment is a key factor in the definition of the strategic management field, but the link between strategic management and organisational performance, however, remains somewhat murky (Nag et al., 2017).

According to Elena-Juliana and Maria (2016), organisational performance is often confounded with notions such as: productivity, efficiency, effectiveness, economy, earning capacity, profitability, competitiveness, etc. A systematic literature review of 213 studies published in reputed journals for a period of only three years (2006-2009) revealed 207 different measures used for assessing performance (Richard et al., 2009).

Organisational design and form are still often taken to be the 'structure' of an organisation. To improve organisational performance, there is a tendency to 'reorganize' or 'restructure' the reporting relationships between internal functional departments and the associated coordination and linking mechanisms that facilitate the flow of information/resources between and among the business units. This view that 'structure' was synonymous with 'design' and that a 'right' structure could be developed for an organization may be traced to organisation theories prevalent in the late 1970s and based in mechanistic systems theory. According to Richard, Devinney and Yip (2009), organizational performance encompasses three specific areas of firm outcomes: (1) financial performance (profits, return on assets, return on investment, etc.)? (2) product market performance (sales, market share, etc.)? and (3) shareholder return (total shareholder return, economic value added, etc.).

Researchers address the nature of these specific measures by examining the objective measures of performance?accounting and financial market measures, plus firm survival?followed by subjective and quasi subjective measures?such as survey-based self-reports and Likert responses. These measures target the financial, product market, and shareholder outcomes that constitute performance.

Source: Synthesized from multiple sources.

Requirements for the proposed study

With the rapidly changing post-Covid economic environment, changing customer and investor demands, and ever-increasing product-market competition, the quality of top executives in shaping firm outcomes has once again attracted the attention of researchers.

You are an organisational researcher with a keen interest in upper echelons theory and firm performance across regional markets on the African continent. Currently, you are proposing a study aimed at investigating the role of managerial ability of top management teams in the performance of JSE-listed companies.

Your study proposes the use of both accounting and market measures of firm performance as well as Demerjian et al. (2012? 2013) model of managerial efficiency. In addition, post-survey interviews will be conducted with five organisational experts who possess relevant experience in organisational performance and managerial ability.

Your study will use a quantitative approach to answer the following research questions:

- How does top management teams' managerial ability contribute to the performance of JSE-listed firms?

- Is there an optimal way to (re)structure top management teams for sustained superior performance of JSE-listed firms?

- What recommendations can be made to the top management teams of JSE-listed firms on how to leverage managerial ability for superior organisational performance?

QUESTION 1 (30Marks)

Please outline how you would go about conducting the proposed study with reference to the following:

1.1 Formulate a suitable title for the proposed study. (3 marks)

1.2. Formulate THREE (3) research objectives that your study will seek to achieve. (3 marks)

1.3 With regard to your proposed research design:

1.3.1 Critically discuss the essential ontological and epistemological elements of the research philosophy that would underpin the proposed study. (3 marks)

1.3.2 Using your understanding of research design, specify and discuss the research design that you would employ for your study and rationalise the choice of this particular design. (3 marks)

1.4 Based on the research design that you have proposed, discuss the methodology you would follow with regard to the following:

1.4.1 Sampling Methodology for the proposed study:

1.4.1.1 Identify the target population for the proposed study and discuss whether your sampling approach would be probability or non-probability. (3 marks)

1.4.1.2 Propose a method(s) of sampling for the study and justify the propriety of the proposed method of sampling for the study. (4 marks)

1.4.2 Method of Data Collection for the proposed study:

1.4.2.1 Propose with meaningful discussion an appropriate method of data collection for your study, highlighting all the considerations for data collection and the data collection instrument(s)? (5 marks)

1.4.3 Method of Data Analysis for the proposed study:

1.4.3.1 Briefly discuss the method(s) of data analysis that you would use in your study (note: you are required to specify and discuss the methods of analysis you would employ for each of your research questions in 1.2). (6 marks)

QUESTION 2 (10 Marks)

An essential part of the requirements for the proposed study is "post-survey interviews will be conducted with five organisational experts who possess the relevant experience in organisational performance and managerial ability".

Based on your understanding of Braun and Clarke's (2006) framework of thematic analysis, discuss the six phases of thematic analysis that you could follow to systematize and increase the traceability and verification of the analysis of the data that would be collected from the post-survey interviews.

SECTION B

QUESTION 3 (20 Marks)

Read the case below and answer the questions that follow.

In pursuit of sustainable corporate profitability (SCP), internationally leading companies, including Amazon and Apple are redefining the purpose of a corporation from that of profit maximisation to a commitment to environmental, social and governance sustainability (The Guardian, 2019). The former is consistent with the shareholder primacy model (SPM), and the latter, the stakeholder theory.

The shareholder primacy model (SPM) advocates for corporate managers and company directors to make business decisions in the primary interest of shareholders (Smith and Ronnegard, 2016:463? Hung, 2020:5). Conversely, according to the stakeholder theory, the purpose of the corporation is to act as a vehicle for furthering the interests of stakeholders rather than merely maximising shareholders' financial returns (Smith and Ronnegard, 2016: 474). According to Yosifon (2017:464), corporates following SPM deliver products or services to make money? while those complying with stakeholder theory, to some extent, make money to provide better, corporate, social or community, services.

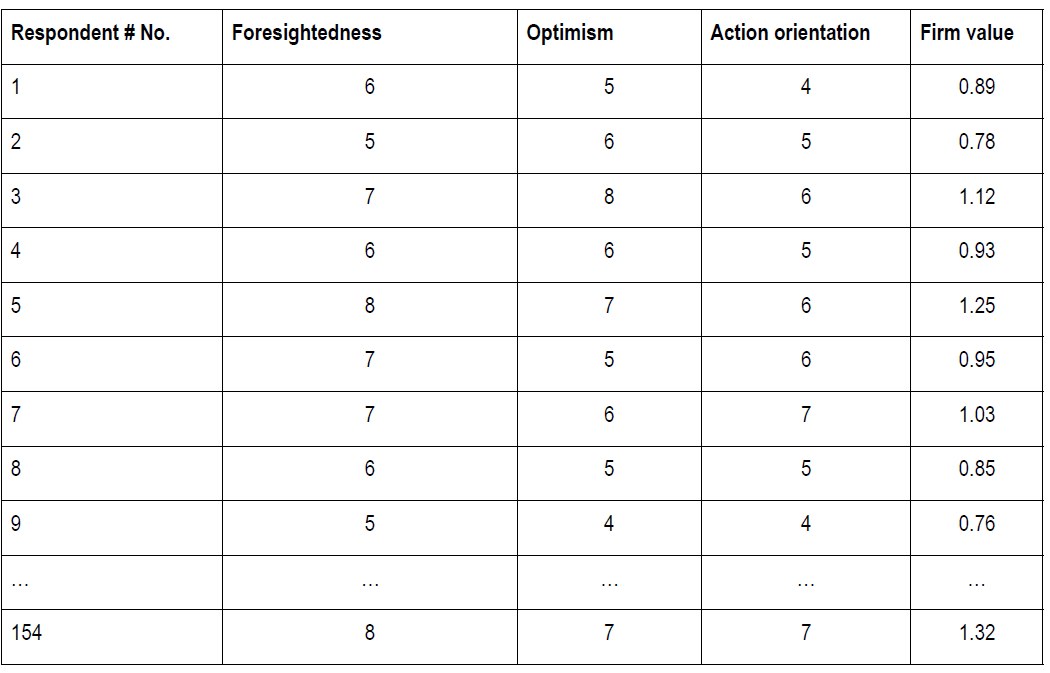

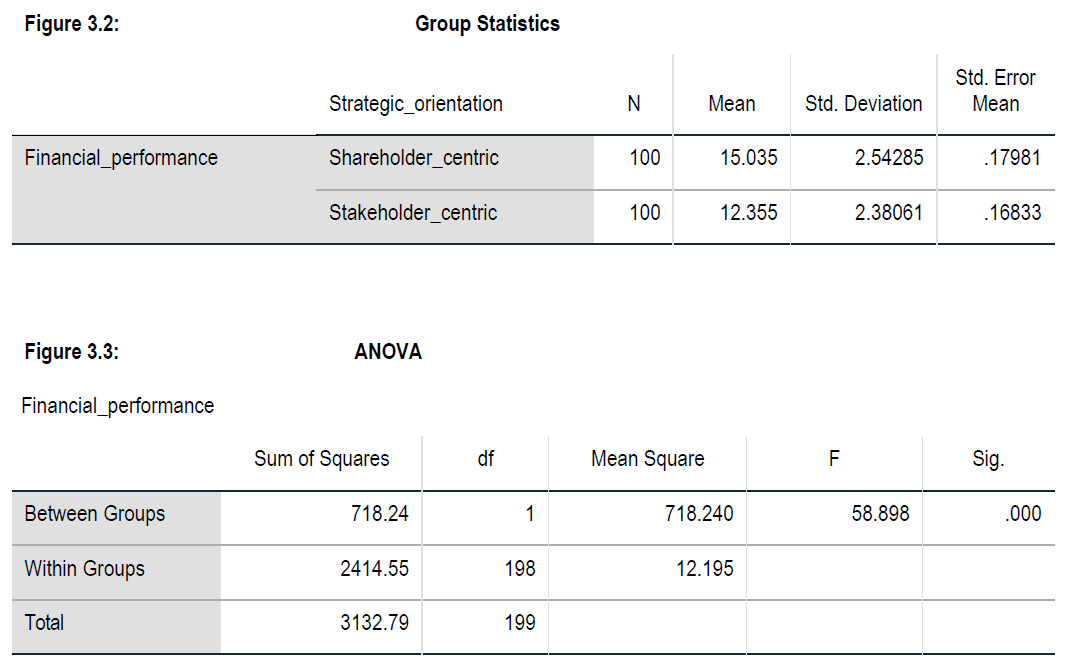

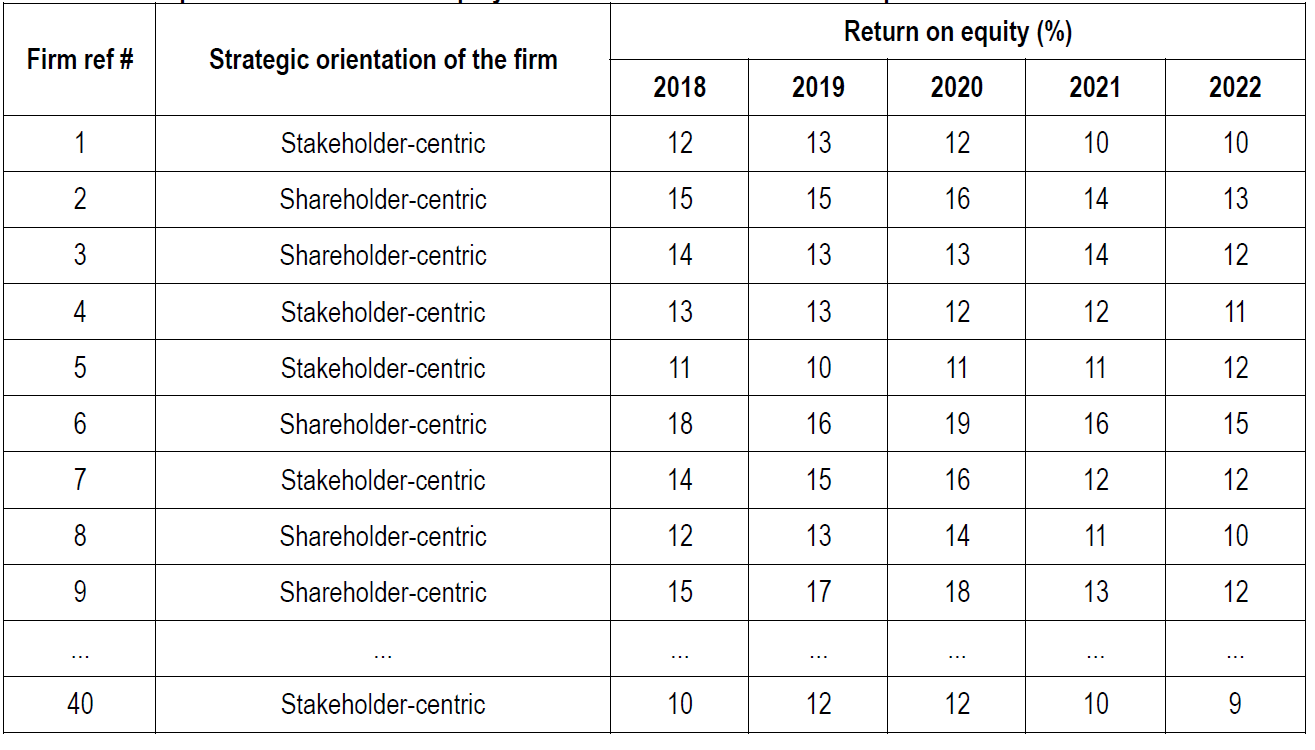

Under the current climate of changing societal expectations of the role of the firm, an organisational researcher is undertaking a study with the aim of examining the comparative impacts of shareholder-centric and stakeholder-centric strategies on organisational financial performance. Table 3.1, below, depicts the excerpt of the data on financial performance (i.e., return on equity) collected from 40 South African firms over the 2018-2022 period (20 of the firms follow the shareholder primacy model and the other 20, the stakeholder theory).

Table 3.1: excerpt of data on return on equity from 40 firms over the 2018-2022 period.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Stage Managers Toolkit

Authors: Laurie Kincman

2nd Edition

1138183776, 978-1138183773