Answered step by step

Verified Expert Solution

Question

1 Approved Answer

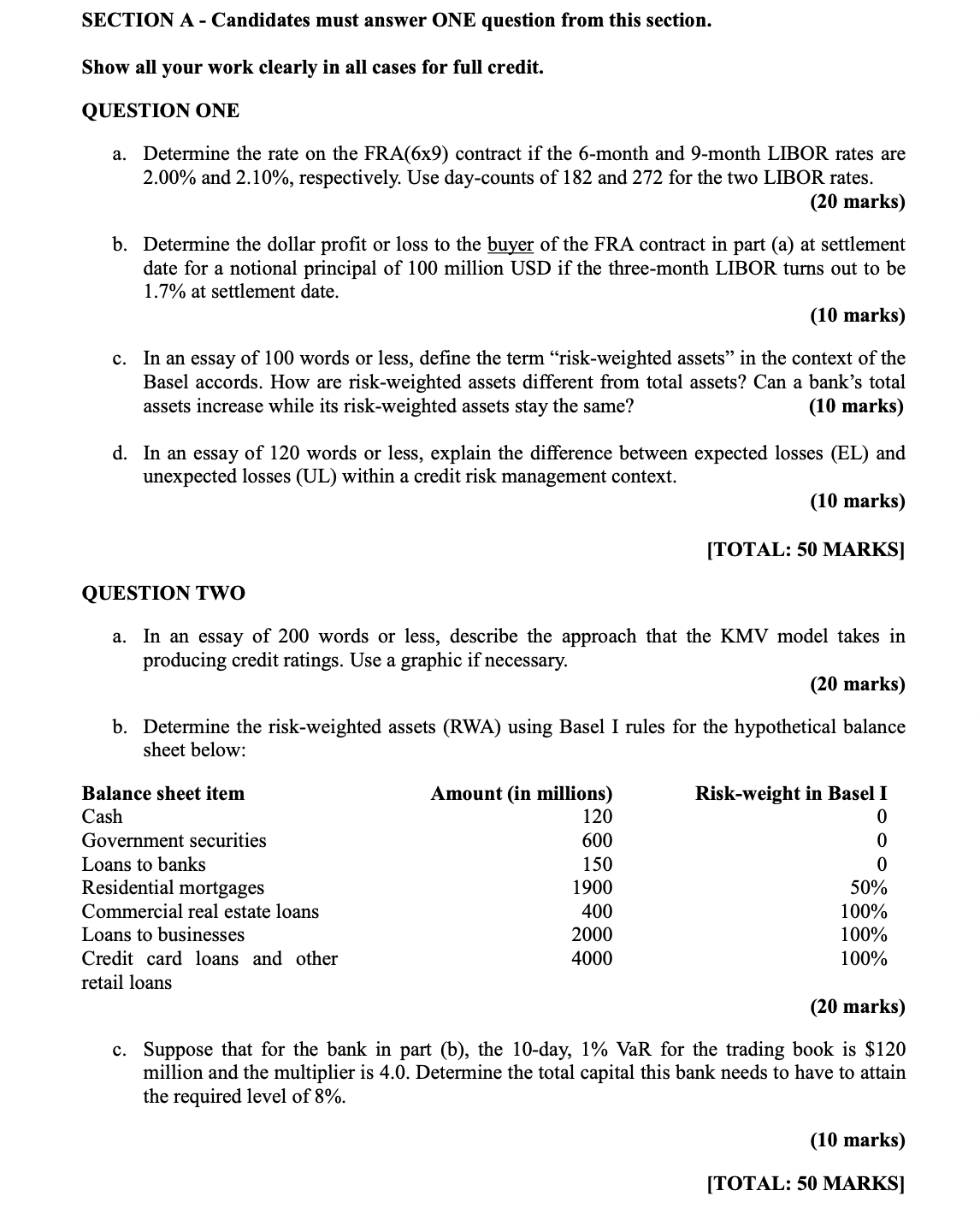

SECTION A- Candidates must answer ONE question from this section. Show all your work clearly in all cases for full credit. QUESTION ONE a.

SECTION A- Candidates must answer ONE question from this section. Show all your work clearly in all cases for full credit. QUESTION ONE a. Determine the rate on the FRA(6x9) contract if the 6-month and 9-month LIBOR rates are 2.00% and 2.10%, respectively. Use day-counts of 182 and 272 for the two LIBOR rates. (20 marks) b. Determine the dollar profit or loss to the buyer of the FRA contract in part (a) at settlement date for a notional principal of 100 million USD if the three-month LIBOR turns out to be 1.7% at settlement date. (10 marks) c. In an essay of 100 words or less, define the term "risk-weighted assets" in the context of the Basel accords. How are risk-weighted assets different from total assets? Can a bank's total assets increase while its risk-weighted assets stay the same? (10 marks) d. In an essay of 120 words or less, explain the difference between expected losses (EL) and unexpected losses (UL) within a credit risk management context. (10 marks) [TOTAL: 50 MARKS] QUESTION TWO a. In an essay of 200 words or less, describe the approach that the KMV model takes in producing credit ratings. Use a graphic if necessary. (20 marks) b. Determine the risk-weighted assets (RWA) using Basel I rules for the hypothetical balance sheet below: Balance sheet item Cash Government securities Loans to banks Residential mortgages Commercial real estate loans Loans to businesses Credit card loans and other retail loans Amount (in millions) Risk-weight in Basel I 120 0 600 0 150 0 1900 50% 400 100% 2000 100% 4000 100% (20 marks) c. Suppose that for the bank in part (b), the 10-day, 1% VaR for the trading book is $120 million and the multiplier is 4.0. Determine the total capital this bank needs to have to attain the required level of 8%. (10 marks) [TOTAL: 50 MARKS]

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles Of Managerial Finance

Authors: Lawrence J. Gitman, Chad J. Zutter

13th Edition

9780132738729, 136119468, 132738724, 978-0136119463