Answered step by step

Verified Expert Solution

Question

1 Approved Answer

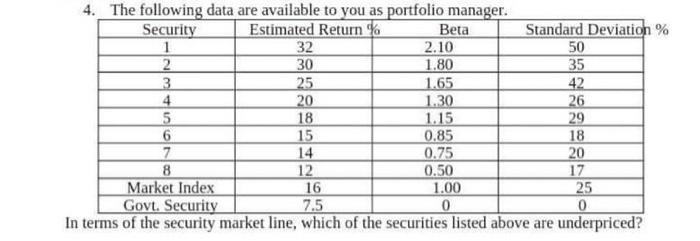

Security 4. The following data are available to you as portfolio manager. Estimated Return % Standard Deviation % Beta 1 32 2.10 50 2

Security 4. The following data are available to you as portfolio manager. Estimated Return % Standard Deviation % Beta 1 32 2.10 50 2 30 1.80 35 3 25 1.65 42 4 20 1.30 26 5 18 1.15 29 6 15 0.85 18 7 14 0.75 20 8 12 0.50 17 Market Index 16 1.00 25 Govt. Security 7.5 0 0 In terms of the security market line, which of the securities listed above are underpriced?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

To determine which securities are underpriced based on the security market line SML we need to compa...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Linear Algebra And Its Applications

Authors: David Lay, Steven Lay, Judi McDonald

6th Global Edition

978-1292351216, 1292351217