Answered step by step

Verified Expert Solution

Question

1 Approved Answer

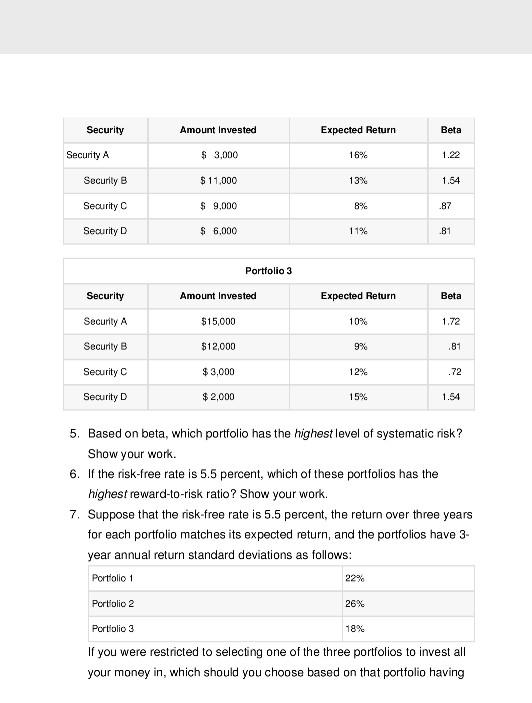

Security Amount Invested Expected Return Beta Security A $ 3,000 16% 1.22 Security B $11,000 13% 1.54 Security C $ 9,000 8% .87 Security D

Security Amount Invested Expected Return Beta Security A $ 3,000 16% 1.22 Security B $11,000 13% 1.54 Security C $ 9,000 8% .87 Security D $ 6,000 11% .81 Portfolio 3 Security Amount Invested Expected Return Beta Security A $15,000 10% 1.72 Security B $12,000 9% .81 Security C $3,000 12% .72 Security D $ 2.000 15% 1.54 5. Based on beta, which portfolio has the highest level of systematic risk? Show your work. 6. If the risk-free rate is 5.5 percent, which of these portfolios has the highest reward-to-risk ratio? Show your work. 7. Suppose that the risk-free rate is 5.5 percent, the return over three years for each portfolio matches its expected return, and the portfolios have 3- year annual return standard deviations as follows: Portfolio 1 22% Portfolio 2 26% Portiolio 3 18% If you were restricted to selecting one of the three portfolios to invest all your money in, which should you choose based on that portfolio having Security Amount Invested Expected Return Beta Security A $ 3,000 16% 1.22 Security B $11,000 13% 1.54 Security C $ 9,000 8% .87 Security D $ 6,000 11% .81 Portfolio 3 Security Amount Invested Expected Return Beta Security A $15,000 10% 1.72 Security B $12,000 9% .81 Security C $3,000 12% .72 Security D $ 2.000 15% 1.54 5. Based on beta, which portfolio has the highest level of systematic risk? Show your work. 6. If the risk-free rate is 5.5 percent, which of these portfolios has the highest reward-to-risk ratio? Show your work. 7. Suppose that the risk-free rate is 5.5 percent, the return over three years for each portfolio matches its expected return, and the portfolios have 3- year annual return standard deviations as follows: Portfolio 1 22% Portfolio 2 26% Portiolio 3 18% If you were restricted to selecting one of the three portfolios to invest all your money in, which should you choose based on that portfolio having

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Markets And Institutions

Authors: Frederic S. Mishkin, Stanley Eakins

6th Edition

0321374215, 9780321374219