Answered step by step

Verified Expert Solution

Question

1 Approved Answer

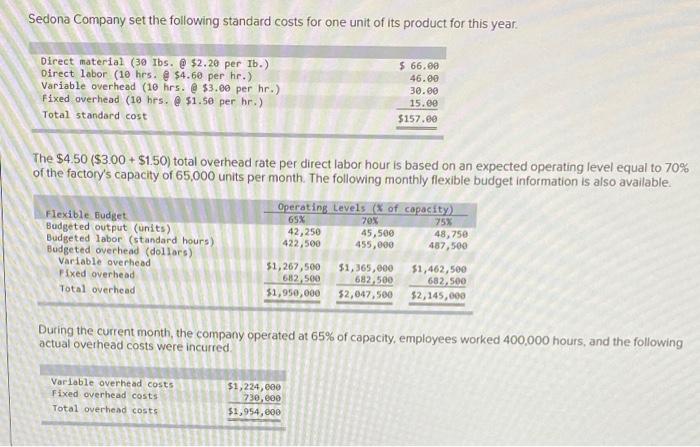

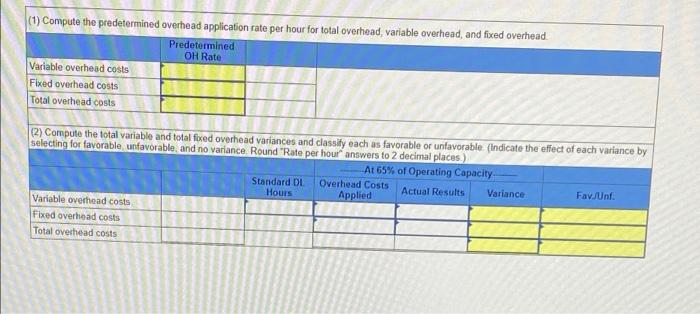

Sedona Company set the following standard costs for one unit of its product for this year. Direct material (30 lbs. @ $2.28 per Ib.) Direct

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managerial Accounting

Authors: Charles E. Davis, Elizabeth Davis

2nd edition

1118548639, 9781118800713, 1118338448, 9781118548639, 1118800710, 978-1118338445