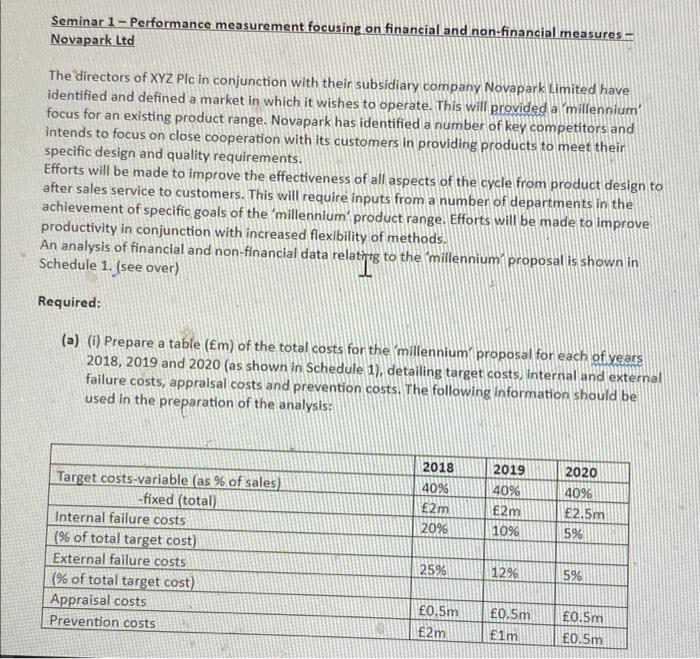

Seminar 1 - Performance measurement focusing on financial and non-financial measures - Novapark Ltd The directors of XYZ Plc in conjunction with their subsidiary company Novapark Limited have identified and defined a market in which it wishes to operate. This will provided a 'millennium' focus for an existing product range. Novapark has identified a number of key competitors and intends to focus on close cooperation with its customers in providing products to meet their specific design and quality requirements. Efforts will be made to improve the effectiveness of all aspects of the cycle from product design to after sales service to customers. This will require inputs from a number of departments in the achievement of specific goals of the 'millennium product range. Efforts will be made to improve productivity in conjunction with increased flexibility of methods. An analysis of financial and non-financial data relating to the 'millennium proposal is shown in Schedule 1. (see over) relations Required: (a) (i) Prepare a table (Em) of the total costs for the 'millennium proposal for each of years 2018, 2019 and 2020 (as shown in Schedule 1), detailing target costs, internal and external failure costs, appraisal costs and prevention costs. The following information should be used in the preparation of the analysis: 2019 2020 2018 40% 2m 20% 4096 40% 2m 10% 2.5m 5% Target costs-variable (as % of sales) -fixed (total) Internal failure costs (% of total target cost) External failure costs (% of total target cost) Appraisal costs Prevention costs 25% 12% 5% 0.5m 2m 0.5m Elm 0.5m 0.5m Seminar 1 - Performance measurement focusing on financial and non-financial measures - Novapark Ltd The directors of XYZ Plc in conjunction with their subsidiary company Novapark Limited have identified and defined a market in which it wishes to operate. This will provided a 'millennium' focus for an existing product range. Novapark has identified a number of key competitors and intends to focus on close cooperation with its customers in providing products to meet their specific design and quality requirements. Efforts will be made to improve the effectiveness of all aspects of the cycle from product design to after sales service to customers. This will require inputs from a number of departments in the achievement of specific goals of the 'millennium product range. Efforts will be made to improve productivity in conjunction with increased flexibility of methods. An analysis of financial and non-financial data relating to the 'millennium proposal is shown in Schedule 1. (see over) relations Required: (a) (i) Prepare a table (Em) of the total costs for the 'millennium proposal for each of years 2018, 2019 and 2020 (as shown in Schedule 1), detailing target costs, internal and external failure costs, appraisal costs and prevention costs. The following information should be used in the preparation of the analysis: 2019 2020 2018 40% 2m 20% 4096 40% 2m 10% 2.5m 5% Target costs-variable (as % of sales) -fixed (total) Internal failure costs (% of total target cost) External failure costs (% of total target cost) Appraisal costs Prevention costs 25% 12% 5% 0.5m 2m 0.5m Elm 0.5m 0.5m