Answered step by step

Verified Expert Solution

Question

1 Approved Answer

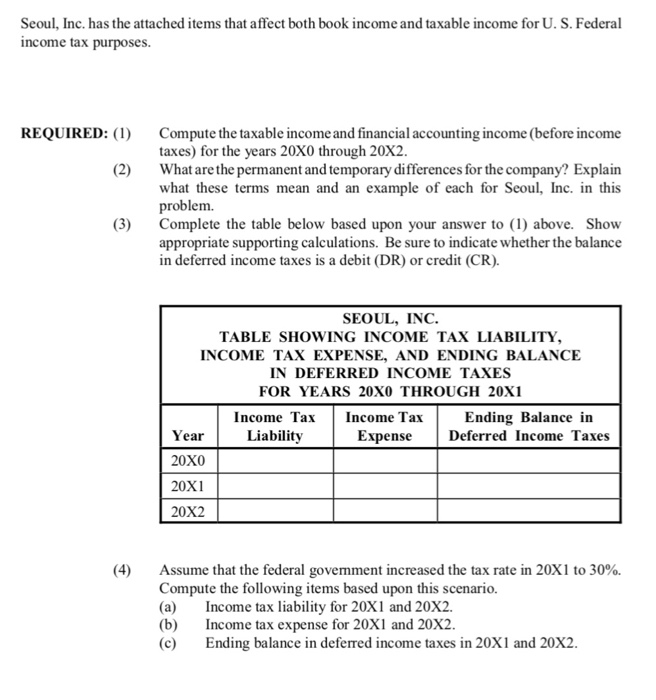

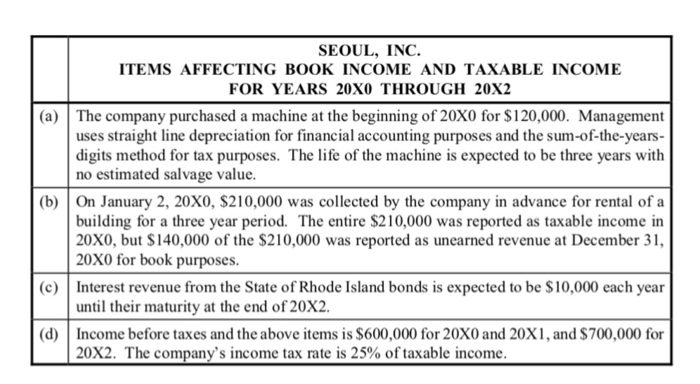

Seoul, Inc. has the attached items that affect both book income and taxable income for U. S. Federal income tax purposes. REQUIRED: ()Compute the taxable

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Shariah Audit Framework A Case Study Of UAE Noor Takaful Operations

Authors: Abdussalam Ismail Onagun

1st Edition

3659644064, 978-3659644061