Answered step by step

Verified Expert Solution

Question

1 Approved Answer

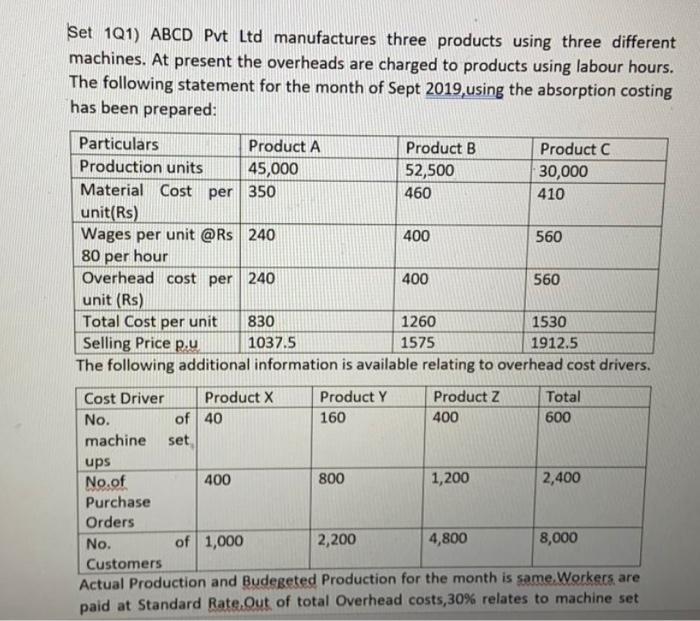

Set 1Q1) ABCD Pvt Ltd manufactures three products using three different machines. At present the overheads are charged to products using labour hours. The following

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Auditing Principles Practice And Problems

Authors: Jagdish Prakash

1st Edition

9327244745, 978-9327244748