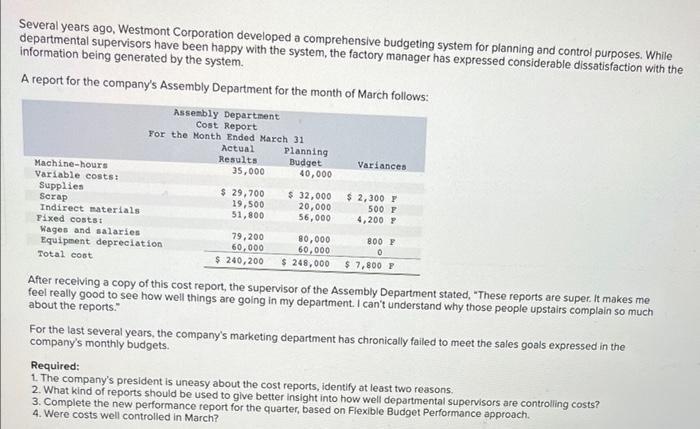

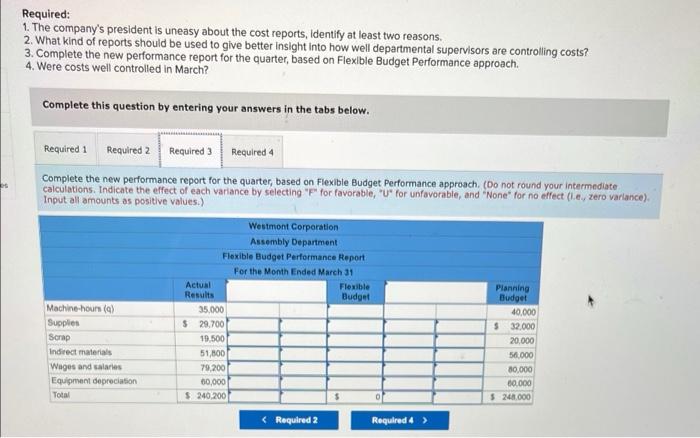

Several years ago, Westmont Corporation developed a comprehensive budgeting system for planning and control purposes. While departmental supervisors have been happy with the system, the factory manager has expressed considerable dissatisfaction with the information being generated by the system. A report for the company's Assembly Department for the month of March follows: Assembly Department Cost Report For the Month Ended March 31 Actual Planning Results Budget Variances Machine-hours 35,000 Variable costs: 40,000 Supplies $ 29,700 $ 32,000 $ 2,300 Serap 19,500 20,000 500 F Indirect materials 51,800 56,000 4, 2007 Fixed costs: Wages and salaries 79,200 80,000 800 Y Equipment depreciation 60,000 60,000 Total cost $ 240,200 $ 248,000 $ 7,800 P After receiving a copy of this cost report, the supervisor of the Assembly Department stated, "These reports are super. It makes me feel really good to see how well things are going in my department. I can't understand why those people upstairs complain so much about the reports." For the last several years, the company's marketing department has chronically failed to meet the sales goals expressed in the company's monthly budgets. Required: 1. The company's president is uneasy about the cost reports, identify at least two reasons. 2. What kind of reports should be used to give better insight into how well departmental supervisors are controlling costs? 3. Complete the new performance report for the quarter, based on Flexible Budget Performance approach. 4. Were costs well controlled in March? 0 Required: 1. The company's president is uneasy about the cost reports, Identify at least two reasons. 2. What kind of reports should be used to give better insight into how well departmental supervisors are controlling costs? 3. Complete the new performance report for the quarter, based on Flexible Budget Performance approach. 4. Were costs well controlled in March? Complete this question by entering your answers in the tabs below. Required 1 Required 2 Required 3 Required Complete the new performance report for the quarter, based on Flexible Budget Performance approach. (Do not round your intermediate calculations. Indicate the effect of each variance by selecting "P" Por favorable, *U* for unfavorable, and "None for no effect (.e., zero varlance), Input all amounts as positive values.) Machine-hours (a) Supplies Scrap Indirect materials Wages and salaries Equipment depreciation Total Westmont Corporation Assembly Department Flexible Budget Performance Report For the Month Ended March 31 Actual Flexible Results Budget 35.000 $ 29,700 19.500 51,800 79,200 60,000 $240.200 $ Planning Budget 40,000 $32.000 20,000 50.000 80,000 00.000 $240.000