Answered step by step

Verified Expert Solution

Question

1 Approved Answer

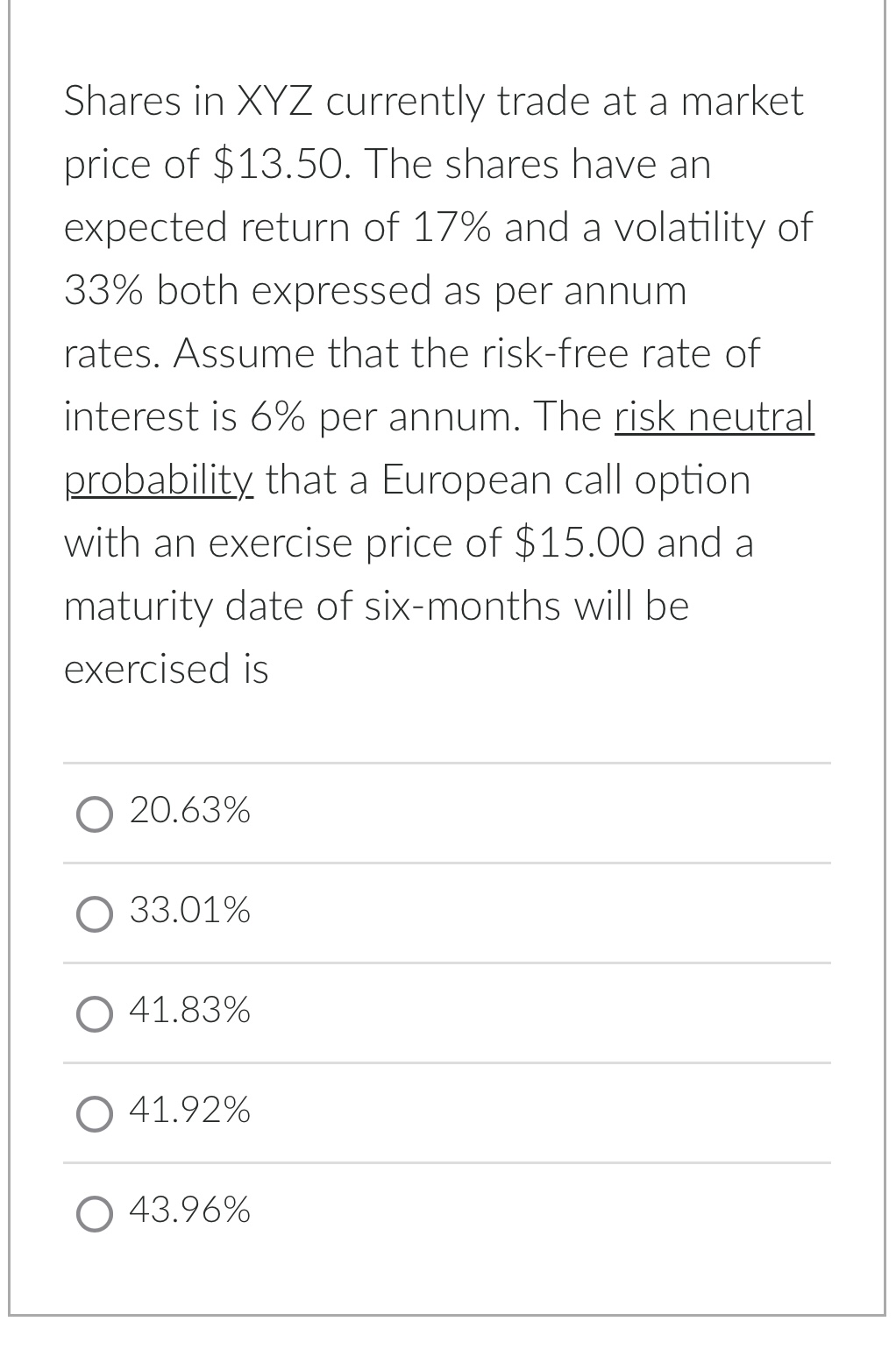

Shares in XYZ currently trade at a market price of $13.50. The shares have an expected return of 17% and a volatility of 33% both

Shares in XYZ currently trade at a market price of $13.50. The shares have an expected return of 17% and a volatility of 33% both expressed as per annum rates. Assume that the risk-free rate of interest is 6\% per annum. The risk neutral probability that a European call option with an exercise price of $15.00 and a maturity date of six-months will be exercised is \begin{tabular}{l} \hline 20.63% \\ \hline 33.01% \\ \hline 41.83% \\ \hline 41.92% \\ \hline 43.96% \\ \hline \end{tabular}

Shares in XYZ currently trade at a market price of $13.50. The shares have an expected return of 17% and a volatility of 33% both expressed as per annum rates. Assume that the risk-free rate of interest is 6\% per annum. The risk neutral probability that a European call option with an exercise price of $15.00 and a maturity date of six-months will be exercised is \begin{tabular}{l} \hline 20.63% \\ \hline 33.01% \\ \hline 41.83% \\ \hline 41.92% \\ \hline 43.96% \\ \hline \end{tabular} Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Automated Stock Trading Systems

Authors: Laurens Bensdorp

1st Edition

1544506031, 978-1544506036