Question

Sharon and Josh have already discussed some specific client acceptance issues, such as independence threats and safeguards. Sharon explains they also must consider the overall

Sharon and Josh have already discussed some specific client acceptance issues, such as independence threats and safeguards. Sharon explains they also must consider the overall integrity of the client (that is, management of Cloud 9). This means they need to perform and document procedures that are likely to provide information about the client's integrity. Josh is a little skeptical. "Do you mean that we should ask them if they are honest?" Sharon suggests it is probably more useful to ask others, and the key people to ask are the existing auditors. Josh is still skeptical. "The existing auditors are Ellis & Associates. Are they going to help us take one of their clients from them?" Sharon says the client must give permission first, and, if that is given, the existing auditor will usually state whether or not there were any issues that the new auditor should be aware of before accepting the work. This type of communication is covered by AS 2610 (AU-C 210 for private company clients) and is part of professional ethics.

Sharon also gives Josh the task of researching Cloud 9's press coverage, with special focus on anything that may indicate poor management integrity. Sharon emphasizes they must perform and document procedures to determine whether W&S Partners is competent to perform the engagement and has the capabilities, time, and resources to do so. For example, they must make sure they have audit team members who understand the clothing and footwear business. They also must have enough staff to complete the audit on time.

In addition, Sharon and Josh must perform and document procedures to show that W&S Partners can comply with all parts of the code of professional conduct, not just those that focus on independence threats and safeguards. Finally, they can draft the engagement letter to cover the contractual relationship between W&S Partners and Cloud 9.

"Great news!" announces Sharon at the weekly team meeting. "We just received word that the audit engagement letter for Cloud 9 has been signed. We are now officially the auditors and the risk assessment phase starts now!"

Later, at the first planning meeting, Sharon and Josh focus on assigning the tasks for gaining an understanding of Cloud 9. Ian Harper, a first-year staff, is not happy. He grumbles to another member of the team, Suzie Pickering, as he leaves the room. "This is such a waste of time. Why did we sign an engagement letter if we don't understand the client? Why don't we just get on with the audit? What else is there to know?"

"Oh boy, are you missing the point!" Suzie says. "If you don't understand where the risks are greatest, where are you going to start 'getting on with it'?"

"The same place you always start," replies Ian.

Ian thinks that all audits are pretty much the same and that W&S Partners must have an audit plan they can use for the Cloud 9 audit. Suzie explains that if they tailor the plan to the client, the audit is far more likely to be efficient and effective. That is, they will get the job done without wasting time and ensure that quality evidence is gathered for the accounts that are most at risk of being misstated. If they can perform this, W&S Partners will not only issue the right audit report, but they will make a profit from the audit as well. In other words, if the plan is good, performing the audit properly will be easier.

Suzie realizes it will be a big job explaining this to Ian and invites him for a coffee in the staff room so they can talk. Suzie is an experienced staff and has worked with other clothing and footwear clients.

Throughout their conversation, Suzie and Ian have been discussing "material" misstatements in financial statements. Ian asks, "Isn't materiality just a number? Companies of about the same size would have the same materiality level, right?" Suzie explains that they will use a percentage of a benchmark, such as income before taxes or total revenue, as a starting place for determining materiality. Then, they will consider increasing or decreasing that amount based on qualitative factors specific to the Cloud 9 audit. For example, since Cloud 9 is a public company subject to regulation and more public scrutiny, the audit team may decide to decrease materiality, which means the team will perform more extensive audit procedures.

"Knowledge of the client's industry is important for determining materiality," continues Suzie. "We must be familiar with the client's operations and the industry to understand what is important, or material, to the users of the client's financial statements."

Ian is worried about getting the materiality level right. "What if we set it too low or too high?" Suzie explains that all parts of the audit plan, including the materiality decisions, will be reviewed throughout the audit and revised, if necessary.

Ian is still struggling with the idea of risk. He knows that audit risk is the risk that the auditor issues the wrong audit report, or gives an inappropriate audit opinion, and that audit risk is related to the client's circumstances. But how does that actually work in practice? What does an auditor do differently for each audit?

"Let's break this down," Suzie advises. "Auditors face the risk of stating that in their opinion the financial statements are not materially misstated, when in fact they are. So, how does a material misstatement get into the published financial statements?"

Ian works through the logic. "First, the error has to be created, either by accident or on purpose. Second, the client's internal control system must fail to either prevent the error getting into the accounts or detect the error once it is in the system. And, finally, the auditor has to fail to find the error during the audit."

"Correct!" says Suzie. "Now, before we go on, I want to break down the idea of 'financial statements,' too. The financial statements are the balance sheet (statement of financial position), income statement (statement of comprehensive income), cash flow statement (statement of cash flows), statement of changes in equity, and all the notes. So when we talk of the risk of misstatements, we are referring to the risk of misstatement in every line item in each of these statements. If we focus on just one line in a balance sheet?say, accounts receivable?what are the possible misstatements that could occur?"

Ian tries to work through the logic again. "The amount could be either understated or overstated. I suppose there are lots of errors that could occur. Obviously, basic math mistakes and other clerical errors could affect the total in either direction. In addition, accounts receivable would be understated if management omitted some customer receivables when they calculated the total. I think the deliberate 'mistakes' are more likely to overstate accounts receivable because that makes the balance sheet look better, and probably means profit is overstated, too. Accounts receivable would be overstated if some of the receivables management claimed in the total did not exist at year-end, did not belong to Cloud 9, were overvalued because bad debts were not written off, or sales from the next period were included in the earlier period."

"Very good," says Suzie. "It is the same for every line item. Every time management prepares a financial statement, they assert that all these errors did not occur?that all the individual items in the financial statements are not materially misstated. The auditor has to break down the financial statement audit into accounts and assertions and consider the risk of misstatement for each assertion for each account or transaction class. The auditor deals with the risk of material misstatement of the entire set of financial statements by gathering evidence at the assertion level for each account. Then, all the evidence is put together so the auditor can form an opinion on the overall financial statements."

Cloud 9 sells athletic shoes and apparel. The shoes are likely to "go out of fashion" reasonably quickly, making obsolescence a big issue. These factors affect the inherent risk of inventory valuation. There is also a risk of errors occurring in transactions with suppliers and customers, which will affect inventory balances. How high is the control risk? Much to Suzie's delight, Ian suggests they will be able to make better assessments of both inherent and control risk for all assertions once they have a better understanding of the client and its system of internal control.

Suzie explains that Cloud 9's audit could be planned and conducted in different ways, depending on the audit strategy adopted. In fact, the overall audit strategy sets the scope, timing, and direction of the audit, and guides the development of the detailed audit plan.

"What audit strategy would be suitable for Cloud 9? Start by thinking about the scope of the audit," she prompts. "The scope is about the different types of work we have to do?some audits have extra requirements."

"I suppose we should find out if Cloud 9 has any special requirements. The fact that it is a public company means we must follow the PCAOB auditing standards and conduct an audit of both the financial statements and the effectiveness of internal controls," Ian suggests.

"That is a good start," says Suzie. "What else?"

"Also," says Ian, "when are our staff available, and when are Cloud 9's key people available to talk to us?"

"Yes," says Suzie. "This is all basic. But if we don't ask these really important questions, we will find ourselves unable to meet the deadline and perhaps under pressure to cut corners. We also have to think about timing of requests to third parties for information. Now, can you think of anything regarding the direction of the audit?"

"I understand about the extra requirements and working out the timing. But I don't really know what you mean by direction," Ian says, confused.

"We have already discussed it to some extent," Suzie explains. "Remember when we spoke about the risk for Cloud 9 created by obsolescence of inventory, and errors occurring with transactions with customers and suppliers? 'Direction' is about where we think there should be extra attention because of higher risk, and how we give that extra attention. We could, for example, make sure we have suitable experts available, if required, to value the inventory. This is also where we bring in our work on "Well, I can think of several other things, such as whether any other auditors will be involved, whether there are any foreign currency translation issues, any industry-specific regulations (although I don't think this is as big an issue for clothing and footwear as it would be for banks, for example), whether there are any service organizations involved such as payroll services, and whether software-aided audit technology is going to be used."

"Very good," says Suzie. "That will do for now. What about timing issues? Are there any special things we should take into account for Cloud 9?"

"What is the date the audit has to be finished?" asks Ian.

"Good question," says Suzie. "We will have a deadline, so we obviously have to work toward it." materiality, both setting materiality for planning purposes, and identifying the material account balances. In our plan, we need to allocate additional time to areas where there may be higher risk of material misstatement. And, one of our biggest tasks will be considering the evidence about the design and operating effectiveness of internal controls at Cloud 9, which we haven't yet considered in detail."

"I see," says Ian. "If we assess the internal controls as being strong, then we plan to do more testing of controls (to confirm our assessment), and less testing of the underlying substance of transactions and account balances. We have to put this in our plan now. But what if our first thoughts about controls are wrong? Will our plan be wrong?"

"That happens," replies Suzie. "That is why our initial plan is constantly changing as we gather more information about the client. Particularly, as in this case, for a new client that we don't have a lot of detailed information on yet. However, we already know what accounts are important to Cloud 9?the client's previous years' financial statements and interim results show us that."

Suzie explains fraud risk is always present, even though actual fraud is reasonably rare, and auditors must explicitly consider it as part of their risk assessment. Being aware of the incentives, pressures, opportunities, and attitudes within the client relating to fraud helps the auditor make the assessment. Ian admits he has a little trouble understanding the difference between incentives and attitudes. He thinks he understands the concept of opportunity.

Suzie explains that incentives relate to the factor that pushes (or pulls) a person to commit a fraud. Examples include a need for money to pay debts or gamble. Attitudes, or rationalization, relate to the thinking about the act of fraud. For example, the person believes it is acceptable to steal from a mean boss; that is, the theft is justified by the boss's "meanness."

W&S Partners has just won the January 31, 2023, audit for Cloud 9. The audit team assigned to this client is:

? Partner, Jo Wadley

? Audit manager, Sharon Gallagher

? Audit senior, Josh Thomas

? IT audit manager, Mark Batten

? Experienced staff, Suzie Pickering

? First-year staff, Ian Harper

As a part of the risk assessment phase for the new audit, the audit team needs to gain an understanding of Cloud 9's structure and its business environment, determine materiality, and assess the risk of material misstatement. This will assist the team in developing an audit strategy and designing the nature, extent, and timing of audit procedures.

One task during the planning phase is to consider the concept of materiality as it applies to the client. Auditors will design procedures to identify and correct errors or irregularities that would have a material effect on the financial statements and affect the decision-making of the users of the financial statements. Materiality is used in determining audit procedures and sample selections, and evaluating differences from client records to audit results. Materiality is the maximum amount of misstatement, individually or in aggregate, that can be accepted in the financial statements. In selecting the benchmark to be used to calculate materiality, the auditors should consider the key drivers of the business. They should ask, "What are the end users (that is, stockholders, banks, etc.) of the accounts going to be looking at?" For example, will stockholders be interested in profit figures that can be used to pay dividends and increase share price?

W&S Partners' audit methodology dictates that one planning materiality (PM) amount is to be used for the financial statements as a whole. The benchmark selected for determining materiality is the one determined to be the key driver of the business.

W&S Partners use the following percentages as starting points for the various benchmarks:

Benchmark

Threshold (%)

Income before tax

5.0Total revenue

0.5Gross profit

2.0Total assets

0.5Equity

1.0

These starting points can be increased or decreased by taking into account qualitative client factors, which could be:

? The nature of the client's business and industry (for example, rapidly changing, either through growth or downsizing, or an unstable environment).

? Whether the client is a public company (or subsidiary of) subject to regulations.

? The knowledge of or high risk of fraud.

Typically, income before tax is used; however, it cannot be used if reporting a loss for the year or if profitability is not consistent.

When calculating PM based on interim figures, it may be necessary to annualize the results. This allows the auditors to plan the audit properly based on an approximate projected year-end balance. Then, at year-end, the figure is adjusted, if necessary, to reflect the actual results.

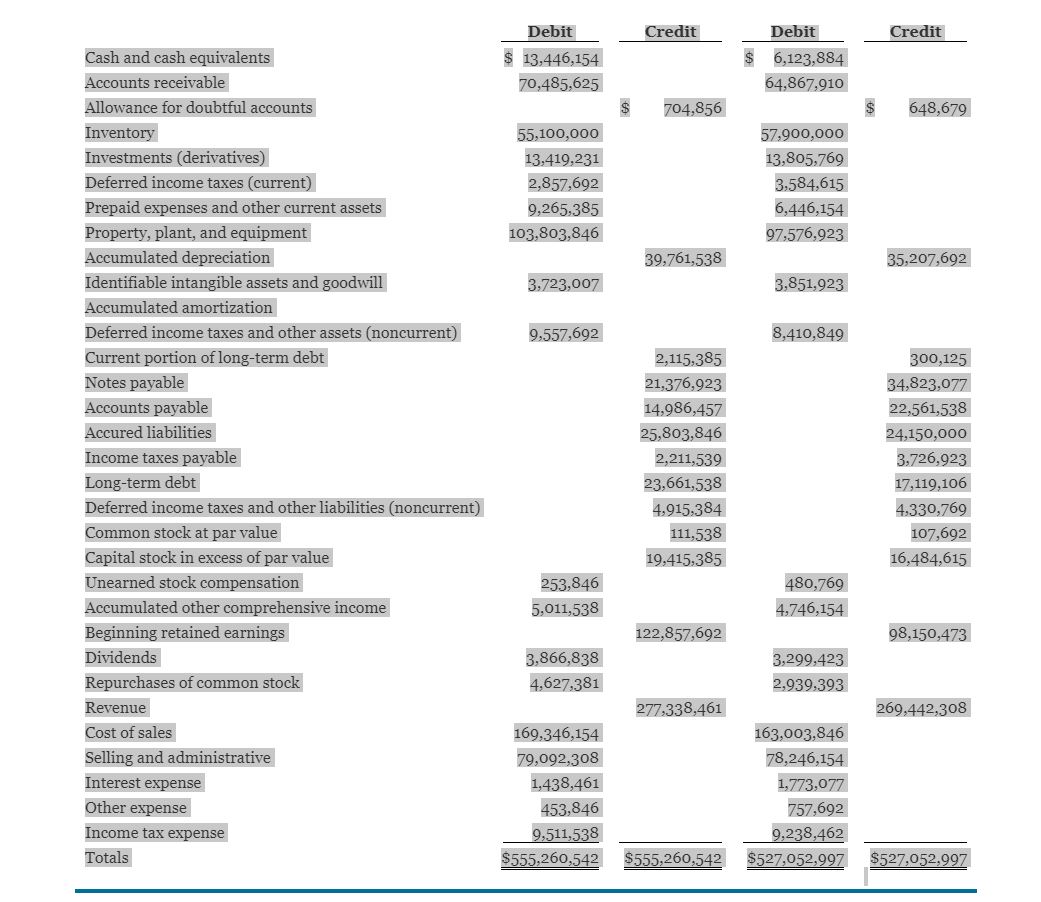

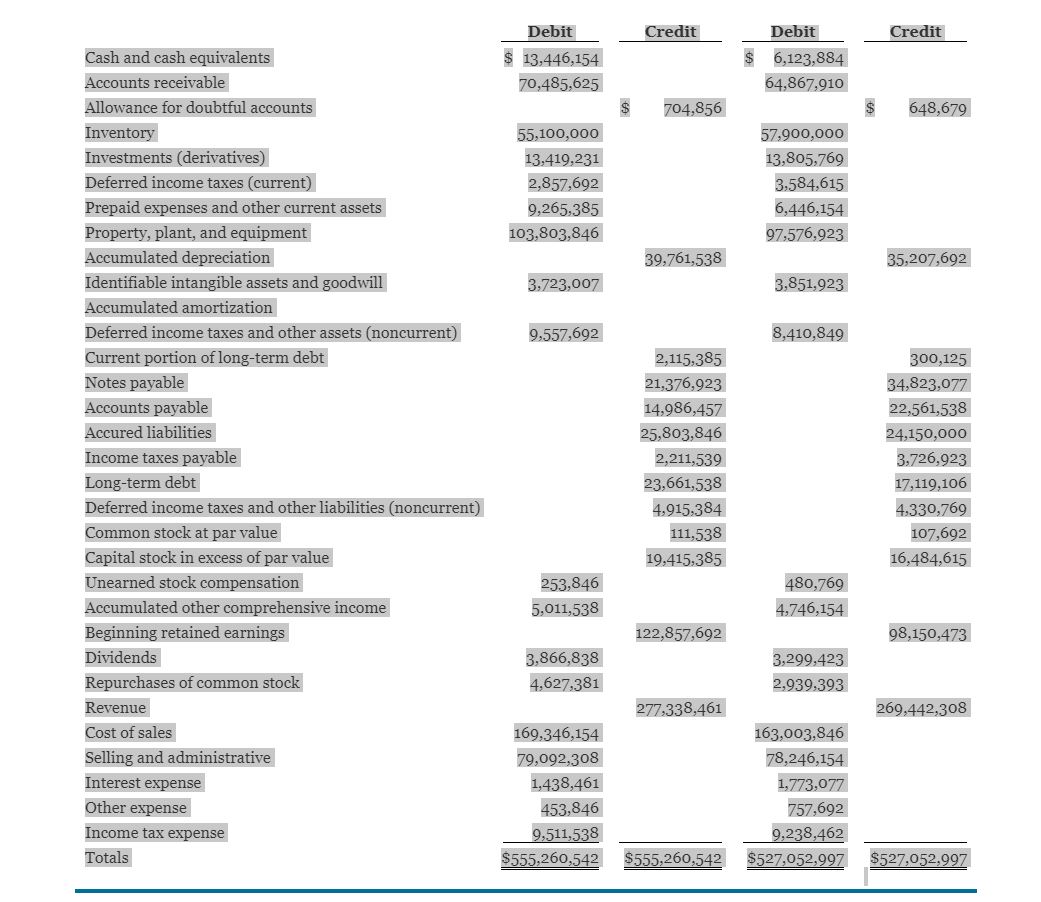

A.) Using the October 31, 2022, trial balance (in the appendix to this text), calculate planning materiality and include the justification for the benchmark that you have used for your calculation.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting Information Systems

Authors: Robert Hurt

4th Edition

78025885, 78025884, 9781259293795 , 978-0078025884