Answered step by step

Verified Expert Solution

Question

1 Approved Answer

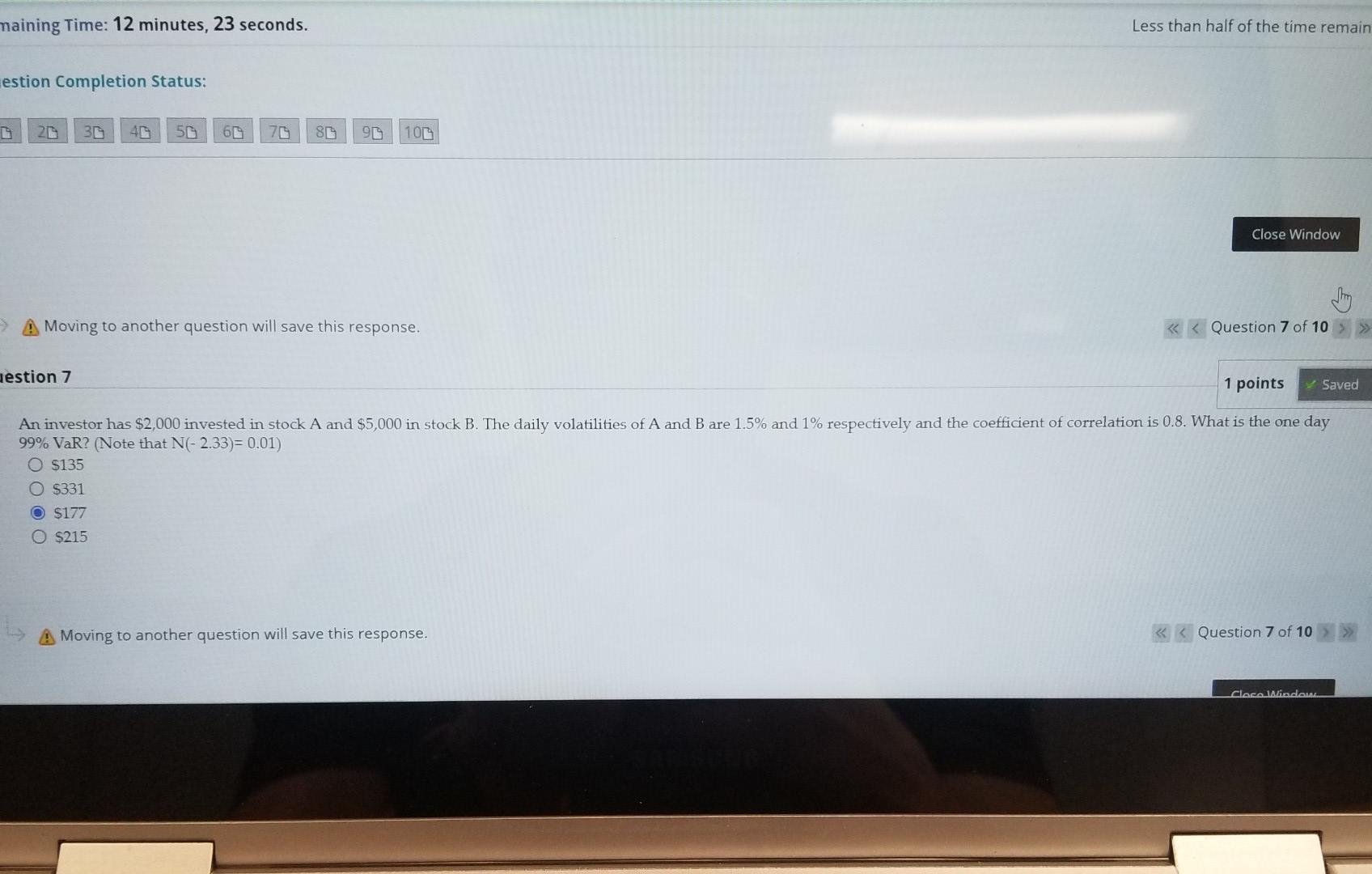

show formula please maining Time: 12 minutes, 23 seconds. Less than half of the time remain estion Completion Status: 26 30 56 66 76 80

show formula please

maining Time: 12 minutes, 23 seconds. Less than half of the time remain estion Completion Status: 26 30 56 66 76 80 96 100 Close Window > A Moving to another question will save this response. > aestion 7 1 points Saved An investor has $2,000 invested in stock A and $5,000 in stock B. The daily volatilities of A and B are 1.5% and 1% respectively and the coefficient of correlation is 0.8. What is the one day 99% VaR? (Note that N(-2.33)= 0.01) O $135 O $331 O $177 O $215 A Moving to another question will save this response.Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Pacific Economic Monitor July 2013

Authors: Asian Development Bank

1st Edition

9292541552,9292541560