Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Show step by - step procedures on how to reach the final answer. If a formula is used, write down the formula before plugging in

Show step bystep procedures on how to reach the final answer. If a formula is used, write down the formula before plugging in numbers; also provide a brief justification for the choice of the formula

Problem A: Valuation of stock options & Greeks

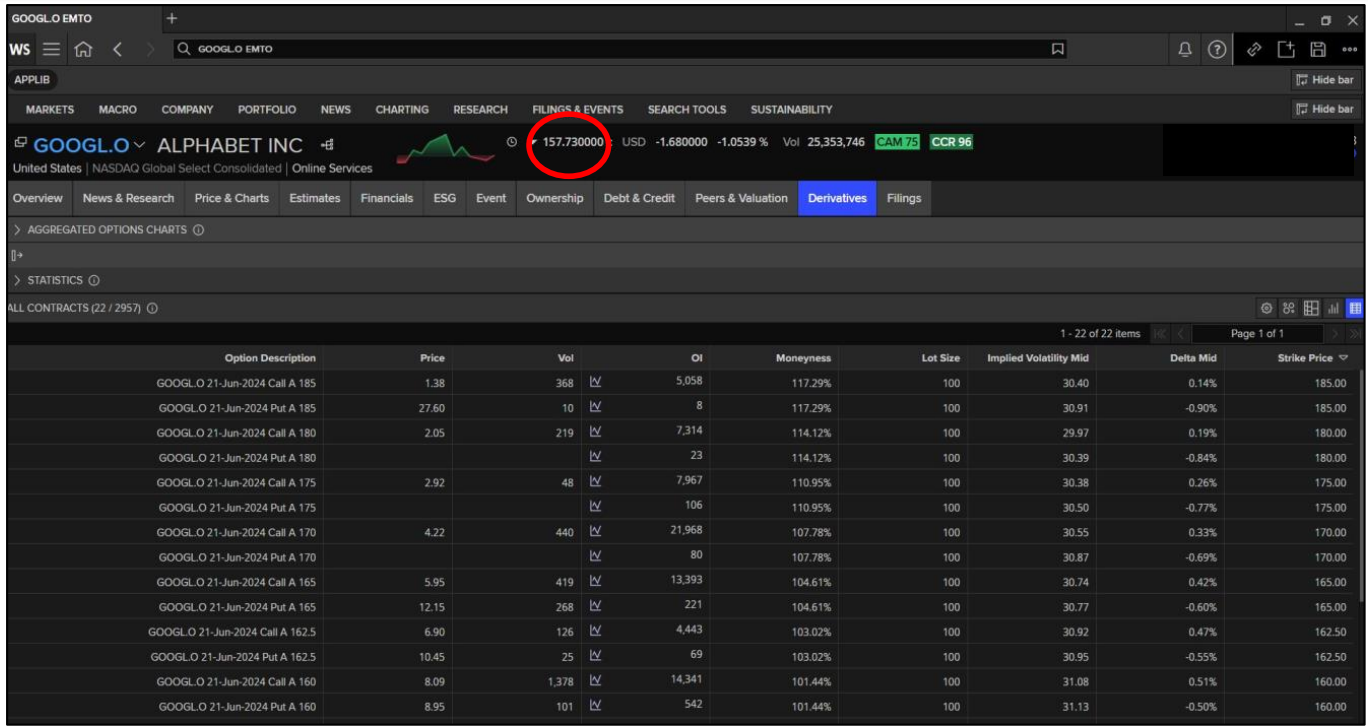

In this question, you need to price options with different option valuation approaches. The figure

below, extracted from Refinitiv Workspace, shows information for stock options on Alphabets

Google stock. Assume today is April Consider the options with the strike price of $

The option maturity is June Assume the benchmark riskfree interest rate is per

annum with continuous compounding for all maturities. Assume that the share price today is

$ and has a volatility of per annum.

Note: Ignore day count conventions and assume that one month of the year, two months of the year.

Figure Screen shot of Alphabet options Refinitiv Workspace a Calculate the up movement size in one month u and the down movement size d and round

these to the nearest second decimal place ie if u use

b Calculate the probability p of the stock price moving up in one month in the riskneutral world.

c Draw a binomial tree to show the stock price movement in the next two onemonth periods.

d Use a twostep binomial tree to calculate the value of a twomonth European call option

based on the noarbitrage approach.

e Use a twostep binomial tree to calculate the value of a twomonth European call option

based on the riskneutral valuation.

f Use a twostep binomial tree to calculate the value of a twomonth European put option

based on the riskneutral valuation.

g Use a twostep binomial tree to calculate the value of a twomonth American put option.

h Without calculations, show the American call option price if we assume the company will not

pay dividends during the option life and explain your approach

i Show whether the putcallparity holds for the European call and the European put prices

you just calculated in e and f

j Compare the put option prices you have just calculated with the actual put option price using

the Price column shown in the figure. Why are there differences? Briefly discuss some

possible reasons.

k What is the BlackScholesMerton price of a twomonth European call option?

l What is the BlackScholesMerton price of a twomonth European put option?

m Without calculations: What would happen to the option prices you just calculated in k and

l if the interest rate increases to Why?

n Calculate the BlackScholes deltas of the put and the call.

o Compare the call option prices you just calculated in e and k Compare also the put option

prices you calculated in f and l Do you expect these prices to be the same? WhyWhy

not?

p Finally, assume that you have a position in options. Using your results from n show

how you can deltahedge your position if

your position is a short position in European calls.

your position is a short position in European puts.

your position is a short position in European calls and European puts.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Investment Analysis And Portfolio Management

Authors: Frank K. Reilly, Peggy L. Hedges, Philip Chang, Keith C. Brown, Hedges Reilly Brown

1st Canadian Edition

0176500693, 978-0176500696