Answered step by step

Verified Expert Solution

Question

1 Approved Answer

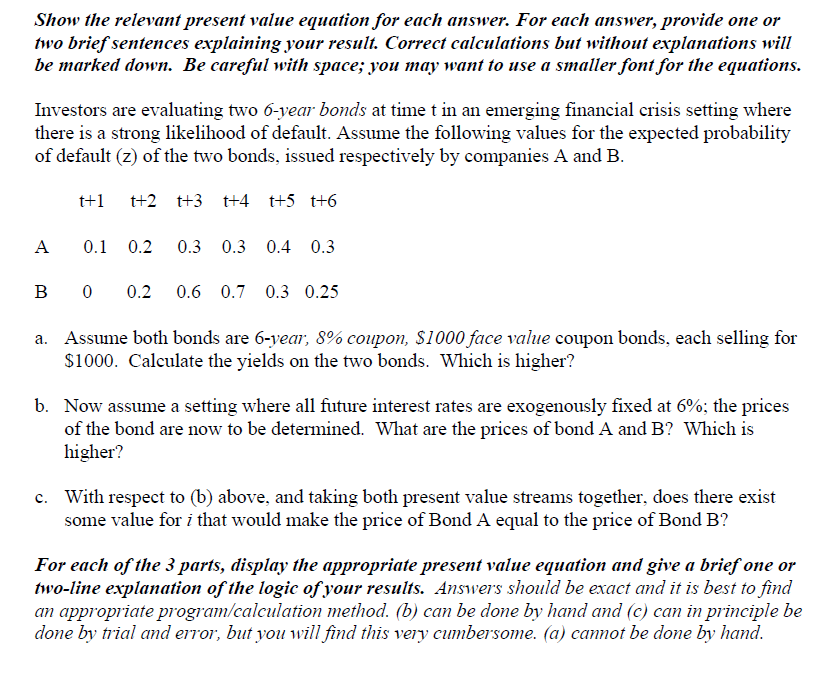

Show the relevant present value equation for each answer. For each answer, provide one or two brief sentences explaining your result. Correct calculations but without

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Introduction To Finance Markets, Investments, And Financial Management

Authors: Ronald W Melicher, Edgar Norton

13th Edition

0470128925, 9780470128923