Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Show work (25 points) 2. Tennessee National Bank has a stock portfolio with a market value of S40 million. The beta of the portfolio is

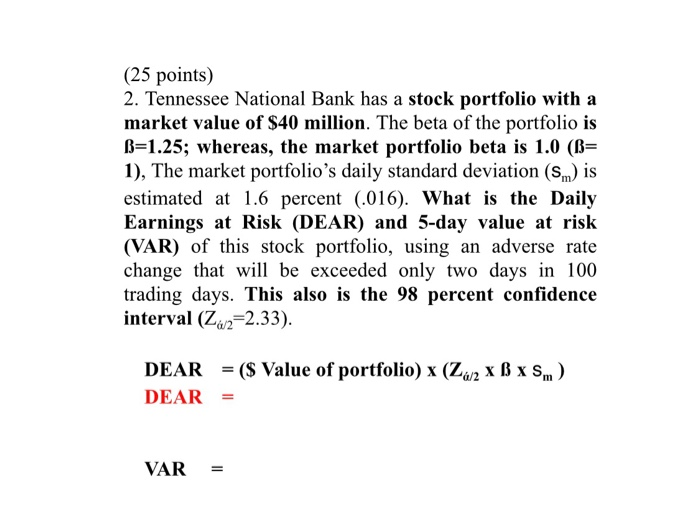

Show work (25 points) 2. Tennessee National Bank has a stock portfolio with a market value of S40 million. The beta of the portfolio is =1.25; whereas, the market portfolio beta is 1.0 (= 1), The market portfolio's daily standard deviation (Sm) is estimated at 1.6 percent (.016). What is the Daily Earnings at Risk (DEAR) and 5-day value at risk (VAR) of this stock portfolio, using an adverse rate change that will be exceeded only two days in 100 trading days. This also is the 98 percent confidence interval (Z2 2.33). DEAR DEAR -($ Value of portfolio) x (2 x x sm )

Show work (25 points) 2. Tennessee National Bank has a stock portfolio with a market value of S40 million. The beta of the portfolio is =1.25; whereas, the market portfolio beta is 1.0 (= 1), The market portfolio's daily standard deviation (Sm) is estimated at 1.6 percent (.016). What is the Daily Earnings at Risk (DEAR) and 5-day value at risk (VAR) of this stock portfolio, using an adverse rate change that will be exceeded only two days in 100 trading days. This also is the 98 percent confidence interval (Z2 2.33). DEAR DEAR -($ Value of portfolio) x (2 x x sm )

Show work Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance A Quantitative Introduction Volume 2

Authors: Piotr Staszkiewicz, Lucia Staszkiewicz

1st Edition

0128027975, 978-0128027974