Question: show work if possible Consider the following table, which gives a security analyst's expected return on two stocks and the market Index in two scenarios:

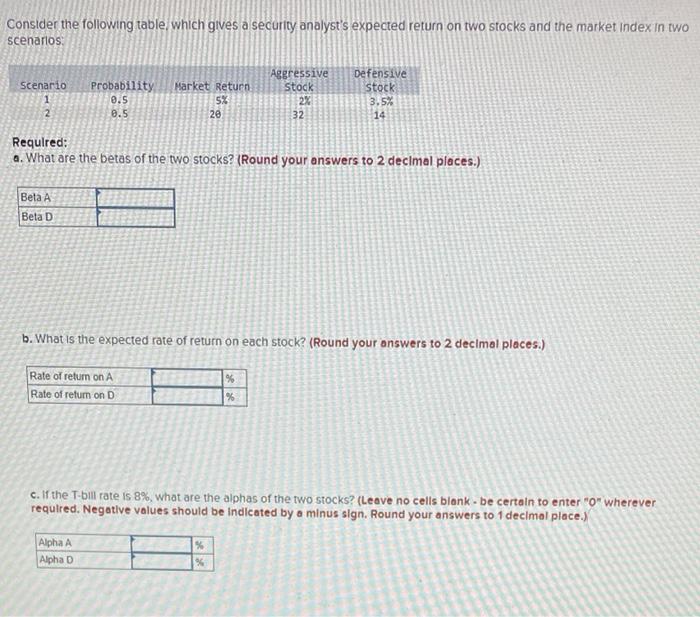

Consider the following table, which gives a security analyst's expected return on two stocks and the market Index in two scenarios: Defensive Aggressive Stock Scenario Probability Market Return stock 0.5 5% 2% 3.5% 2 0.5 20 32 14 Required: a. What are the betas of the two stocks? (Round your answers to 2 decimal places.) Beta A Beta D b. What is the expected rate of return on each stock? (Round your answers to 2 decimal places.) Rate of return on A % Rate of return on D % c. If the T-bill rate is 8%, what are the alphas of the two stocks? (Leave no cells blank - be certain to enter "0" wherever required. Negative values should be indicated by a minus sign. Round your answers to 1 decimal place.) % Alpha A Alpha D %

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts