Answered step by step

Verified Expert Solution

Question

1 Approved Answer

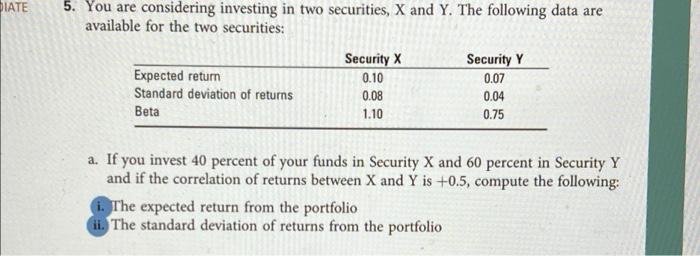

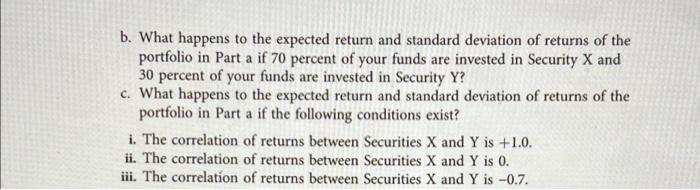

show work please DIATE 5. You are considering investing in two securities, X and Y. The following data are available for the two securities: Security

show work please

DIATE 5. You are considering investing in two securities, X and Y. The following data are available for the two securities: Security X Security Y Expected return 0.10 0.07 Standard deviation of returns 0.08 0.04 Beta 1.10 0.75 a. If you invest 40 percent of your funds in Security X and 60 percent in Security Y and if the correlation of returns between X and Y is +0.5, compute the following: 1. The expected return from the portfolio it. The standard deviation of returns from the portfolio b. What happens to the expected return and standard deviation of returns of the portfolio in Part a if 70 percent of your funds are invested in Security X and 30 percent of your funds are invested in Security Y? c. What happens to the expected return and standard deviation of returns of the portfolio in Part a if the following conditions exist? i. The correlation of returns between Securities X and Y is +1.0. ii. The correlation of returns between Securities X and Y is 0. iii. The correlation of returns between Securities X and Y is -0.7 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Nft Guide Learn How To Buy Sell Collect And Mint Non Fungible Tokens

Authors: Thomas Jase

1st Edition