Answered step by step

Verified Expert Solution

Question

1 Approved Answer

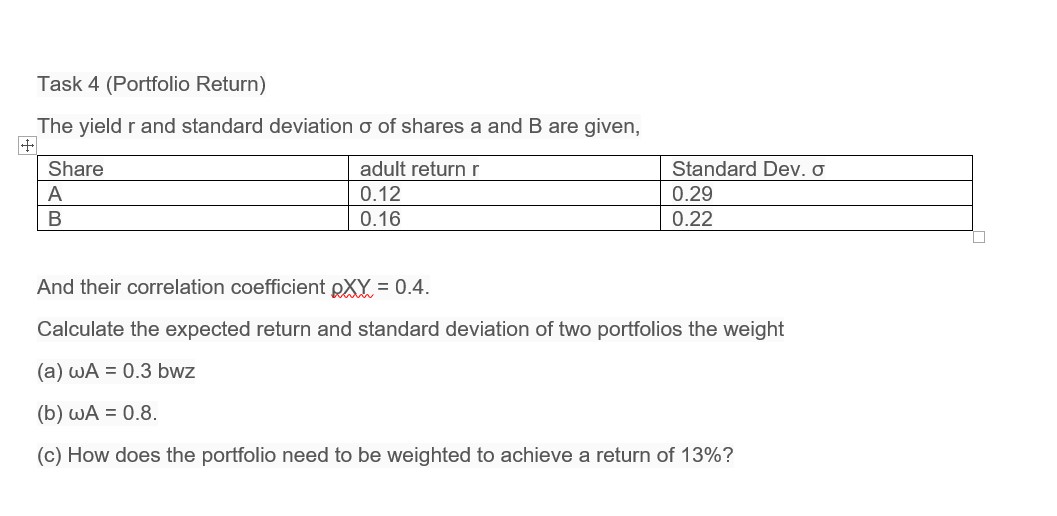

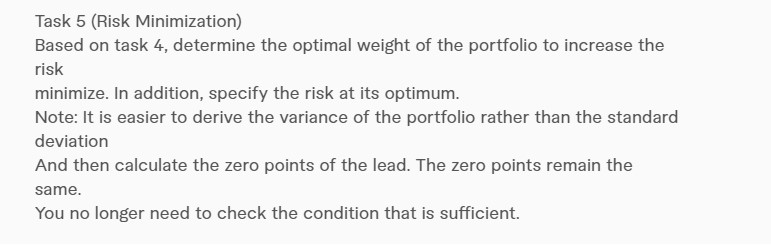

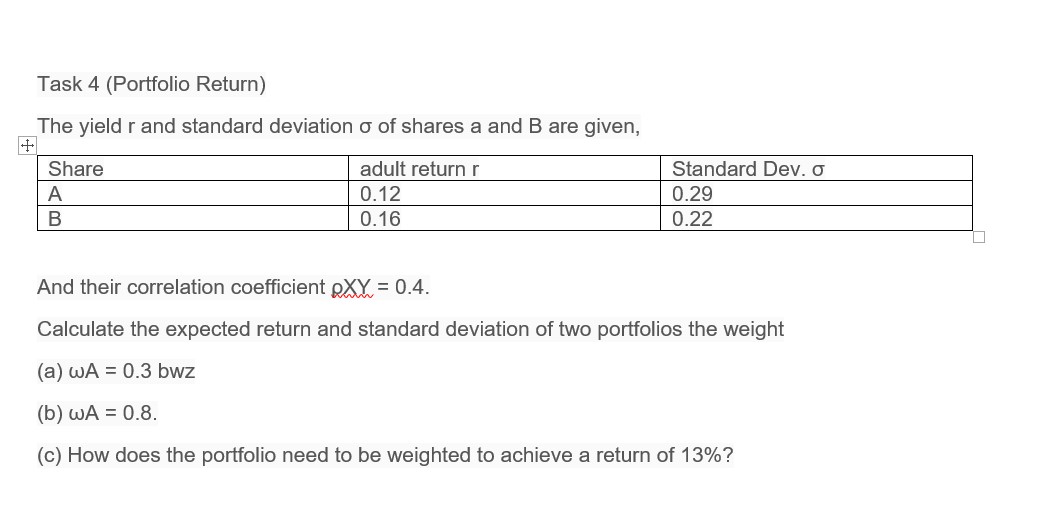

Sir, i am stuck on this question only task no 5 Task 5 (Risk Minimization) Based on task 4. determine the optimal weight of the

Sir, i am stuck on this question

only task no 5

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Functional Analysis And The Feynman Operator Calculus

Authors: Tepper L Gill, Woodford W Zachary, Zachary Woodford

1st Edition

331927595X, 9783319275956