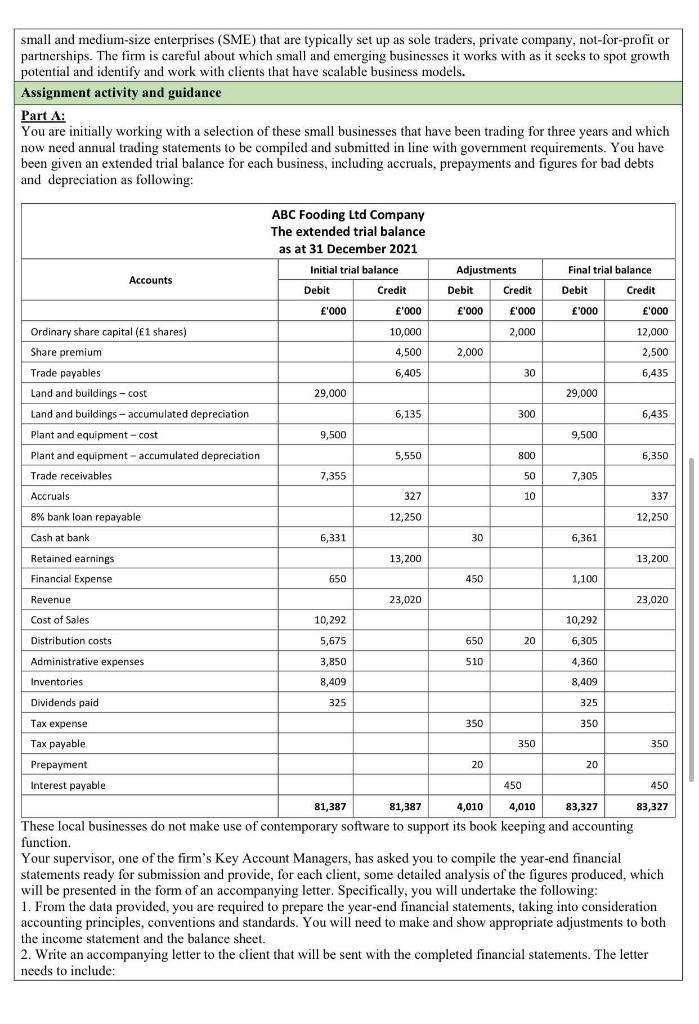

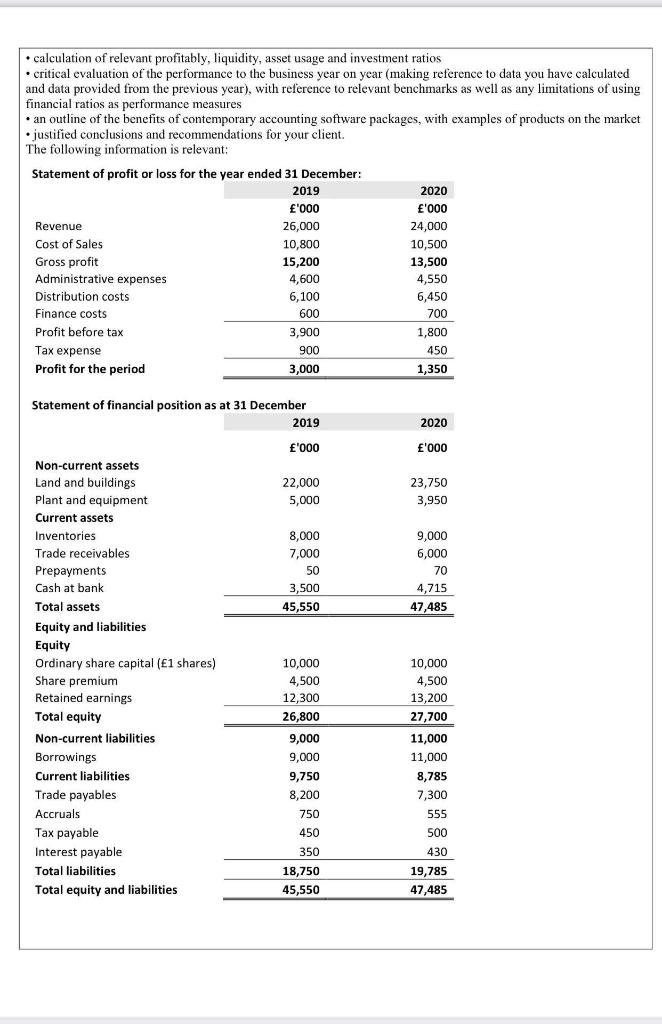

small and medium-size enterprises (SME) that are typically set up as sole traders, private company, not-for-profit or partnerships. The firm is careful about which small and emerging businesses it works with as it seeks to spot growth potential and identify and work with clients that have scalable business models. Assignment activity and guidance Part A: You are initially working with a selection of these small businesses that have been trading for three years and which now need annual trading statements to be compiled and submitted in line with government requirements. You have been given an extended trial balance for each business, including accruals, prepayments and figures for bad debts and depreciation as following: ABC Fooding Ltd Company The extended trial balance as at 31 December 2021 Initial trial balance Debit Credit Accounts Adjustments Debit Credit Final trial balance Debit Credit '000 ' '000 '000 '000 '000 ' '000 2,000 10,000 4,500 12,000 2,500 2,000 6,405 30 6,435 29,000 29,000 Ordinary share capital (E1 shares) Share premium Trade payables Land and buildings - cost Land and buildings -accumulated depreciation Plant and equipment -cost Plant and equipment-accumulated depreciation Trade receivables 6,135 300 6,435 9,500 9,500 5,550 800 6,350 7,355 50 7,305 Accruals 327 10 337 8% bank loan repayable 12,250 12,250 Cash at bank 6,331 30 6,361 Retained earnings 13,200 13,200 650 450 1,100 Financial Expense Revenue 23,020 23,020 Cost of Sales 10,292 10,292 5,675 650 20 6,305 Distribution costs Administrative expenses 3,850 510 4,360 Inventories 8,409 8,409 325 350 350 350 20 450 81,387 83,327 Dividends paid 325 Tax expense 350 Tax payable Prepayment 20 Interest payable 450 81,387 4,010 4,010 83,327 These local businesses do not make use of contemporary software to support its book keeping and accounting function. Your supervisor, one of the firm's Key Account Managers, has asked you to compile the year-end financial statements ready for submission and provide, for each client, some detailed analysis of the figures produced, which will be presented in the form of an accompanying letter. Specifically, you will undertake the following: 1. From the data provided, you are required to prepare the year-end financial statements, taking into consideration accounting principles, conventions and standards. You will need to make and show appropriate adjustments to both the income statement and the balance sheet. Write an accompanying letter to the client that will be sent with the completed financial statements. The letter needs to include: calculation of relevant profitably, liquidity, asset usage and investment ratios . critical evaluation of the performance to the business year on year (making reference to data you have calculated and data provided from the previous year), with reference to relevant benchmarks as well as any limitations of using financial ratios as performance measures an outline of the benefits of contemporary accounting software packages, with examples of products on the market justified conclusions and recommendations for your client. The following information is relevant: Statement of profit or loss for the year ended 31 December: 2019 2020 '000 '000 Revenue 26,000 24,000 Cost of Sales 10,800 10,500 Gross profit 15,200 13,500 Administrative expenses 4,600 4,550 Distribution costs 6,100 6,450 Finance costs 600 700 Profit before tax 3,900 1,800 Tax expense 900 450 Profit for the period 3,000 1,350 Statement of financial position as at 31 December 2019 2020 '000 '000 22,000 5,000 23,750 3,950 8,000 7,000 50 9,000 6,000 70 4,715 47,485 3,500 45,550 Non-current assets Land and buildings Plant and equipment Current assets Inventories Trade receivables Prepayments Cash at bank Total assets Equity and liabilities Equity Ordinary share capital (E1 shares) Share premium Retained earnings Total equity Non-current liabilities Borrowings Current liabilities Trade payables Accruals Tax payable Interest payable Total liabilities Total equity and liabilities 10,000 4,500 12,300 26,800 9,000 9,000 9,750 8,200 10,000 4,500 13,200 27,700 11,000 11,000 8,785 7,300 750 555 450 350 500 430 18,750 45,550 19,785 47,485 small and medium-size enterprises (SME) that are typically set up as sole traders, private company, not-for-profit or partnerships. The firm is careful about which small and emerging businesses it works with as it seeks to spot growth potential and identify and work with clients that have scalable business models. Assignment activity and guidance Part A: You are initially working with a selection of these small businesses that have been trading for three years and which now need annual trading statements to be compiled and submitted in line with government requirements. You have been given an extended trial balance for each business, including accruals, prepayments and figures for bad debts and depreciation as following: ABC Fooding Ltd Company The extended trial balance as at 31 December 2021 Initial trial balance Debit Credit Accounts Adjustments Debit Credit Final trial balance Debit Credit '000 ' '000 '000 '000 '000 ' '000 2,000 10,000 4,500 12,000 2,500 2,000 6,405 30 6,435 29,000 29,000 Ordinary share capital (E1 shares) Share premium Trade payables Land and buildings - cost Land and buildings -accumulated depreciation Plant and equipment -cost Plant and equipment-accumulated depreciation Trade receivables 6,135 300 6,435 9,500 9,500 5,550 800 6,350 7,355 50 7,305 Accruals 327 10 337 8% bank loan repayable 12,250 12,250 Cash at bank 6,331 30 6,361 Retained earnings 13,200 13,200 650 450 1,100 Financial Expense Revenue 23,020 23,020 Cost of Sales 10,292 10,292 5,675 650 20 6,305 Distribution costs Administrative expenses 3,850 510 4,360 Inventories 8,409 8,409 325 350 350 350 20 450 81,387 83,327 Dividends paid 325 Tax expense 350 Tax payable Prepayment 20 Interest payable 450 81,387 4,010 4,010 83,327 These local businesses do not make use of contemporary software to support its book keeping and accounting function. Your supervisor, one of the firm's Key Account Managers, has asked you to compile the year-end financial statements ready for submission and provide, for each client, some detailed analysis of the figures produced, which will be presented in the form of an accompanying letter. Specifically, you will undertake the following: 1. From the data provided, you are required to prepare the year-end financial statements, taking into consideration accounting principles, conventions and standards. You will need to make and show appropriate adjustments to both the income statement and the balance sheet. Write an accompanying letter to the client that will be sent with the completed financial statements. The letter needs to include: calculation of relevant profitably, liquidity, asset usage and investment ratios . critical evaluation of the performance to the business year on year (making reference to data you have calculated and data provided from the previous year), with reference to relevant benchmarks as well as any limitations of using financial ratios as performance measures an outline of the benefits of contemporary accounting software packages, with examples of products on the market justified conclusions and recommendations for your client. The following information is relevant: Statement of profit or loss for the year ended 31 December: 2019 2020 '000 '000 Revenue 26,000 24,000 Cost of Sales 10,800 10,500 Gross profit 15,200 13,500 Administrative expenses 4,600 4,550 Distribution costs 6,100 6,450 Finance costs 600 700 Profit before tax 3,900 1,800 Tax expense 900 450 Profit for the period 3,000 1,350 Statement of financial position as at 31 December 2019 2020 '000 '000 22,000 5,000 23,750 3,950 8,000 7,000 50 9,000 6,000 70 4,715 47,485 3,500 45,550 Non-current assets Land and buildings Plant and equipment Current assets Inventories Trade receivables Prepayments Cash at bank Total assets Equity and liabilities Equity Ordinary share capital (E1 shares) Share premium Retained earnings Total equity Non-current liabilities Borrowings Current liabilities Trade payables Accruals Tax payable Interest payable Total liabilities Total equity and liabilities 10,000 4,500 12,300 26,800 9,000 9,000 9,750 8,200 10,000 4,500 13,200 27,700 11,000 11,000 8,785 7,300 750 555 450 350 500 430 18,750 45,550 19,785 47,485