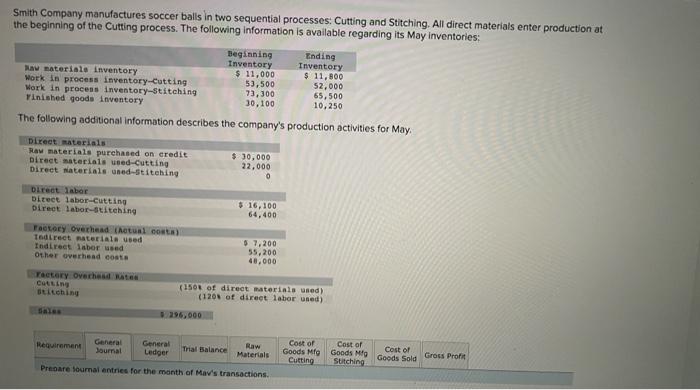

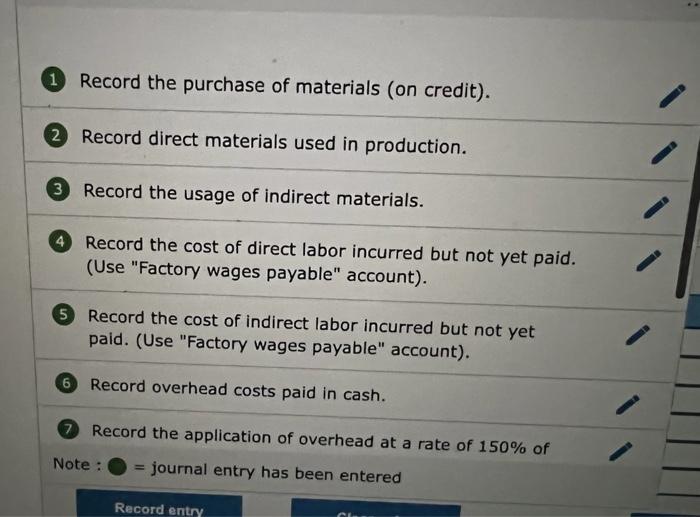

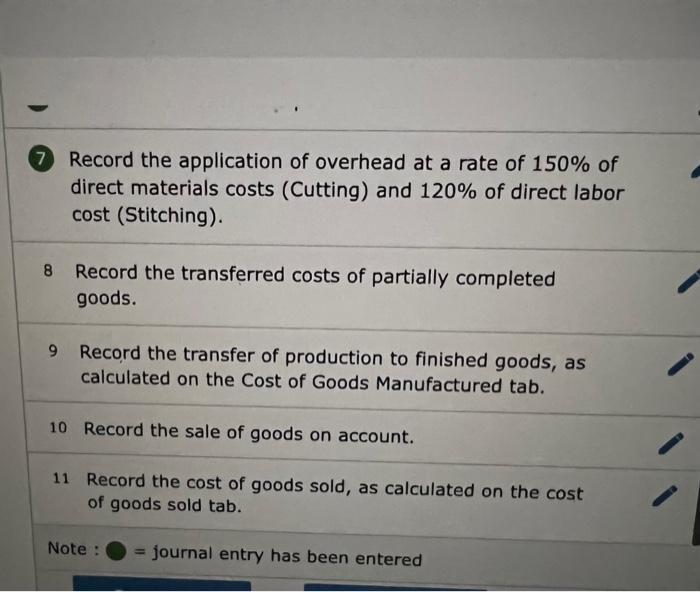

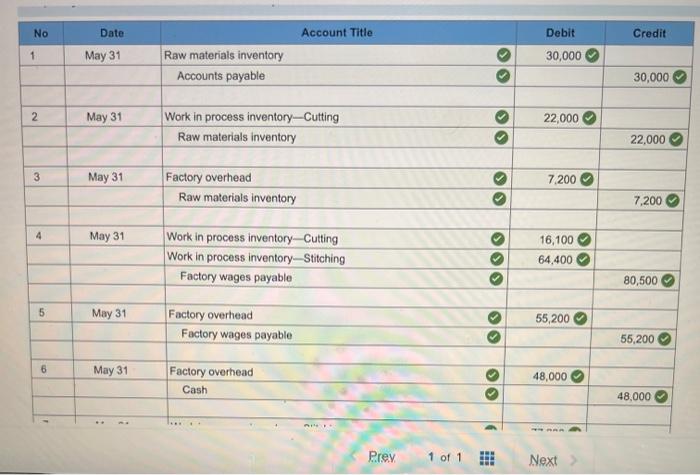

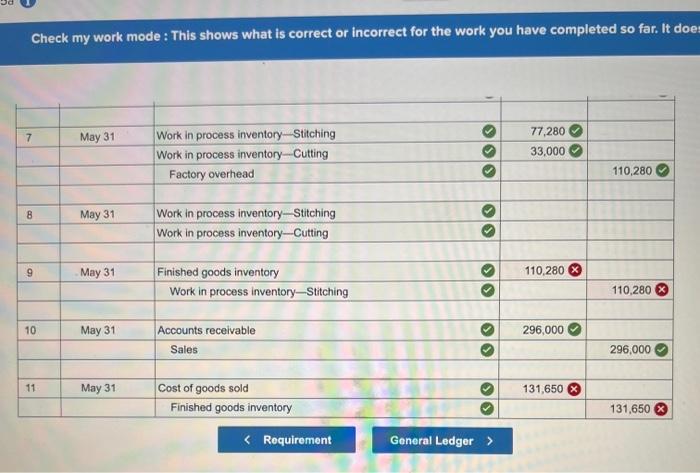

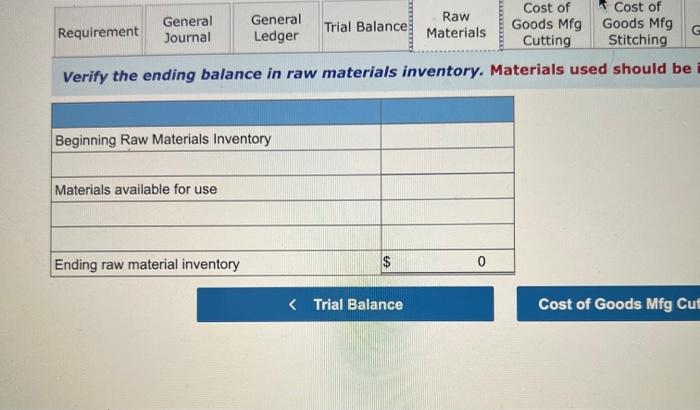

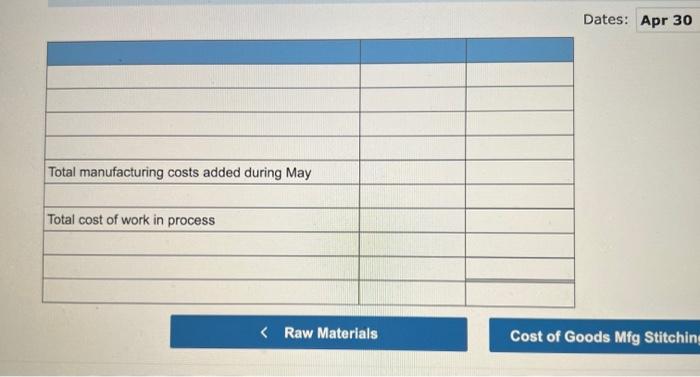

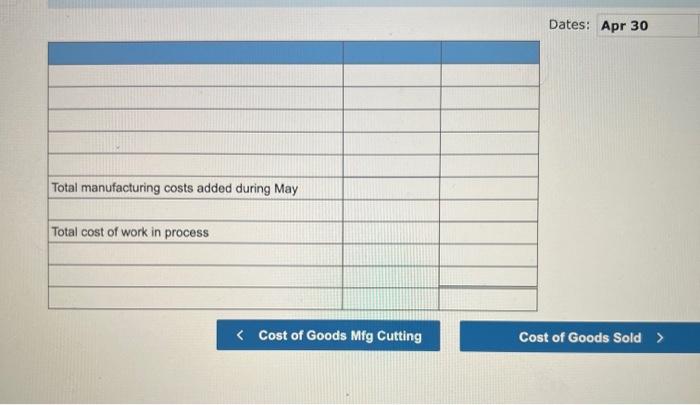

Smith Company manufactures soccer balls in two sequential processes: Cutting and Stitching. All direct materials enter production at the beginning of the Cutting process. The following information is available regarding its May inventories: Beginning Ending Inventory Inventory Raw materials inventory $ 11,000 $ 11,800 Work in process inventory-Cutting 53,500 52,000 Work in process inventory-Stitching 73,300 65,500 Finished goods inventory 30,100 10,250 The following additional Information describes the company's production activities for May Direct materials Raw materials purchased on credit Direct materials used-cutting Direct materials used-stitching $ 30,000 22.000 0 Direct labor Direct labor-cutting Direct labor-stitching $ 16,100 64,400 Factory Overhead (htul costa) Todirect materials used Indirect labor used Other overhead coats $ 7,200 55,200 40.000 Factory Ovechte Cutting stitching (1501 of direct materials used) (1205 of direct labor used) 296,000 Requirement General Journal General Ledger Trial Balance Raw Materials Cost of Goods Mo Cutting Cost of Goods Mo Suitching Cost of Goods Sold Gross Profit Prepare fournal entries for the month of Mav's transactions Record the purchase of materials (on credit). 2 Record direct materials used in production. 3 Record the usage of indirect materials. 4 Record the cost of direct labor incurred but not yet paid. (Use "Factory wages payable" account). 5 Record the cost of indirect labor incurred but not yet paid. (Use "Factory wages payable" account). 6 Record overhead costs paid in cash. Record the application of overhead at a rate of 150% of Note : journal entry has been entered Record entry 7 Record the application of overhead at a rate of 150% of direct materials costs (Cutting) and 120% of direct labor cost (Stitching). Record the transferred costs of partially completed goods. 9 Record the transfer of production to finished goods, as calculated on the Cost of Goods Manufactured tab. 10 Record the sale of goods on account. 11 Record the cost of goods sold, as calculated on the cost of goods sold tab. Note : = journal entry has been entered No Account Title Debit Credit Date May 31 1 30,000 Raw materials inventory Accounts payable 30,000 2 May 31 22,000 Work in process inventory-Cutting Raw materials inventory 22.000 3 May 31 7.200 Factory overhead Raw materials inventory 7,200 4 May 31 Work in process inventory-Cutting Work in process inventory-Stitching Factory wages payable >>> 16,100 64.400 80,500 5 May 31 Factory overhead Factory wages payable 55,200 55,200 6 May 31 Factory overhead Cash 48,000 48,000 6 Prey. 1 of 1 HE Next Check my work mode : This shows what is correct or incorrect for the work you have completed so far. It does 7 May 31 Work in process inventory Stitching Work in process inventory Cutting Factory overhead 77,280 33,000 BIO 110,280 8 May 31 Work in process inventory Stitching Work in process inventory-Cutting 9 May 31 110,280 % Finished goods inventory Work in process inventoryStitching >> 110,280 10 May 31 296,000 Accounts receivable Sales 296,000 11 May 31 131,650 Cost of goods sold Finished goods inventory 131,650 Cost of Cost of General Raw General Requirement Trial Balance Goods Mfg Goods Mfg Journal Ledger Materials G Cutting Stitching Verify the ending balance in raw materials inventory. Materials used should be Beginning Raw Materials Inventory Materials available for use Ending raw material inventory $ 0 Calculate the value of cost of goods sold for the month of May. Ignore any over- or underapp calculation of cost of goods sold. Dates: Apr 30 Calculate cost of goods sold: Cost of goods available for sale Cost of goods sold Calculate the value of gross profit for the month of May. Dates: Apr 30 to: Gross Profit