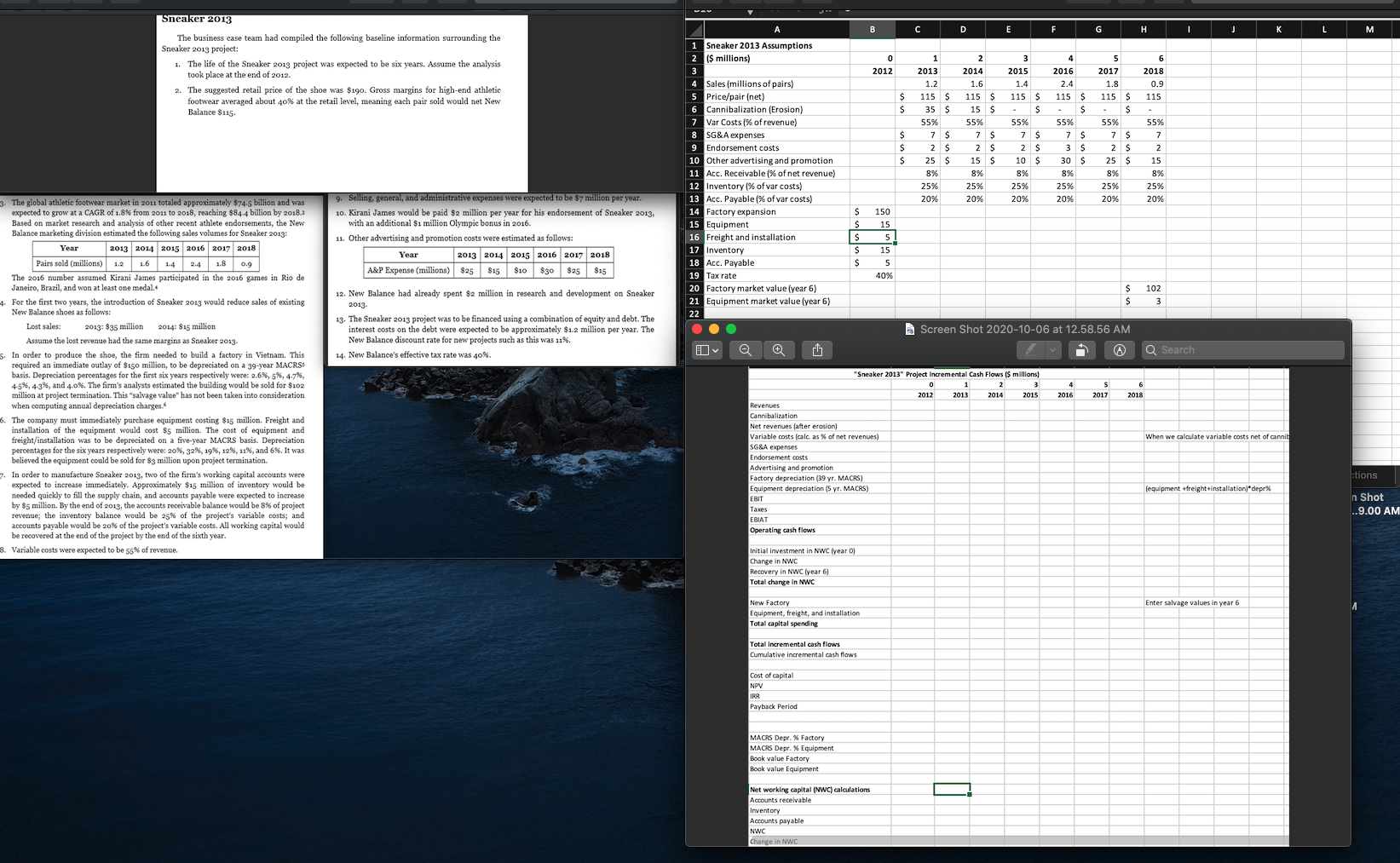

Sneaker 2013 case study assumptions and background details are given.

B D E F G H I J L M 1 Sneaker 2013 Assumptions 2 ($ millions) Sneaker 2013 The business case team had compiled the following baseline information surrounding the Sneaker 2013 project: 1. The life of the Sneaker 2013 project was expected to be six years. Assume the analysis took place at the end of 2012. 2. The suggested retail price of the shoe was $190. Gross margins for high-end athletic footwear averaged about 40% at the retail level, meaning each pair sold would net New Balance $115. 0 2012 6 2018 0.9 115 $ $ 1 2013 1.2 115 $ 35 S 55% 7 S 2 $ 25 $ 8% 25% 20% 2 2014 1.6 115 S 15 $ 55% 7 S 2 S 15 $ 8% 25% 20% 3 2015 1.4 115 $ $ 55% 7 s 2 s 10 $ 8% 25% 20% 4 Sales (millions of pairs) 5 Price/pair (net) 6 Cannibalization (Erosion) 7 Var Costs (% of revenue) 8 SG&A expenses 9 Endorsement costs 10 Other advertising and promotion 11 Acc. Receivable % of net revenue) 12 Inventory (% of var costs) 13 Acc. Payable (% of var costs) 14 Factory expansion 15 Equipment 16 Freight and installation 17 Inventory 18 Acc. Payable 19 Tax rate 20 Factory market value (year 6) 21 Equipment market value (year 6) 22 4 2016 2.4 115 $ $ 55% 7 $ 3 S 30 $ 8% 25% 20% 5 2017 1.8 115 $ $ 55% 7 S 2 $ 25 $ 89 25% 20% s s s 55% 7 2 15 8% 25% 20% 9. Selling, general, and administrative expenses were expected to be $7 million per year. 10. Kirani James would be paid $2 million per year for his endorsement of Sneaker 2013, with an additional $1 million Olympic bonus in 2016. 11. Other advertising and promotion costs were estimated as follows: Year 2013 2014 2015 2016 2017 2018 A&P Expense (millions) $25 $15 $10 $30 $25 $15 $ S 150 15 5 15 5 $ $ 40% 12. New Balance had already spent $2 million in research and development on Sneaker 2013 $ $ 102 3 Screen Shot 2020-10-06 at 12.58.56 AM 13. The Sneaker 2013 project was to be financed using a combination of equity and debt. The interest costs on the debt were expected to be approximately $1.2 million per year. The New Balance discount rate for new projects such as this was 11%. 14. New Balance's effective tax rate was 40%. Q Search 3. The global athletic footwear market in 2011 totaled approximately $74.5 billion and was expected to grow at a CAGR of 1.8% from 2011 to 2018, reaching $84.4 billion by 2018. Based on market research and analysis of other recent athlete endorsements, the New Balance marketing division estimated the following sales volumes for Sneaker 2013: Year 2013 2014 2015 2016 2017 2018 Pairs sold (millions) 1.2 1.6 1.4 2.4 1.8 0.9 The 2016 number assumed Kirani James participated in the 2016 games in Rio de Janeiro, Brazil, and won at least one medal. 4. For the first two years, the introduction Sneaker 2013 would reduce sales existing New Balance shoes as follows: Lost sales: 2013: $35 million 2014: $15 million Assume the lost revenue had the same margins as Sneaker 2013 In order produce the shoe, the firm needed to build a factory in Vietnam. This required an immediate outlay of $150 million, to be depreciated on a 39-year MACRS! basis. Depreciation percentages for the first six years respectively were: 2.6%, 5%, 4.7%, 4.5%, 4-3%, and 4.0%. The firm's analysts estimated the building would be sold for $102 million at project termination. This "salvage value has not been taken into consideration when computing annual depreciation charges. The company must immediately purchase equipment costing $15 million. Freight and installation of the equipment would cost $5 million. The cost of equipment and freight/installation was to be depreciated on a five-year MACRS basis. Depreciation percentages for the six years respectively were: 20%, 32%, 19%, 12%, 13%, and 6%. It was believed the equipment could be sold for $3 million upon project termination. In order to manufacture Sneaker 2013, two of the firm's working capital accounts were expected to increase immediately. Approximately $15 million of inventory would be needed quickly to fill the supply chain, and accounts payable were expected to increase by $5 million. By the end of 2013, the accounts receivable balance would be 8% of project revenue; the inventory balance would be 25% of the project's variable costs; and accounts payable would be 20% of the project's variable costs. All working capital would be recovered at the end of the project by the end of the sixth year. 3. Variable costs were expected to be 55% of revenue. 4 2016 5 2017 6 2018 When we calculate variable costs net of cannit Sneaker 2013" Project Incremental Cash Flows ($ millions) 0 1 2013 2014 2015 Revenues Cannibalization Net revenues (after erosion) Variable costs (calc as % of net revenues) SG&A expenses Endorsement costs Advertising and promotion Factory depreciation (39 yr. MACRS) Equipment depreciation (Syr. MACRS) EBIT Taxes EBIAT Operating cash flows tions (equipment +freight+installation) depr% In Shot ..9.00 AM Initial investment in NWC Iyear 0) Change in NWC Recovery in NWC [year 6) Total change in NWC Enter salvage values in year 6 New Factory Equipment, freight, and installation Total capital spending Total incremental cash flows Cumulative incremental cash flows Cost of capital IRR Payback Period MACRS Depr. % Factory MACRS Depr. % Equipment Book value Factory Book value Equipment Net working capital (NWC) calculations Accounts receivable Inventory Accounts payable NWC Change in NWC B D E F G H I J L M 1 Sneaker 2013 Assumptions 2 ($ millions) Sneaker 2013 The business case team had compiled the following baseline information surrounding the Sneaker 2013 project: 1. The life of the Sneaker 2013 project was expected to be six years. Assume the analysis took place at the end of 2012. 2. The suggested retail price of the shoe was $190. Gross margins for high-end athletic footwear averaged about 40% at the retail level, meaning each pair sold would net New Balance $115. 0 2012 6 2018 0.9 115 $ $ 1 2013 1.2 115 $ 35 S 55% 7 S 2 $ 25 $ 8% 25% 20% 2 2014 1.6 115 S 15 $ 55% 7 S 2 S 15 $ 8% 25% 20% 3 2015 1.4 115 $ $ 55% 7 s 2 s 10 $ 8% 25% 20% 4 Sales (millions of pairs) 5 Price/pair (net) 6 Cannibalization (Erosion) 7 Var Costs (% of revenue) 8 SG&A expenses 9 Endorsement costs 10 Other advertising and promotion 11 Acc. Receivable % of net revenue) 12 Inventory (% of var costs) 13 Acc. Payable (% of var costs) 14 Factory expansion 15 Equipment 16 Freight and installation 17 Inventory 18 Acc. Payable 19 Tax rate 20 Factory market value (year 6) 21 Equipment market value (year 6) 22 4 2016 2.4 115 $ $ 55% 7 $ 3 S 30 $ 8% 25% 20% 5 2017 1.8 115 $ $ 55% 7 S 2 $ 25 $ 89 25% 20% s s s 55% 7 2 15 8% 25% 20% 9. Selling, general, and administrative expenses were expected to be $7 million per year. 10. Kirani James would be paid $2 million per year for his endorsement of Sneaker 2013, with an additional $1 million Olympic bonus in 2016. 11. Other advertising and promotion costs were estimated as follows: Year 2013 2014 2015 2016 2017 2018 A&P Expense (millions) $25 $15 $10 $30 $25 $15 $ S 150 15 5 15 5 $ $ 40% 12. New Balance had already spent $2 million in research and development on Sneaker 2013 $ $ 102 3 Screen Shot 2020-10-06 at 12.58.56 AM 13. The Sneaker 2013 project was to be financed using a combination of equity and debt. The interest costs on the debt were expected to be approximately $1.2 million per year. The New Balance discount rate for new projects such as this was 11%. 14. New Balance's effective tax rate was 40%. Q Search 3. The global athletic footwear market in 2011 totaled approximately $74.5 billion and was expected to grow at a CAGR of 1.8% from 2011 to 2018, reaching $84.4 billion by 2018. Based on market research and analysis of other recent athlete endorsements, the New Balance marketing division estimated the following sales volumes for Sneaker 2013: Year 2013 2014 2015 2016 2017 2018 Pairs sold (millions) 1.2 1.6 1.4 2.4 1.8 0.9 The 2016 number assumed Kirani James participated in the 2016 games in Rio de Janeiro, Brazil, and won at least one medal. 4. For the first two years, the introduction Sneaker 2013 would reduce sales existing New Balance shoes as follows: Lost sales: 2013: $35 million 2014: $15 million Assume the lost revenue had the same margins as Sneaker 2013 In order produce the shoe, the firm needed to build a factory in Vietnam. This required an immediate outlay of $150 million, to be depreciated on a 39-year MACRS! basis. Depreciation percentages for the first six years respectively were: 2.6%, 5%, 4.7%, 4.5%, 4-3%, and 4.0%. The firm's analysts estimated the building would be sold for $102 million at project termination. This "salvage value has not been taken into consideration when computing annual depreciation charges. The company must immediately purchase equipment costing $15 million. Freight and installation of the equipment would cost $5 million. The cost of equipment and freight/installation was to be depreciated on a five-year MACRS basis. Depreciation percentages for the six years respectively were: 20%, 32%, 19%, 12%, 13%, and 6%. It was believed the equipment could be sold for $3 million upon project termination. In order to manufacture Sneaker 2013, two of the firm's working capital accounts were expected to increase immediately. Approximately $15 million of inventory would be needed quickly to fill the supply chain, and accounts payable were expected to increase by $5 million. By the end of 2013, the accounts receivable balance would be 8% of project revenue; the inventory balance would be 25% of the project's variable costs; and accounts payable would be 20% of the project's variable costs. All working capital would be recovered at the end of the project by the end of the sixth year. 3. Variable costs were expected to be 55% of revenue. 4 2016 5 2017 6 2018 When we calculate variable costs net of cannit Sneaker 2013" Project Incremental Cash Flows ($ millions) 0 1 2013 2014 2015 Revenues Cannibalization Net revenues (after erosion) Variable costs (calc as % of net revenues) SG&A expenses Endorsement costs Advertising and promotion Factory depreciation (39 yr. MACRS) Equipment depreciation (Syr. MACRS) EBIT Taxes EBIAT Operating cash flows tions (equipment +freight+installation) depr% In Shot ..9.00 AM Initial investment in NWC Iyear 0) Change in NWC Recovery in NWC [year 6) Total change in NWC Enter salvage values in year 6 New Factory Equipment, freight, and installation Total capital spending Total incremental cash flows Cumulative incremental cash flows Cost of capital IRR Payback Period MACRS Depr. % Factory MACRS Depr. % Equipment Book value Factory Book value Equipment Net working capital (NWC) calculations Accounts receivable Inventory Accounts payable NWC Change in NWC