So we were given a practice case to assist us in preparing us for the exam. I tried solving it, but was not sure if the answers are correct. Is anyone able to answer each component step by step of this case. It would really help identify where I went wrong in my analysis or if I did it correctly. Thank you

ALL the information about this is posted in these screenshots. There is no other info

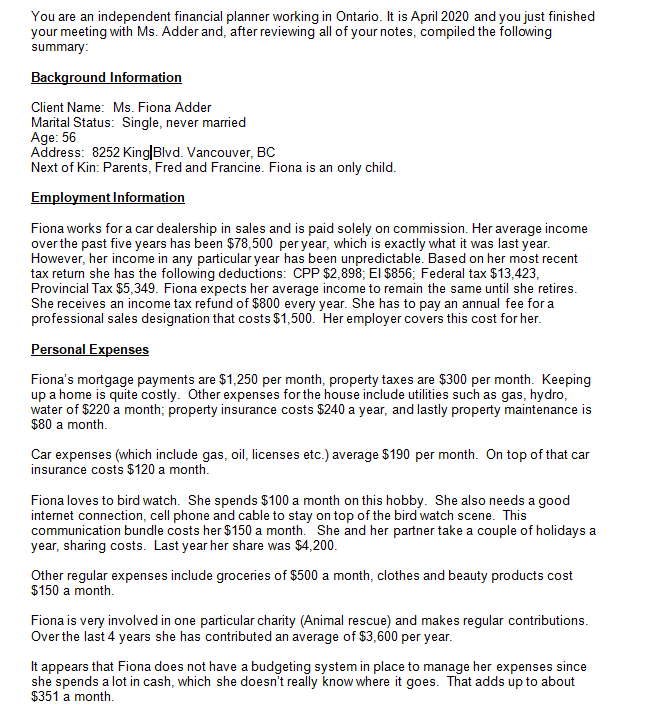

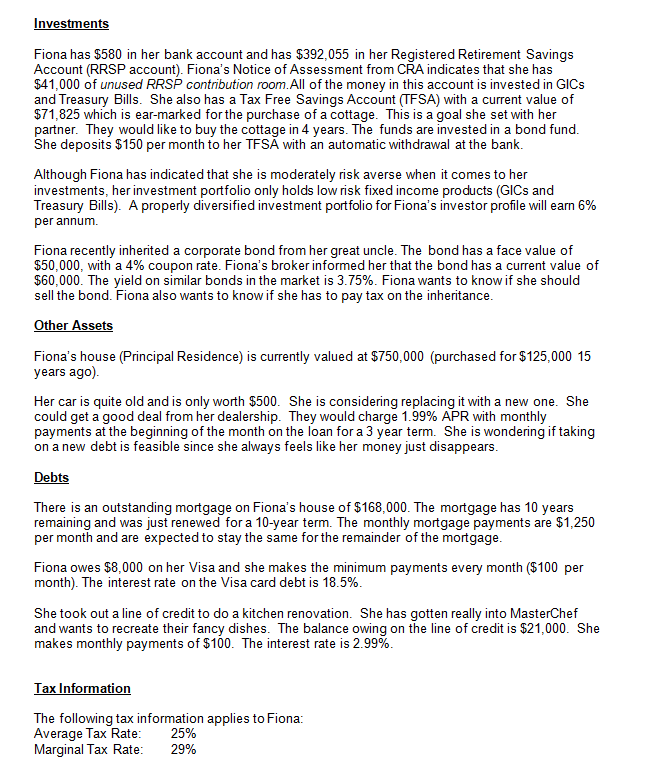

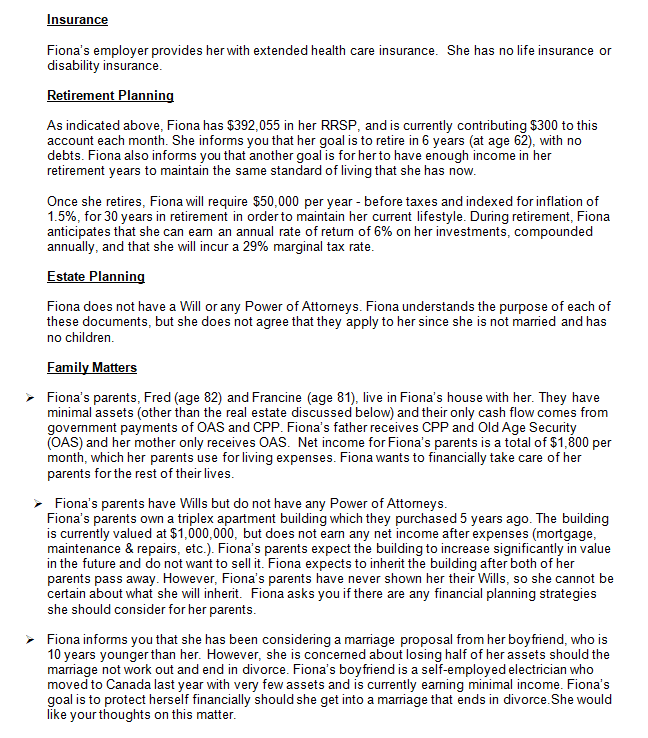

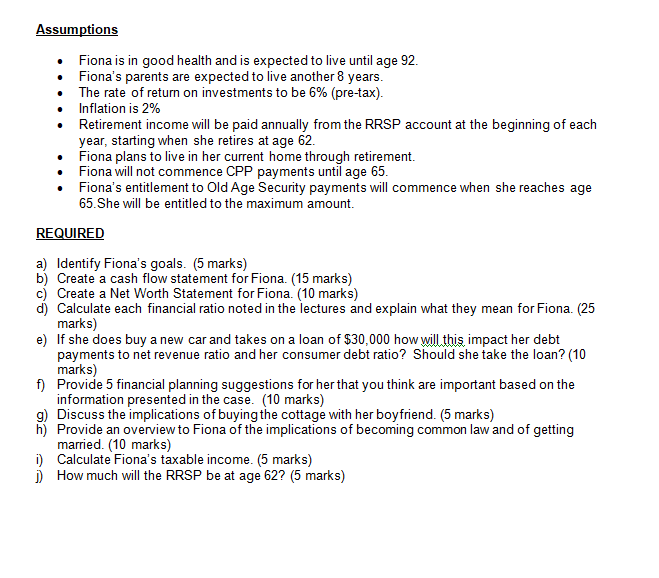

You are an independent financial planner working in Ontario. It is April 2020 and you just finished your meeting with Ms. Adder and, after reviewing all of your notes, compiled the following summary: Background Information Client Name: Ms. Fiona Adder Marital Status: Single, never married Age: 56 Address: 8252 King|Blvd. Vancouver, BC Next of kin: Parents, Fred and Francine. Fiona is an only child. Employment Information Fiona works for a car dealership in sales and is paid solely on commission. Her average income over the past five years has been $78,500 per year, which is exactly what it was last year. However, her income in any particular year has been unpredictable. Based on her most recent tax return she has the following deductions: CPP $2,898; EI $856; Federal tax $13,423, Provincial Tax $5,349. Fiona expects her average income to remain the same until she retires. She receives an income tax refund of $800 every year. She has to pay an annual fee for a professional sales designation that costs $1,500. Her employer covers this cost for her. Personal Expenses Fiona's mortgage payments are $1,250 per month, property taxes are $300 per month. Keeping up a home is quite costly. Other expenses for the house include utilities such as gas, hydro, water of $220 a month; property insurance costs $240 a year, and lastly property maintenance is $80 a month. Car expenses (which include gas, oil, licenses etc.) average $190 per month. On top of that car insurance costs $120 a month. Fiona loves to bird watch. She spends $100 a month on this hobby. She also needs a good internet connection, cell phone and cable to stay on top of the bird watch scene. This communication bundle costs her $150 a month. She and her partner take a couple of holidays a year, sharing costs. Last year her share was $4,200. Other regular expenses include groceries of $500 a month, clothes and beauty products cost $150 a month. Fiona is very involved in one particular charity (Animal rescue) and makes regular contributions. Over the last 4 years she has contributed an average of $3,600 per year. It appears that Fiona does not have a budgeting system in place to manage her expenses since she spends a lot in cash, which she doesn't really know where it goes. That adds up to about $351 a month. Investments Fiona has $580 in her bank account and has $392,055 in her Registered Retirement Savings Account (RRSP account). Fiona's Notice of Assessment from CA indicates that she has $41,000 of unused RRSP contribution room. All of the money in this account is invested in GICs and Treasury Bills. She also has a Tax Free Savings Account (TFSA) with a current value of $71,825 which is ear-marked for the purchase of a cottage. This is a goal she set with her partner. They would like to buy the cottage in 4 years. The funds are invested in a bond fund. She deposits $150 per month to her TFS with an automatic withdrawal at the bank. Although Fiona has indicated that she is moderately risk averse when it comes to her investments, her investment portfolio only holds low risk fixed income products (GICs and Treasury Bills). A properly diversified investment portfolio for Fiona's investor profile will earn 6% per annum Fiona recently inherited a corporate bond from her great uncle. The bond has a face value of $50,000, with a 4% coupon rate. Fiona's broker informed her that the bond has a current value of $60,000. The yield on similar bonds in the market is 3.75%. Fiona wants to know if she should sell the bond. Fiona also wants to know if she has to pay tax on the inheritance. Other Assets Fiona's house (Principal Residence) is currently valued at $750,000 (purchased for $125,000 15 years ago) Her car is quite old and is only worth $500. She is considering replacing it with a new one. She could get a good deal from her dealership. They would charge 1.99% APR with monthly payments at the beginning of the month on the loan for a 3 year term. She is wondering if taking on a new debt is feasible since she always feels like her money just disappears. Debts There is an outstanding mortgage on Fiona's house of $168,000. The mortgage has 10 years remaining and was just renewed for a 10-year term. The monthly mortgage payments are $1,250 per month and are expected to stay the same for the remainder of the mortgage. Fiona owes $8,000 on her Visa and she makes the minimum payments every month ($100 per month). The interest rate on the Visa card debt is 18.5%. She took out a line of credit to do a kitchen renovation. She has gotten really into MasterChef and wants to recreate their fancy dishes. The balance owing on the line of credit is $21,000. She makes monthly payments of $100. The interest rate is 2.99% Tax Information The following tax information applies to Fiona: Average Tax Rate: 25% Marginal Tax Rate: 29% Insurance Fiona's employer provides her with extended health care insurance. She has no life insurance or disability insurance. Retirement Planning As indicated above, Fiona has $392,055 in her RRSP, and is currently contributing $300 to this account each month. She informs you that her goal is to retire in 6 years (at age 62), with no debts. Fiona also informs you that another goal is for her to have enough income in her retirement years to maintain the same standard of living that she has now. Once she retires, Fiona will require $50,000 per year- before taxes and indexed for inflation of 1.5%, for 30 years in retirement in order to maintain her current lifestyle. During retirement, Fiona anticipates that she can earn an annual rate of return of 6% on her investments, compounded annually, and that she will incur a 29% marginal tax rate. Estate Planning Fiona does not have a Will or any Power of Attorneys. Fiona understands the purpose of each of these documents, but she does not agree that they apply to her since she is not married and has no children. Family Matters Fiona's parents, Fred (age 82) and Francine (age 81), live in Fiona's house with her. They have minimal assets (other than the real estate discussed below) and their only cash flow comes from government payments of OAS and CPP. Fiona's father receives CPP and Old Age Security (OAS) and her mother only receives OAS. Net income for Fiona's parents is a total of $1,800 per month, which her parents use for living expenses. Fiona wants to financially take care of her parents for the rest of their lives. Fiona's parents have Wills but do not have any Power of Attorneys. Fiona's parents own a triplex apartment building which they purchased 5 years ago. The building is currently valued at $1,000,000, but does not earn any net income after expenses (mortgage, maintenance & repairs, etc.). Fiona's parents expect the building to increase significantly in value in the future and do not want to sell it. Fiona expects to inherit the building after both of her parents pass away. However, Fiona's parents have never shown her their Wills, so she cannot be certain about what she will inherit. Fiona asks you if there are any financial planning strategies she should consider for her parents. Fiona informs you that she has been considering a marriage proposal from her boyfriend, who is 10 years younger than her. However, she is concerned about losing half of her assets should the marriage not work out and end in divorce. Fiona's boyfriend is a self-employed electrician who moved to Canada last year with very few assets and is currently earning minimal income. Fiona's goal is to protect herself financially should she get into a marriage that ends in divorce. She would like your thoughts on this matter. Assumptions Fiona is in good health and is expected to live until age 92. Fiona's parents are expected to live another 8 years. The rate of return on investments to be 6% (pre-tax). Inflation is 2% Retirement income will be paid annually from the RRSP account at the beginning of each year, starting when she retires at age 62. Fiona plans to live in her current home through retirement. Fiona will not commence CPP payments until age 65. Fiona's entitlement to Old Age Security payments will commence when she reaches age 65. She will be entitled to the maximum amount. REQUIRED a) Identify Fiona's goals. (5 marks) b) Create a cash flow statement for Fiona. (15 marks) c) Create a Net Worth Statement for Fiona (10 marks) d) Calculate each financial ratio noted in the lectures and explain what they mean for Fiona. (25 marks) e) If she does buy a new car and takes on a loan of $30,000 how will this impact her debt payments to net revenue ratio and her consumer debt ratio? Should she take the loan? (10 marks) f) Provide 5 financial planning suggestions for her that you think are important based on the information presented in the case. (10 marks) g) Discuss the implications of buying the cottage with her boyfriend. (5 marks) h) Provide an overview to Fiona of the implications of becoming common law and of getting married. (10 marks) i) Calculate Fiona's taxable income. (5 marks) j) How much will the RRSP be at age 62? (5 marks) You are an independent financial planner working in Ontario. It is April 2020 and you just finished your meeting with Ms. Adder and, after reviewing all of your notes, compiled the following summary: Background Information Client Name: Ms. Fiona Adder Marital Status: Single, never married Age: 56 Address: 8252 King|Blvd. Vancouver, BC Next of kin: Parents, Fred and Francine. Fiona is an only child. Employment Information Fiona works for a car dealership in sales and is paid solely on commission. Her average income over the past five years has been $78,500 per year, which is exactly what it was last year. However, her income in any particular year has been unpredictable. Based on her most recent tax return she has the following deductions: CPP $2,898; EI $856; Federal tax $13,423, Provincial Tax $5,349. Fiona expects her average income to remain the same until she retires. She receives an income tax refund of $800 every year. She has to pay an annual fee for a professional sales designation that costs $1,500. Her employer covers this cost for her. Personal Expenses Fiona's mortgage payments are $1,250 per month, property taxes are $300 per month. Keeping up a home is quite costly. Other expenses for the house include utilities such as gas, hydro, water of $220 a month; property insurance costs $240 a year, and lastly property maintenance is $80 a month. Car expenses (which include gas, oil, licenses etc.) average $190 per month. On top of that car insurance costs $120 a month. Fiona loves to bird watch. She spends $100 a month on this hobby. She also needs a good internet connection, cell phone and cable to stay on top of the bird watch scene. This communication bundle costs her $150 a month. She and her partner take a couple of holidays a year, sharing costs. Last year her share was $4,200. Other regular expenses include groceries of $500 a month, clothes and beauty products cost $150 a month. Fiona is very involved in one particular charity (Animal rescue) and makes regular contributions. Over the last 4 years she has contributed an average of $3,600 per year. It appears that Fiona does not have a budgeting system in place to manage her expenses since she spends a lot in cash, which she doesn't really know where it goes. That adds up to about $351 a month. Investments Fiona has $580 in her bank account and has $392,055 in her Registered Retirement Savings Account (RRSP account). Fiona's Notice of Assessment from CA indicates that she has $41,000 of unused RRSP contribution room. All of the money in this account is invested in GICs and Treasury Bills. She also has a Tax Free Savings Account (TFSA) with a current value of $71,825 which is ear-marked for the purchase of a cottage. This is a goal she set with her partner. They would like to buy the cottage in 4 years. The funds are invested in a bond fund. She deposits $150 per month to her TFS with an automatic withdrawal at the bank. Although Fiona has indicated that she is moderately risk averse when it comes to her investments, her investment portfolio only holds low risk fixed income products (GICs and Treasury Bills). A properly diversified investment portfolio for Fiona's investor profile will earn 6% per annum Fiona recently inherited a corporate bond from her great uncle. The bond has a face value of $50,000, with a 4% coupon rate. Fiona's broker informed her that the bond has a current value of $60,000. The yield on similar bonds in the market is 3.75%. Fiona wants to know if she should sell the bond. Fiona also wants to know if she has to pay tax on the inheritance. Other Assets Fiona's house (Principal Residence) is currently valued at $750,000 (purchased for $125,000 15 years ago) Her car is quite old and is only worth $500. She is considering replacing it with a new one. She could get a good deal from her dealership. They would charge 1.99% APR with monthly payments at the beginning of the month on the loan for a 3 year term. She is wondering if taking on a new debt is feasible since she always feels like her money just disappears. Debts There is an outstanding mortgage on Fiona's house of $168,000. The mortgage has 10 years remaining and was just renewed for a 10-year term. The monthly mortgage payments are $1,250 per month and are expected to stay the same for the remainder of the mortgage. Fiona owes $8,000 on her Visa and she makes the minimum payments every month ($100 per month). The interest rate on the Visa card debt is 18.5%. She took out a line of credit to do a kitchen renovation. She has gotten really into MasterChef and wants to recreate their fancy dishes. The balance owing on the line of credit is $21,000. She makes monthly payments of $100. The interest rate is 2.99% Tax Information The following tax information applies to Fiona: Average Tax Rate: 25% Marginal Tax Rate: 29% Insurance Fiona's employer provides her with extended health care insurance. She has no life insurance or disability insurance. Retirement Planning As indicated above, Fiona has $392,055 in her RRSP, and is currently contributing $300 to this account each month. She informs you that her goal is to retire in 6 years (at age 62), with no debts. Fiona also informs you that another goal is for her to have enough income in her retirement years to maintain the same standard of living that she has now. Once she retires, Fiona will require $50,000 per year- before taxes and indexed for inflation of 1.5%, for 30 years in retirement in order to maintain her current lifestyle. During retirement, Fiona anticipates that she can earn an annual rate of return of 6% on her investments, compounded annually, and that she will incur a 29% marginal tax rate. Estate Planning Fiona does not have a Will or any Power of Attorneys. Fiona understands the purpose of each of these documents, but she does not agree that they apply to her since she is not married and has no children. Family Matters Fiona's parents, Fred (age 82) and Francine (age 81), live in Fiona's house with her. They have minimal assets (other than the real estate discussed below) and their only cash flow comes from government payments of OAS and CPP. Fiona's father receives CPP and Old Age Security (OAS) and her mother only receives OAS. Net income for Fiona's parents is a total of $1,800 per month, which her parents use for living expenses. Fiona wants to financially take care of her parents for the rest of their lives. Fiona's parents have Wills but do not have any Power of Attorneys. Fiona's parents own a triplex apartment building which they purchased 5 years ago. The building is currently valued at $1,000,000, but does not earn any net income after expenses (mortgage, maintenance & repairs, etc.). Fiona's parents expect the building to increase significantly in value in the future and do not want to sell it. Fiona expects to inherit the building after both of her parents pass away. However, Fiona's parents have never shown her their Wills, so she cannot be certain about what she will inherit. Fiona asks you if there are any financial planning strategies she should consider for her parents. Fiona informs you that she has been considering a marriage proposal from her boyfriend, who is 10 years younger than her. However, she is concerned about losing half of her assets should the marriage not work out and end in divorce. Fiona's boyfriend is a self-employed electrician who moved to Canada last year with very few assets and is currently earning minimal income. Fiona's goal is to protect herself financially should she get into a marriage that ends in divorce. She would like your thoughts on this matter. Assumptions Fiona is in good health and is expected to live until age 92. Fiona's parents are expected to live another 8 years. The rate of return on investments to be 6% (pre-tax). Inflation is 2% Retirement income will be paid annually from the RRSP account at the beginning of each year, starting when she retires at age 62. Fiona plans to live in her current home through retirement. Fiona will not commence CPP payments until age 65. Fiona's entitlement to Old Age Security payments will commence when she reaches age 65. She will be entitled to the maximum amount. REQUIRED a) Identify Fiona's goals. (5 marks) b) Create a cash flow statement for Fiona. (15 marks) c) Create a Net Worth Statement for Fiona (10 marks) d) Calculate each financial ratio noted in the lectures and explain what they mean for Fiona. (25 marks) e) If she does buy a new car and takes on a loan of $30,000 how will this impact her debt payments to net revenue ratio and her consumer debt ratio? Should she take the loan? (10 marks) f) Provide 5 financial planning suggestions for her that you think are important based on the information presented in the case. (10 marks) g) Discuss the implications of buying the cottage with her boyfriend. (5 marks) h) Provide an overview to Fiona of the implications of becoming common law and of getting married. (10 marks) i) Calculate Fiona's taxable income. (5 marks) j) How much will the RRSP be at age 62