Answered step by step

Verified Expert Solution

Question

1 Approved Answer

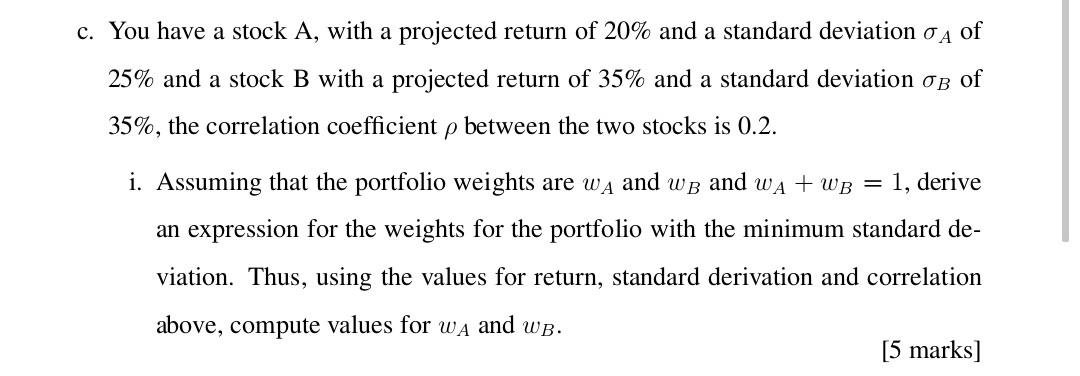

solve asap please c. You have a stock A, with a projected return of 20% and a standard deviation A of 25% and a stock

solve asap please

c. You have a stock A, with a projected return of 20% and a standard deviation A of 25% and a stock B with a projected return of 35% and a standard deviation B of 35%, the correlation coefficient between the two stocks is 0.2. i. Assuming that the portfolio weights are wA and wB and wA+wB=1, derive an expression for the weights for the portfolio with the minimum standard deviation. Thus, using the values for return, standard derivation and correlation above, compute values for wA and wB. [5 marks]Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managing Currency Options In Financial Institutions

Authors: Yat-Fai Lam, Kin-Keung Lai

1st Edition

1138778052, 978-1138778054